You have debt. You want to pay it off. But every time you search for answers, you find two completely opposite strategies — the debt snowball vs avalanche debate. One says pay the smallest balance first. The other says attack the highest interest rate first. Both have passionate supporters. Both claim to be the best.

So which one should you choose?

In this complete guide, we break down the debt snowball vs avalanche comparison with real numbers, real psychology, and real examples — so you can finally make the right decision for your financial situation in 2026.

What Is the Debt Snowball Method?

Before we compare debt snowball vs avalanche, let’s understand each method clearly.

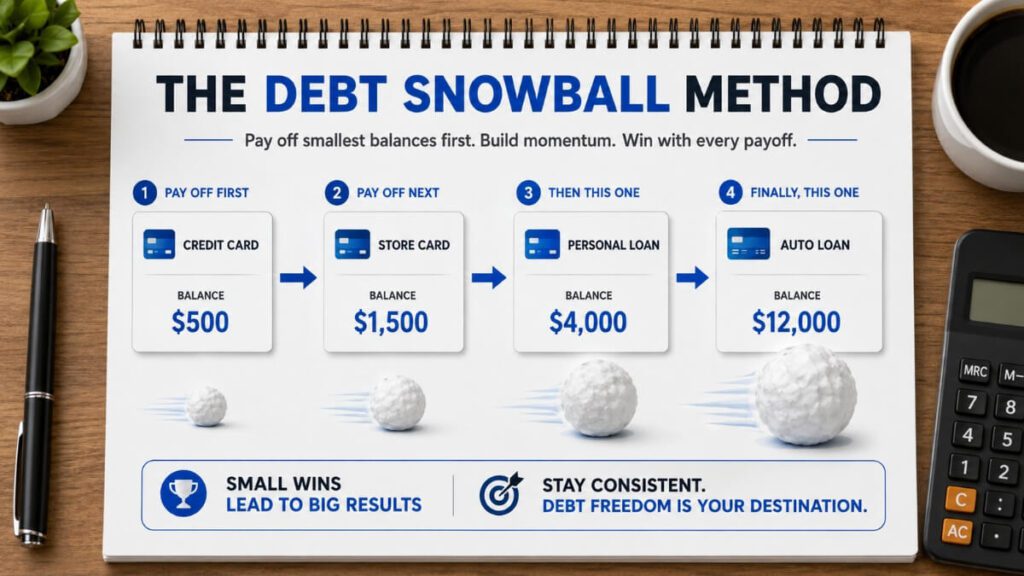

The debt snowball method was popularized by personal finance expert Dave Ramsey. The core idea is simple — pay off your smallest debt first, regardless of the interest rate.

Here is how the debt snowball works:

1 .List all your debts from smallest balance to largest balance

2 .Make minimum payments on all debts

3 .Put every extra dollar toward the smallest debt

4 .Once the smallest debt is paid off, roll that payment into the next smallest

Repeat until all debts are gone

Example of Debt Snowball:

| Debt | Balance | Interest Rate | Minimum Payment |

| Medical Bill | $500 | 0% | $25 |

| Credit Card A | $1,200 | 18% | $35 |

| Car Loan | $5,000 | 7% | $150 |

| Student Loan | $12,000 | 5% | $200 |

With the snowball method, you attack the $500 medical bill first — regardless of interest rates. Once that is gone, you take the $25 you were paying on it and add it to your credit card payment. Your Credit Card A payment becomes $60. When that is paid, you roll $60 into your car loan payment, making it $210. This rolling effect is exactly why it is called a snowball.

Why debt snowball works psychologically:

The biggest advantage of the debt snowball vs avalanche debate for snowball supporters is motivation. When you pay off that first small debt quickly, you get a powerful psychological win. You feel progress. You feel momentum. That feeling keeps you going through months or even years of debt repayment.

Research from Harvard Business Review found that people who use the debt snowball method are more likely to actually finish paying off all their debts — simply because the early wins keep them motivated.

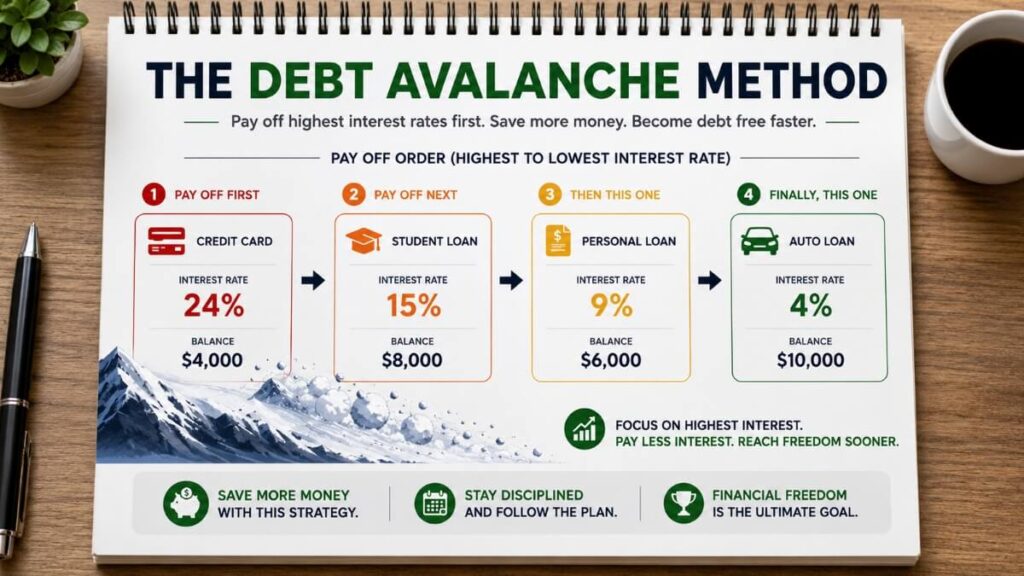

What Is the Debt Avalanche Method?

Now let us look at the other side of the debt snowball vs avalanche comparison.

The debt avalanche method is the mathematically superior strategy. Instead of focusing on balance size, it targets the interest rate. You pay off the highest interest rate debt first — saving you the maximum amount of money over time.

Here is how the debt avalanche works:

1 .List all your debts from highest interest rate to lowest

2 .Make minimum payments on all debts

3 .Put every extra dollar toward the highest interest rate debt

4 .Once paid off, roll that payment into the next highest rate

Repeat until debt-free

Example of Debt Avalanche:

Using the same debts as before, but now ranked by interest rate:

| Debt | Balance | Interest Rate | Minimum Payment |

| Credit Card A | $1,200 | 18% | $35 |

| Car Loan | $5,000 | 7% | $150 |

| Student Loan | $12,000 | 5% | $200 |

| Medical Bill | $500 | 0% | $25 |

With the avalanche method, you attack Credit Card A first because it has the 18% interest rate — even though it is not the smallest balance. This approach saves you significantly more money in total interest paid over the life of your debt repayment journey.

Why debt avalanche works mathematically:

In the debt snowball vs avalanche comparison, avalanche wins on pure numbers every single time. When you eliminate the highest interest rate debt first, you stop that debt from growing aggressively. Credit cards with 20% to 25% APR can literally double your debt if left unmanaged. The avalanche cuts off that expensive growth first.

According to the Federal Reserve, U.S. household credit card debt reached $1.21 trillion in 2025 — with average APRs above 20%. For anyone carrying high-interest credit card debt, the avalanche method can save hundreds or even thousands of dollars in interest payments.

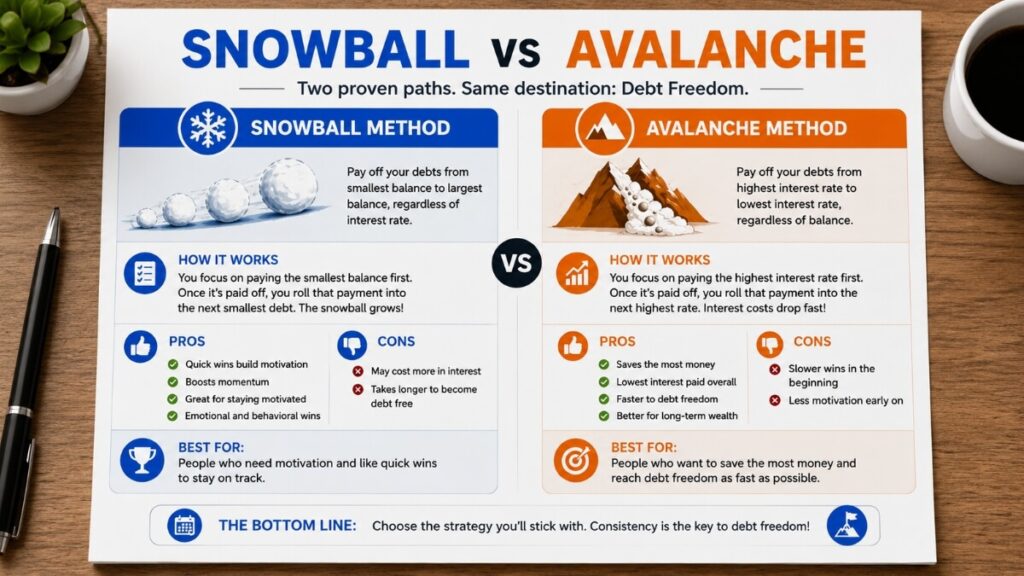

Debt Snowball vs Avalanche — Head to Head Comparison

Now let us put debt snowball vs avalanche directly side by side so you can see exactly how they differ.

| Factor | Debt Snowball | Debt Avalanche |

| Order of payoff | Smallest balance first | Highest interest rate first |

| Total interest paid | More | Less |

| Speed of payoff | Slower mathematically | Faster mathematically |

| Motivation level | Very high early on | Moderate — takes longer for first win |

| Best for | People who need motivation | Disciplined, math-focused people |

| Complexity | Very simple | Slightly more complex |

| Recommended by | Dave Ramsey | Most financial experts |

Real Numbers: Debt Snowball vs Avalanche

Let us use a real example to see exactly how debt snowball vs avalanche plays out with actual numbers.

“According to Fidelity’s debt payoff guide, the avalanche method saves more on interest but snowball method works better for people who need early motivation.”

Scenario: You have $600 extra per month to put toward debt payoff.

Your debts:

Credit Card: $3,000 at 22% APR, $60 minimum

Personal Loan: $2,000 at 14% APR, $50 minimum

Car Loan: $8,000 at 6% APR, $200 minimum

Student Loan: $15,000 at 4.5% APR, $250 minimum

Total minimums: $560/month

Extra money available: $40/month above minimums

Using Debt Snowball:

Attack Personal Loan ($2,000) first — smallest balance

Paid off in approximately 14 months

Then roll payment into Credit Card

Total interest paid: approximately $4,200

Total time to debt-free: approximately 52 months

Using Debt Avalanche:

Attack Credit Card ($3,000 at 22%) first — highest interest

Paid off in approximately 18 months

Then roll payment into Personal Loan

Total interest paid: approximately $3,100

Total time to debt-free: approximately 49 months

The difference: Avalanche saves approximately $1,100 in interest and gets you debt-free about 3 months faster. However, with snowball, you get your first debt paid off 4 months earlier — which can be a huge psychological boost.

This is the heart of the debt snowball vs avalanche debate — a real financial difference versus a real emotional difference.

Debt Snowball vs Avalanche: Which One Is Right for You?

The honest answer to the debt snowball vs avalanche question is — it depends entirely on who you are as a person.

Choose Debt Snowball if:

You have struggled to stick with debt payoff plans in the past

You need visible progress to stay motivated

You have many small debts that feel overwhelming

You are someone who gives up when results feel slow

Your debts have similar interest rates anyway

Choose Debt Avalanche if:

You are disciplined and can stay motivated without quick wins

You have one or two very high interest rate debts like credit cards above 20%

You are comfortable with math and spreadsheets

You have a stable income and a long-term mindset

Saving money on interest is your top priority

The debt snowball vs avalanche hybrid approach:

Many financial experts now suggest a hybrid approach — start with one or two small debts using the snowball method to get early wins and build confidence. Then switch to the avalanche method to eliminate your most expensive debts. This combination gives you the psychological boost of snowball and the financial efficiency of avalanche.

Common Mistakes When Choosing Between Debt Snowball vs Avalanche

Many people make critical errors when deciding between debt snowball vs avalanche. Here are the most common ones to avoid:

Mistake 1 — Choosing based on what sounds better, not what fits your personality

The best debt payoff method is not the one that saves the most money on paper. It is the one you will actually stick with. A person who quits the avalanche method after 3 months saves nothing. A person who completes the snowball method pays off everything — even if they paid a bit more in interest.

Mistake 2 — Not building an emergency fund first

Before choosing between debt snowball vs avalanche, make sure you have at least $1,000 in an emergency fund. Without it, one unexpected car repair or medical bill will send you straight back into new debt — destroying all your progress.

Mistake 3 — Ignoring minimum payments

Whether you choose debt snowball or avalanche, always make minimum payments on every debt first. Missing a minimum payment can trigger penalty rates and damage your credit score — making debt payoff even harder.

Mistake 4 — Not tracking progress

The debt snowball vs avalanche debate aside, tracking your progress is what keeps you going. Use a simple spreadsheet, a debt payoff app, or even a hand-drawn chart on paper. Seeing the numbers go down is powerful motivation regardless of which method you choose.

Mistake 5 — Forgetting about income

The fastest way to pay off debt — faster than any debt snowball vs avalanche strategy — is to increase your income. Even an extra $200 to $300 per month through a side hustle, freelance work, or overtime can cut your debt-free timeline by months or years.

If you are also working on building a debt-free life, make sure you understand your retirement benefits and tax planning so your savings stay protected long-term.

Debt Snowball vs Avalanche in 2026 — Why This Matters More Than Ever

The debt snowball vs avalanche decision matters more in 2026 than it ever has before.

Here is why:

U.S. household debt hit $18.8 trillion in Q4 2025 according to the New York Federal Reserve. Credit card APRs remain at historically high levels — most above 20%. The average American carries over $105,000 in total debt including mortgages, student loans, and credit cards.

In this environment, every dollar of interest you avoid paying is a dollar you keep. The debt snowball vs avalanche choice is not just a personal finance theory — it is a practical decision that can save thousands of dollars and years of your financial life.

At the same time, many people are struggling with debt fatigue — the feeling that no matter how hard you try, you are not making real progress. This is exactly where the psychological benefits of the debt snowball method become critically important. If motivation is your challenge, snowball wins. If interest savings are your priority, avalanche wins.

Step-by-Step: How to Start Your Debt Payoff Plan Today

Regardless of which side of the debt snowball vs avalanche debate you choose, here is how to start immediately:

Step 1 — List Every Debt

Write down every single debt you have. Include the creditor name, total balance, interest rate, and minimum monthly payment. Do not skip anything — even small medical bills or loans from family members.

Step 2 — Choose Your Method

Based on your personality, your motivation style, and your interest rates, decide between debt snowball vs avalanche. If your interest rates are all similar, go snowball. If you have one very high rate debt, consider avalanche.

Step 3 — Find Extra Money

Review your monthly budget. Cut subscriptions you do not use. Reduce dining out. Sell items you no longer need. Even finding an extra $100 per month can dramatically speed up both the snowball and avalanche methods.

Step 4 — Automate Minimum Payments

Set up automatic minimum payments on all debts immediately. This protects your credit score and prevents late fees while you focus your extra money on your target debt.

Step 5 — Attack Your Target Debt

Whether you chose debt snowball or avalanche, direct every extra dollar toward your target debt — smallest balance or highest interest rate respectively.

Step 6 — Celebrate Wins and Stay Consistent

Every time you pay off a debt in your debt snowball vs avalanche plan, celebrate it. Tell someone. Track it visually. The emotional acknowledgment of progress is what keeps people going through the long journey to becoming debt-free.

Frequently Asked Questions

Q1. Is debt snowball or avalanche better for beginners?

For beginners, the debt snowball method is generally better. The quick wins from paying off small debts first build the confidence and motivation needed to continue. Most beginners find the avalanche method too slow to see early results, which leads to giving up.

Q2. Does debt snowball vs avalanche affect credit score?

Both the debt snowball and avalanche methods improve your credit score over time. Paying off credit card balances reduces your credit utilization ratio — one of the biggest factors in your credit score. Both methods are equally good for credit improvement.

Q3. Can I switch from debt snowball to avalanche midway?

Yes, absolutely. Many people start with the snowball method for the early motivation boost, then switch to the avalanche method once they have eliminated a few small debts. This hybrid approach combines the best of both strategies.

Q4. What if I have only one debt?

If you only have one debt, the debt snowball vs avalanche comparison does not apply. Simply pay as much as possible above the minimum payment every month. The more you pay, the faster you become debt-free and the less interest you pay overall.

Q5. Which method does Dave Ramsey recommend?

Dave Ramsey strongly recommends the debt snowball method. He believes that personal finance is more about behavior than mathematics — and that the psychological wins from paying off small debts are more powerful than the interest savings from the avalanche method.

Conclusion

The debt snowball vs avalanche debate does not have one universal winner. The best method is the one you will actually complete. If you need motivation and visible wins, choose the debt snowball. If you are disciplined and want to save the maximum on interest, choose the debt avalanche. If you are somewhere in between, try the hybrid approach.

What matters most is not which method you choose — it is that you choose one and start today. Every day you delay costs you money in interest. Every payment you make brings you closer to financial freedom.

Start your debt snowball vs avalanche journey today. Your future self will thank you.

Disclaimer

This article is for informational and educational purposes only. It does not constitute professional financial advice. Please consult a certified financial advisor before making major debt management decisions. Individual results may vary based on income, debt amounts, interest rates, and personal financial circumstances.

Pingback: Debt Free Financial Freedom — 7 Steps to Build Real Wealth