Every Indian investor has faced the same question at some point: should I put my money in a fixed deposit vs mutual fund? Your parents probably swear by fixed deposits. Your friends talk about SIPs and mutual fund returns. And you are stuck in the middle, not knowing which path leads to real financial growth.

The debate around fixed deposit vs mutual fund is not just about numbers. It is about your goals, your risk appetite, your time horizon, and your peace of mind. In 2025–26, this question matters more than ever. Indian stock markets have seen sharp volatility, foreign investors have pulled out billions, and Nifty 50 has been under pressure since its September 2024 peak. As a result, millions of Indian households are quietly moving money back into fixed deposits.

This complete guide breaks down fixed deposit vs mutual fund across every important parameter — returns, risk, liquidity, taxation, inflation, and real-world suitability — so you can make a smarter decision with your hard-earned money.

What Is a Fixed Deposit?

A fixed deposit (FD) is one of India’s oldest and most trusted investment instruments. You deposit a lump sum amount with a bank or NBFC for a fixed period, and the bank pays you a guaranteed interest rate throughout that tenure. Whether the stock market crashes or rallies, your FD return does not change.

As of June 2026, major Indian banks are offering the following FD interest rates:

SBI: Up to 6.40% for general citizens, up to 7.05% for senior citizens

HDFC Bank: Up to 6.50% for general citizens, up to 7.00% for senior citizens

ICICI Bank: Up to 6.50% for general citizens, up to 7.10% for senior citizens

Axis Bank: Up to 6.45% for general citizenship, up to 7.20% for senior citizens

Small Finance Banks: Up to 8.10% for general citizens, up to 8.75% for senior citizens

Fixed deposits are regulated and insured up to ₹5 lakh per depositor per bank by the Deposit Insurance and Credit Guarantee Corporation (DICGC). This makes them one of the safest investment options available in India.

What Is a Mutual Fund?

A mutual fund pools money from thousands of investors and invests it in a diversified portfolio of stocks, bonds, or other securities. Professional fund managers handle all investment decisions. Mutual funds are regulated by SEBI and offer multiple types — equity funds, debt funds, hybrid funds, and index funds.

“Mutual funds in India are regulated by the Securities and Exchange Board of India (SEBI), ensuring investor protection and fund transparency.”

Unlike a fixed deposit vs mutual fund comparison where FDs offer guaranteed returns, mutual fund returns depend entirely on market performance. However, this market linkage also gives mutual funds the potential to deliver significantly higher returns over the long term.

Fixed Deposit vs Mutual Fund: A Detailed Comparison

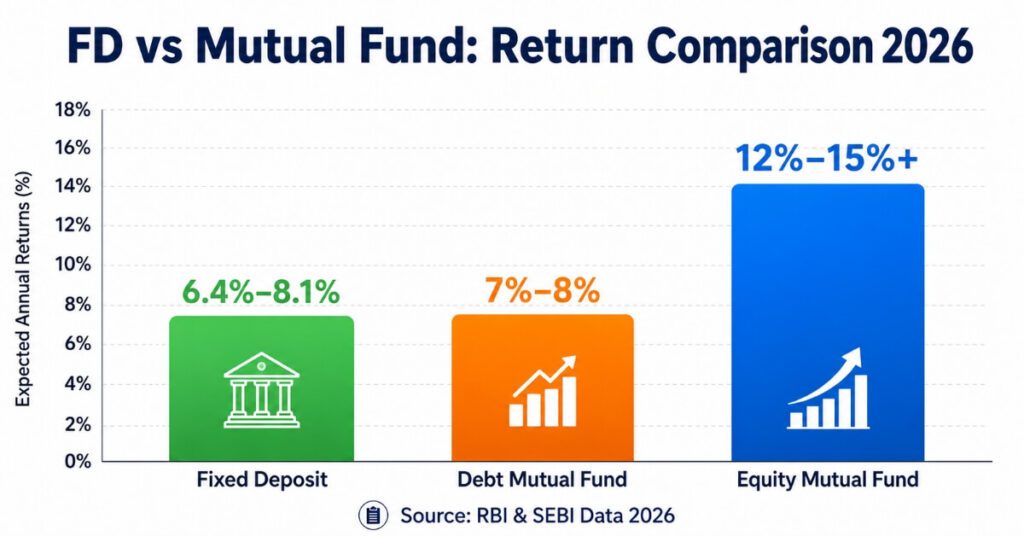

1. Returns

This is where the fixed deposit vs mutual fund debate gets most interesting.

Fixed deposits currently offer returns between 6.40% and 8.10% per annum depending on your bank and tenure. These returns are guaranteed and predictable.

Mutual funds, on the other hand, offer variable returns:

Debt mutual funds: Approximately 7%–8% per annum

Hybrid mutual funds: Approximately 9%–11% per annum

Equity mutual funds: Historically 12%–15%+ per annum over a 5–10 year period

The key difference in fixed deposit vs mutual fund returns is consistency vs potential. FDs give you certainty. Mutual funds give you possibility.

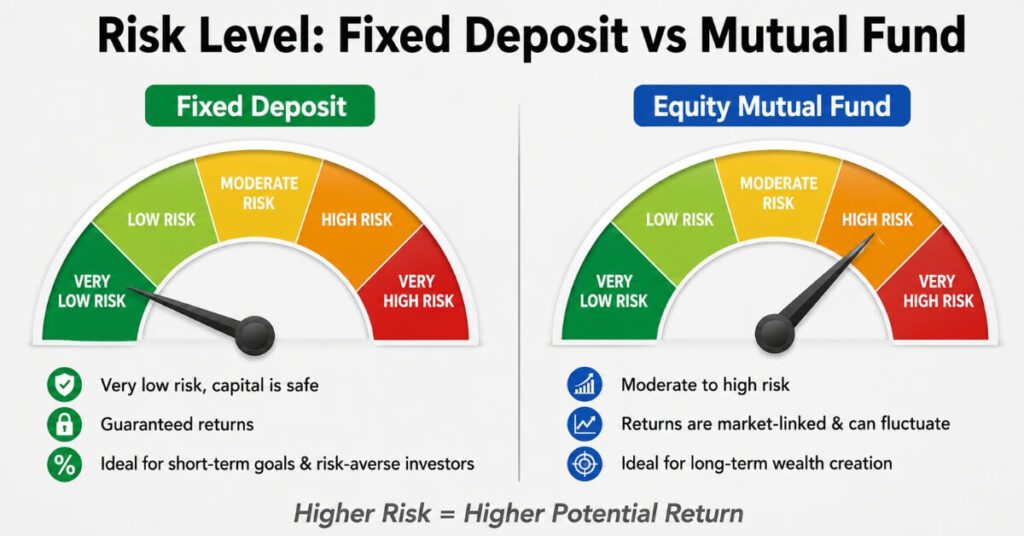

2. Risk

Fixed deposits carry virtually zero risk for amounts up to ₹5 lakh per bank. Your principal is safe, your interest is guaranteed, and your maturity amount is known from day one.

Mutual funds carry market risk. Equity mutual funds can fall 30%–40% during a market crash. Even debt funds can lose value if interest rates move unfavorably. When comparing fixed deposit vs mutual fund from a risk perspective, FDs are clearly the safer choice for capital protection.

However, it is important to understand that mutual funds hide short-term pain in exchange for long-term gain. Historically, every major market crash has been followed by a strong recovery for disciplined investors.

3. Liquidity

Fixed deposits are not completely liquid. Premature withdrawal attracts a penalty of 0.5%–1% on the applicable interest rate. For tax-saving FDs with a 5-year lock-in, premature withdrawal is not allowed at all.

Mutual funds (except ELSS funds with a 3-year lock-in) offer much better liquidity. Open-ended mutual funds can be redeemed within 1–3 business days. In the fixed deposit vs mutual fund liquidity battle, mutual funds clearly win.

4. Inflation Impact

India’s average inflation in 2025–26 has stayed around 5%–6%. If your FD is earning 6.40%, your real return after inflation is barely 1%–1.4%. After taxes, your real return may actually be negative.

This is the uncomfortable truth about fixed deposit vs mutual fund comparisons that most people ignore. Over a 10–15 year period, FD returns often fail to beat inflation meaningfully. Equity mutual funds, with long-term historical returns of 12%–15%, significantly outpace inflation and help build real wealth.

5. Taxation

Fixed deposit interest is added to your total income and taxed at your applicable income tax slab. If you are in the 30% tax bracket, you pay 30% tax on every rupee of FD interest earned. TDS of 10% is deducted at source if interest income exceeds ₹40,000 per year (₹50,000 for senior citizens) in a financial year.

Mutual fund taxation in the fixed deposit vs mutual fund comparison is more favorable for long-term investors:

Equity mutual funds (held over 1 year): 12.5% Long Term Capital Gains (LTCG) tax on gains above ₹1.25 lakh

Debt mutual funds: Taxed at slab rate (same as FD, post 2023 amendment)

ELSS funds: Tax deduction under Section 80C up to ₹1.5 lakh

For high-income earners, equity mutual funds offer a clear tax advantage in the fixed deposit vs mutual fund debate.

6. Investment Amount and Mode

Fixed deposits require a lump sum investment. Minimum amounts vary by bank but typically start at ₹1,000–₹10,000.

Mutual funds offer a Systematic Investment Plan (SIP), which allows you to invest as little as ₹100–₹500 per month. This makes mutual funds far more accessible for young investors and salaried professionals. In the fixed deposit vs mutual fund accessibility comparison, mutual funds score much higher.

Why Are Investors Moving Back to Fixed Deposits in 2025–26?

The news is not just numbers — it reflects a real psychological shift. According to RBI data, bank loans grew by 16.2% as of May 2026 while deposits grew by only 12.2%, creating a widening gap that has made deposit growth a banking priority.

Nifty 50, which hit a record high in September 2024, has since faced heavy selling by foreign institutional investors (FIIs). The rise in oil prices due to geopolitical tensions in West Asia and the growing dominance of AI-driven global markets have added to uncertainty. As a result, investment inflows into Indian equity mutual funds dropped to a three-year low.

Yes Bank CEO Vinay Tonse highlighted this shift, noting that Indian households are moving savings back into bank deposits amid high market risk. RBI data confirms this: commercial bank deposits grew 11.5% by March 2026, up from 10.6% in March 2025, with household savers contributing 59.3% of total deposits.

In the fixed deposit vs mutual fund choice right now, many risk-averse investors are consciously choosing the certainty of FDs over the uncertainty of equity markets.

Fixed Deposit vs Mutual Fund: Side-by-Side Summary Table

| Parameter | Fixed Deposit | Mutual Fund |

| Returns | 6.4%–8.1% (guaranteed) | 7%–15%+ (market-linked) |

| Risk | Very Low | Low to High |

| Liquidity | Moderate (penalty on early exit) | High (open-ended funds) |

| Inflation Beat | Rarely | Often (equity funds) |

| Taxation | Slab rate on interest | 12.5% LTCG (equity) |

| Minimum Investment | ₹1,000 lump sum | ₹100/month via SIP |

| Lock-in | Flexible (5yr for tax-saving) | 3yr for ELSS only |

| Ideal For | Conservative investors | Growth-oriented investors |

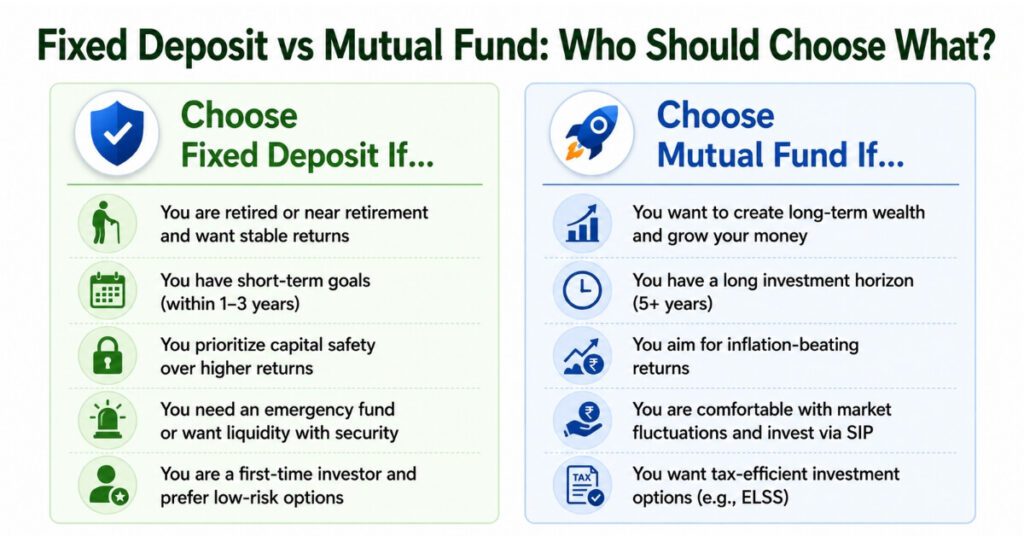

Who Should Choose a Fixed Deposit?

The fixed deposit vs mutual fund decision becomes clear once you know your financial profile. Choose a fixed deposit if:

You are retired or nearing retirement and need stable income

You have a short-term financial goal within 1–3 years (wedding, home down payment, emergency fund)

You cannot afford to lose any part of your principal

You are a first-time investor not yet comfortable with market fluctuations

You want to park your emergency fund safely

Who Should Choose a Mutual Fund?

In the fixed deposit vs mutual fund comparison, mutual funds are better suited if:

You have a long-term investment horizon of 5 years or more

You are building wealth for goals like retirement, child education, or buying a home a decade later

You can handle short-term market volatility without panic-selling

You want tax-efficient returns and the power of compounding

You are a young professional with regular income and monthly SIP capacity

The Smart Answer: You Do Not Have to Choose Just One

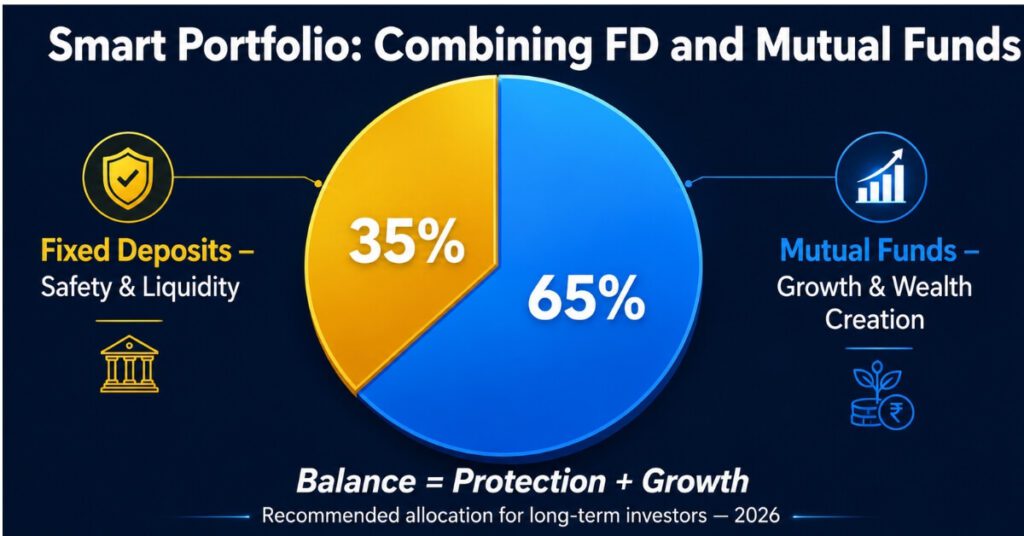

The wisest approach to fixed deposit vs mutual fund is not an either/or decision. Most seasoned financial planners recommend a balanced portfolio:

30%–40% in fixed deposits for capital safety, liquidity, and short-term needs

60%–70% in mutual funds (mix of equity and debt) for long-term wealth creation

This combination protects you during market downturns while also giving your money the opportunity to grow meaningfully over time. In the fixed deposit vs mutual fund framework, balance is always smarter than extremes.

5 Common Mistakes Investors Make in Fixed Deposit vs Mutual Fund Decisions

1. Investing all money in FDs and ignoring inflation

Many conservative investors park everything in FDs without realizing that after tax and inflation, their real returns are near zero or negative.

2. Chasing high mutual fund returns without understanding risk

New investors often jump into equity mutual funds at market peaks and panic-sell during corrections, locking in losses.

3. Ignoring the tax impact of FD interest

Fixed deposit interest is fully taxable each year. High-income earners pay up to 30% tax on FD returns, making the post-tax return significantly lower.

“Want to know how to report your FD interest income correctly while filing taxes? Read our complete guide on how to use Form 16 to file ITR.”

4. Treating ELSS mutual funds like regular equity funds

ELSS has a 3-year lock-in. Investors who need liquidity should not allocate emergency funds to ELSS just for tax benefits.

5. Not reviewing the fixed deposit vs mutual fund split annually

Your ideal allocation between FD and mutual funds changes as your income, goals, and risk appetite change. Annual portfolio reviews are essential.

Final Verdict: Fixed Deposit vs Mutual Fund in 2025–26

There is no single winner in the fixed deposit vs mutual fund debate. The right answer depends entirely on who you are as an investor.

If safety, certainty, and short-term goals define your financial life right now, fixed deposits are your best friend. If wealth creation, inflation-beating returns, and long-term financial independence are your goals, mutual funds — especially equity funds via monthly SIPs — are the better path.

In today’s volatile market environment, the smartest Indian investors are doing both: keeping some money safe in FDs while steadily building wealth through disciplined mutual fund SIPs. That is the true power of understanding fixed deposit vs mutual fund — and using both wisely.

Start with what you know. Build from there. And let your money work as hard as you do.

Frequently Asked Questions (FAQs)

Q1. Which is better — fixed deposit vs mutual fund for a beginner?

For a complete beginner, starting with a fixed deposit is safer because your principal is protected and returns are guaranteed. Once you understand basic investing concepts, you can gradually move into mutual funds through a monthly SIP starting as low as ₹500. The best approach is to keep 3–6 months of expenses in a fixed deposit as your emergency fund and invest the rest in mutual funds for long-term growth.

Q2. Is fixed deposit vs mutual fund a better option for senior citizens?

Senior citizens generally benefit more from fixed deposits because they need stable, predictable income after retirement. Most banks offer an additional 0.25%–0.50% interest to senior citizens on FDs, making current rates as high as 7.75% at major banks. However, a small allocation to conservative debt mutual funds can still help beat inflation for senior citizens with a longer financial horizon.

Q3. Can I lose money in a mutual fund but not in a fixed deposit?

Yes. In a fixed deposit, your principal is completely safe up to ₹5 lakh per bank (DICGC insurance). In equity mutual funds, your investment value can fall significantly during market downturns. However, historically, equity mutual funds have always recovered and delivered strong returns for investors who stayed invested for 7–10 years or more.

Q4. What is the minimum amount needed to start a fixed deposit vs mutual fund investment?

Fixed deposits typically require a minimum lump sum of ₹1,000–₹10,000 depending on the bank. Mutual funds can be started with as little as ₹100–₹500 per month through a SIP. This makes mutual funds far more accessible for young investors who want to start small and build wealth gradually.

Q5. Is fixed deposit interest taxable in India?

Yes. Fixed deposit interest is fully taxable at your income tax slab rate every financial year. If your total FD interest exceeds ₹40,000 per year (₹50,000 for senior citizens), the bank deducts TDS at 10%. If you are in the 30% tax bracket, your post-tax FD return can be significantly lower than the advertised interest rate, which makes equity mutual funds more tax-efficient for long-term investors.

Q6. Which is safer during a stock market crash — fixed deposit or mutual fund?

Fixed deposits are completely unaffected by stock market crashes. Your FD returns are locked in at the time of deposit and do not change regardless of what happens in the market. Equity mutual funds can lose significant value during a crash. This is why financial advisors recommend keeping at least a portion of your savings in fixed deposits as a safe anchor in your portfolio during volatile market conditions.

Q7. How does inflation affect fixed deposit vs mutual fund returns?

Inflation is the silent enemy of fixed deposit investors. With India’s inflation averaging 5%–6% in 2025–26, and FD rates at 6.4%–7%, your real return after inflation is very thin — and after tax, it may be near zero or negative. Equity mutual funds with historical returns of 12%–15% per annum over the long term are far better at protecting and growing your purchasing power against inflation.

Conclusion

The fixed deposit vs mutual fund debate does not have a single right answer — it has a right answer for you specifically, based on your financial goals, risk tolerance, and investment timeline.

Fixed deposits are your shield. They protect your capital, deliver guaranteed returns, and give you peace of mind during market uncertainty. In today’s volatile environment, with Indian markets under pressure and global geopolitical risks rising, it is completely rational to keep a solid portion of your savings in FDs.

Mutual funds are your engine. They give your money the power to grow, beat inflation, and build real long-term wealth. Through disciplined SIP investing, even small monthly amounts can compound into significant wealth over 10–15 years.

The smartest investors do not pick sides in the fixed deposit vs mutual fund debate. They use both. They protect what they need today with fixed deposits, and they grow what they will need tomorrow with mutual funds.

Start wherever you are comfortable. Review your portfolio every year. Increase your mutual fund allocation as your confidence and income grow. And always keep an emergency fund parked safely in a fixed deposit.

That is the real secret to winning the fixed deposit vs mutual fund game — not choosing one, but using both wisely.

Disclaimer

The information provided in this article about fixed deposit vs mutual fund is for educational and informational purposes only. It does not constitute financial, investment, or legal advice. Fixed deposit interest rates mentioned are indicative and subject to change by individual banks at any time. Mutual fund investments are subject to market risks. Past performance of mutual funds does not guarantee future returns. Please read all scheme-related documents carefully before investing. We strongly recommend consulting a SEBI-registered investment advisor or certified financial planner before making any investment decisions based on your personal financial situation.