If you have ever tried to save for retirement, you have probably come across two popular options: Roth IRA vs Traditional IRA. These two accounts look similar on the surface, but they work in completely different ways when it comes to taxes, withdrawals, and long-term wealth building.

Choosing between a Roth IRA vs Traditional IRA is one of the most important financial decisions you will make for your retirement. The wrong choice can cost you thousands of dollars in unnecessary taxes over your lifetime. The right choice, on the other hand, can supercharge your savings and let your money grow with maximum efficiency.

In this complete guide, we break down everything you need to know about Roth IRA vs Traditional IRA — contributions, tax benefits, income limits, withdrawal rules, and who each account is best for in 2026. By the end, you will know exactly which account fits your financial situation.

What Is an IRA?

An Individual Retirement Account (IRA) is a tax-advantaged savings account that helps you build wealth for retirement. Unlike a 401(k), which is offered through your employer, an IRA is something you open yourself through a bank, brokerage, or financial institution.

There are two main types — and understanding the Roth IRA vs Traditional IRA difference is the foundation of smart retirement planning.

What Is a Roth IRA?

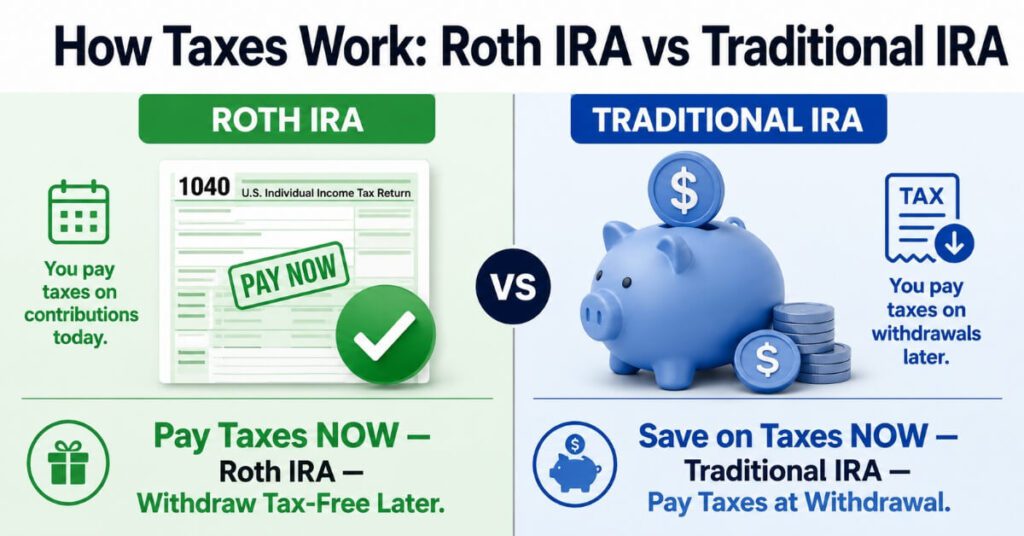

A Roth IRA is a retirement account where you contribute after-tax money. You pay taxes on your income now, invest it in the Roth IRA, and when you withdraw that money in retirement, you pay zero taxes on both the contributions and the growth.

This is the core advantage of the Roth IRA vs Traditional IRA comparison — tax-free money in retirement.

Key Features of a Roth IRA (2026):

Contribution Limit: $7,500 per year (under age 50) | $8,600 per year (age 50+)

Income Limit: Single filers must earn less than $153,000 | Married filing jointly must earn less than $242,000

Tax on Contributions: Paid now (after-tax dollars)

Tax on Withdrawals: Zero — completely tax-free in retirement

Required Minimum Distributions (RMDs): None during the account owner’s lifetime

Early Withdrawal: Contributions (not earnings) can be withdrawn anytime without penalty

What Is a Traditional IRA?

A Traditional IRA is a retirement account where you contribute pre-tax money. Your contributions may be tax-deductible, which reduces your taxable income today. However, when you withdraw the money in retirement, you pay income tax on every dollar you take out.

In the Roth IRA vs Traditional IRA debate, Traditional IRA gives you the tax benefit now — while Roth IRA gives you the tax benefit later.

Key Features of a Traditional IRA (2026):

Contribution Limit: $7,500 per year (under age 50) | $8,600 per year (age 50+)

Income Limit: No income limit to contribute, but deductibility phases out based on income and workplace plan coverage

Tax on Contributions: May be tax-deductible (pre-tax dollars)

Tax on Withdrawals: Taxed as ordinary income

Required Minimum Distributions (RMDs): Must begin at age 73

Early Withdrawal: 10% penalty plus taxes if withdrawn before age 59½

Roth IRA vs Traditional IRA: Side-by-Side Comparison

Here is a clear breakdown of how Roth IRA vs Traditional IRA compares fon every major factor:

| Feature | Roth IRA | Traditional IRA |

| Tax on Contributions | After-tax (no deduction) | Pre-tax (may be deductible) |

| Tax on Withdrawals | Tax-free | Taxed as income |

| 2026 Contribution Limit | $7,500 / $8,600 (50+) | $7,500 / $8,600 (50+) |

| Income Limits | Yes — phases out above $153K (single) | No limit to contribute |

| RMDs Required | No | Yes, starting at age 73 |

| Early Withdrawal Rules | Contributions anytime penalty-free | 10% penalty + taxes before 59½ |

| Best For | Young earners, low current tax bracket | High earners, expecting lower retirement tax |

When you look at both accounts side by side like this, it becomes clear that they serve very different types of investors.

Tax Differences: The Heart of the Roth IRA vs Traditional IRA Decision

The biggest factor in choosing between these two accounts is taxes — specifically, when you pay them and at what rate.

Pay Taxes Now or Later?

The core question when comparing these accounts is simple:

Roth IRA = Pay taxes NOW at your current tax rate. Grow tax-free. Withdraw tax-free.

Traditional IRA = Get a tax break NOW. Pay taxes LATER at your retirement tax rate.

Which Tax Strategy Wins?

If you are young and in a low tax bracket today, but expect your income (and therefore tax rate) to grow significantly over your career, the Roth IRA vs Traditional IRA math clearly favors the Roth. You lock in a low tax rate now, and all future growth is completely tax-free.

If you are currently in a high tax bracket and expect your retirement income to be lower, the Traditional IRA wins this comparison. You get the deduction now when taxes are expensive, and pay them later when they are cheaper.

2026 Contribution Limits: Roth IRA vs Traditional IRA

Both accounts share the same contribution limits in 2026:

Under age 50: $7,500 per year

Age 50 and above: $8,600 per year (includes $1,100 catch-up contribution)

Important note: The $7,500 limit is combined across ALL IRAs. If you contribute $4,000 to a Roth IRA, you can only put $3,500 in a Traditional IRA that same year.

This is a critical rule that many beginners overlook when opening their first IRA

2026 Income Limits: Roth IRA vs Traditional IRA

Income limits are one of the major differences between these two retirement accounts.

Roth IRA Income Limits (2026):

Single filers: Full contribution if income is below $153,000 | Partial contribution between $153,000–$168,000 | No contribution above $168,000

Married filing jointly: Full contribution below $242,000 | Partial contribution between $242,000–$252,000 | No contribution above $252,000

Traditional IRA Income Limits (2026):

Anyone with earned income can contribute to a Traditional IRA regardless of how much they earn.

However, tax deductibility phases out if you or your spouse have a workplace retirement plan:

Single filers covered by workplace plan: Deduction phases out between $81,000–$91,000

Married filing jointly (you are covered): Phases out between $129,000–$149,000

This distinction is often missed in the Roth IRA vs Traditional IRA debate. High earners can still contribute to a Traditional IRA — they just may not get the tax deduction.

Withdrawal Rules: Roth IRA vs Traditional IRA

Withdrawal rules are another critical area where these two accounts differ significantly.

Roth IRA Withdrawal Rules:

Contributions: Can be withdrawn at ANY time, at ANY age, with NO penalties and NO taxes. You already paid tax on them.

Earnings: Must wait until age 59½ AND the account must be at least 5 years old for tax-free, penalty-free withdrawal.

RMDs: Not required during the owner’s lifetime. This makes the Roth a strong choice for estate planning purposes.

Traditional IRA Withdrawal Rules:

Before age 59½: 10% early withdrawal penalty plus ordinary income taxes apply.

After age 59½: Withdrawals are taxed as ordinary income. No penalty.

RMDs: Must start withdrawing a minimum amount each year beginning at age 73. Failure to take RMDs results in a 25% penalty on the amount that should have been withdrawn.

For someone who wants maximum flexibility, the Roth IRA vs Traditional IRA comparison clearly favors the Roth.

Roth IRA vs Traditional IRA: Who Should Choose Which?

Choose a Roth IRA If:

You are young and early in your career with lower income today

You are currently in the 22% tax bracket or lower

You expect your income to increase significantly in the future

You want tax-free income in retirement

You want no required minimum distributions

You want flexibility to access contributions penalty-free in emergencies

Choose a Traditional IRA If:

You are currently in a high tax bracket (32% or above)

You expect your income (and tax rate) to be lower in retirement

You need to reduce your taxable income now

You are closer to retirement and want immediate tax savings

You earn too much for Roth IRA income limits

The Roth IRA vs Traditional IRA decision is personal. There is no universal “best” answer — it depends entirely on your current income, expected future income, and tax situation

Can You Have Both a Roth IRA and Traditional IRA?

Yes! The IRS allows you to contribute to both accounts in the same year. However, the combined total cannot exceed the annual limit of $7,500 ($8,600 if 50+).

This split strategy can help you hedge your tax exposure — you get some tax benefit now through the Traditional IRA and some tax-free growth for the future through the Roth IRA. This is one of the smartest moves in the Roth IRA vs Traditional IRA playbook.

What Is a Backdoor Roth IRA?

If your income is too high to contribute directly to a Roth IRA, the Backdoor Roth IRA strategy is a legal workaround. Here is how it works:

Contribute to a Traditional IRA (no income limit to contribute)

Convert that Traditional IRA to a Roth IRA

Pay taxes on the converted amount

Enjoy tax-free growth going forward

This strategy makes the comparison even more relevant for high earners, because it opens the Roth IRA door regardless of income.

Roth IRA vs Traditional IRA for Retirement Income Planning

When planning retirement income, the difference between these two accounts becomes very powerful:

Traditional IRA withdrawals count as taxable income, which can push you into a higher bracket, increase Medicare premiums, and make more of your Social Security benefits taxable.

Roth IRA withdrawals are completely tax-free and do not count as income for these purposes.

For this reason, many financial planners recommend building a mix of both Traditional and Roth savings, giving you flexibility to control your taxable income in retirement. This is the real long-term power of understanding the Roth IRA vs Traditional IRA difference.

Roth IRA vs Traditional IRA: Impact on Social Security

This is something many people miss entirely. Traditional IRA withdrawals add to your adjusted gross income, which can cause up to 85% of your Social Security benefits to be taxed. Roth IRA withdrawals do not affect Social Security taxation at all.

Over a 20–30 year retirement, this difference can add up to tens of thousands of dollars in savings. It is a powerful reason to consider the Roth side of the Roth IRA vs Traditional IRA equation carefully.

Common Mistakes to Avoid

When choosing between these two retirement accounts, people often make these mistakes:

1 .Not starting early — Time in the market matters more than which account you choose.

2 .Ignoring income limits — Contributing to a Roth IRA above the income limit triggers IRS penalties.

3 .Missing the contribution deadline — You can make 2026 IRA contributions until Tax Day 2027.

4 .Not contributing the maximum — Many people contribute far less than the allowed $7,500.

5 .Forgetting about RMDs — Traditional IRA holders must plan for mandatory withdrawals at 73.

Roth IRA vs Traditional IRA: Which Is Better in 2026?

Here is the honest answer: both are excellent retirement tools, and the best choice depends on your individual situation.

In 2026, with updated contribution limits and shifted income thresholds, the Roth IRA vs Traditional IRA decision is clearer than ever:

If you are under 40, earning under $100,000, and in the early stages of your career → Roth IRA wins

If you are over 50, in the 32%+ tax bracket, and looking to reduce today’s taxes → Traditional IRA wins

If you are somewhere in the middle → Contribute to both and diversify your tax exposure

The one mistake you should never make is doing nothing — both accounts are far better than no retirement savings at all.

For official guidance on mutual fund investing and investor protection, refer to SEBI Investor – Understanding Mutual Funds before making any investment decisions.

FAQs: Roth IRA vs Traditional IRA

Q1. What is the main difference between Roth IRA vs Traditional IRA?

The main difference is when you pay taxes. With a Roth IRA, you pay taxes now and withdraw tax-free. With a Traditional IRA, you get a tax deduction now but pay taxes on withdrawals in retirement.

Q2. Which is better — Roth IRA or Traditional IRA?

It depends on your tax situation. Roth IRA is generally better for younger earners expecting income growth. Traditional IRA is better for high earners who need to reduce taxes today.

Q3. Can I contribute to both a Roth IRA and Traditional IRA in 2026?

Yes. You can contribute to both, but the combined total cannot exceed $7,500 (or $8,600 if you are 50 or older).

Q4. What is the income limit for Roth IRA in 2026?

Single filers can fully contribute if income is below $153,000. The limit phases out up to $168,000. For married filing jointly, the phase-out is $242,000–$252,000.

Q5. What happens if I withdraw from a Traditional IRA early?

If you withdraw before age 59½, you pay a 10% early withdrawal penalty plus ordinary income taxes on the amount withdrawn.

Q6. Is there a Required Minimum Distribution (RMD) for Roth IRA?

No. Roth IRAs do not require minimum distributions during the owner’s lifetime, making them excellent for estate planning.

Q7. What is a Backdoor Roth IRA?

It is a legal strategy where high earners contribute to a Traditional IRA and then convert it to a Roth IRA to bypass the Roth income limits.

Q8. Can I lose money in an IRA?

Yes. IRA accounts are investment accounts, and the value can go up or down based on market performance. They are not insured like bank savings accounts.

Conclusion

The Roth IRA vs Traditional IRA debate does not have a single winner — it has a right answer for each person based on their unique financial situation. Both accounts are powerful retirement tools that offer significant tax advantages. The key is to start early, contribute consistently, and choose the account that aligns with your current and future tax situation.

If you are young and in a lower tax bracket today, the math strongly favors the Roth. If you are a high earner looking for an immediate tax break, the Traditional IRA delivers that benefit now. And if you want the best of both worlds, contributing to both accounts within the annual limit is a smart, flexible strategy.

Do not wait. Whether you choose a Roth IRA, a Traditional IRA, or both — the most important step is to start today and let your money grow.

If you’re also comparing safe investment options beyond retirement accounts, read our detailed guide on Fixed Deposit vs Mutual Fund to understand which investment is better for your financial goals.

Disclaimer

The information provided in this article about Roth IRA vs Traditional IRA is for educational and informational purposes only and does not constitute financial, tax, or investment advice. IRS rules, contribution limits, and income thresholds change periodically. Please consult a qualified financial advisor or tax professional before making any retirement account decisions. SK Smart Digital Hub is not responsible for any financial decisions made based on the information provided in this article.

Pingback: Best SIP Plan to Start Investing Now — Top 5 Picks for 2026