Getting a personal loan sanctioned quickly depends on one number more than anything else, and that number is your credit history score. If you have ever wondered why some people get instant approval while others get rejected within minutes, the answer almost always comes down to the cibil score for personal loan approval. Banks and NBFCs use this three-digit number to decide whether you are a safe borrower or a risky one, and it directly affects your interest rate, loan amount, and processing speed.

In this article, we will break down exactly what cibil score for personal loan approval means, what range lenders expect, which factors affect it, and how you can improve it before you apply. Whether you are applying for the first time or have faced rejection before, understanding cibil score for personal loan approval can save you time, money, and unnecessary stress.

What Is CIBIL Score And Why Does It Matter

CIBIL stands for Credit Information Bureau (India) Limited, and it is one of the four RBI-licensed credit bureaus that track the borrowing and repayment behaviour of individuals across India. Your CIBIL score is a three-digit number ranging from 300 to 900 that reflects your creditworthiness based on your past loans, credit cards, EMIs, and repayment history.

When it comes to unsecured lending like personal loans, where there is no collateral involved, lenders rely heavily on this score to judge risk. This is exactly why the cibil score for personal loan approval carries so much weight in the entire application process. A higher score signals that you have handled credit responsibly in the past, while a lower score raises red flags for the lender.

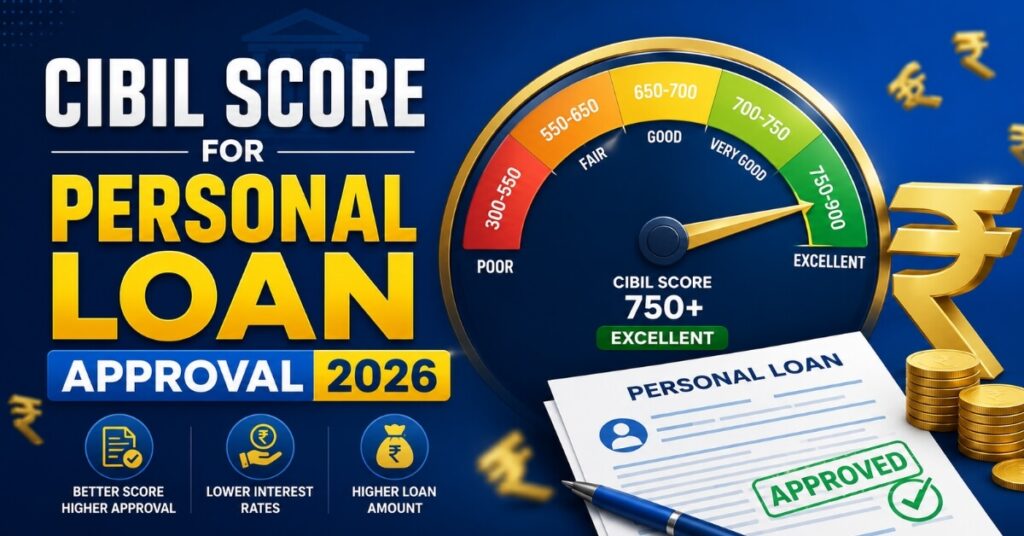

Ideal CIBIL Score Range For Personal Loan Approval

Most banks and NBFCs in India follow a fairly consistent pattern when evaluating the cibil score for personal loan approval. Here is a general breakdown of how lenders typically view different score ranges:

750 and above: This is considered an excellent score. A cibil score for personal loan approval in this range usually results in fast approval, the lowest available interest rates, and access to higher loan amounts.

700 to 749: This is a good score. Most lenders will approve your application, though you may not always get the most competitive interest rate.

650 to 699: This is considered an average score. Approval is still possible, but lenders may ask for additional documentation, a co-applicant, or offer a smaller loan amount at a higher interest rate.

Below 650: This is a weak score. Getting the cibil score for personal loan approval in this range accepted becomes difficult, and many lenders may reject the application outright or refer you to specialised high-risk lending products.

It is worth noting that different banks set their own internal cut-offs, so the exact threshold for cibil score for personal loan approval can vary slightly from one lender to another. However, 750 is widely accepted as the benchmark for a smooth and hassle-free approval experience.

Why Lenders Focus So Heavily On This Score

Unlike a home loan or a car loan, a personal loan does not require you to pledge any asset as security. This means that if a borrower defaults, the lender has no direct way to recover the money through collateral. Because of this risk, the cibil score for personal loan approval becomes the single most important tool lenders use to estimate the probability of timely repayment.

A strong score tells the lender that you have a track record of paying EMIs and credit card bills on time. A weak score, on the other hand, suggests missed payments, high credit utilisation, or a history of loan defaults. This is why even applicants with a stable income can get rejected if their cibil score for personal loan approval does not meet the lender’s internal policy.

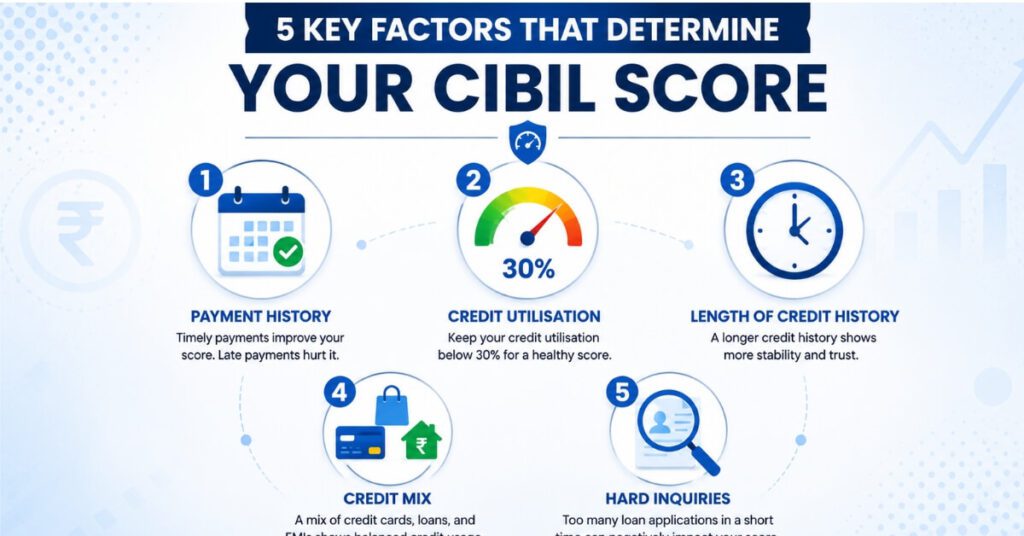

Factors That Influence Your CIBIL Score

Several factors work together to determine your cibil score for personal loan approval, and understanding them can help you take corrective action well in advance.

Payment history: This is the single biggest factor. Late payments, missed EMIs, or credit card dues that are not cleared on time can significantly damage your credit score.

Credit utilisation ratio: This refers to how much of your available credit limit you are using. Keeping your utilisation below 30 percent is generally recommended if you want a healthy score.

Length of credit history: A longer track record of responsible borrowing tends to improve your score, since it gives lenders more data to evaluate.

Credit mix: Having a healthy combination of secured loans, such as a home loan, and unsecured credit, such as credit cards, can positively influence your score.

Number of hard inquiries: Every time you apply for a new loan or credit card, the lender performs a hard inquiry, which can temporarily lower your score. Applying for multiple loans within a short period can hurt your score.

Outstanding debt: The total amount you currently owe across all loans and credit cards also plays a role. High existing debt relative to your income can make lenders cautious even if your score looks reasonable on paper.

How To Check Your CIBIL Score Before Applying

Before submitting a loan application, it is a smart practice to check your cibil score for personal loan approval on your own. You are entitled to one free credit report every calendar year directly from CIBIL’s official website. Several banks and financial platforms also offer free score checks as part of their services.

Reviewing your report before applying gives you a chance to spot errors, such as loans that were closed but still show as active, or payments that were recorded incorrectly. Disputing and correcting these errors in advance can meaningfully improve your cibil score for personal loan approval and increase your chances of getting approved on the first attempt.

Documents Usually Required Along With Your Score

Even with a strong score, lenders will still ask for a standard set of documents to verify your identity, income, and address. These typically include a PAN card, an Aadhaar card or another valid identity proof, recent salary slips or income tax returns for self-employed applicants, the last three to six months of bank statements, and a passport-size photograph. Salaried applicants may also need to submit an employment certificate, while self-employed individuals are often asked for business proof and audited financial statements.

Keeping these documents ready in advance not only speeds up the approval process but also reduces the chances of your application being delayed or sent back for clarification. Many digital lenders now allow you to upload documents online, which has made the overall process considerably faster compared to a few years ago.

Common Mistakes Applicants Make

Even applicants with a decent score sometimes get rejected or receive unfavourable terms because of avoidable mistakes. One common error is applying for a loan amount that is far higher than what your income can comfortably support, which makes lenders nervous about your repayment capacity regardless of your score. Another mistake is not comparing offers across multiple banks and NBFCs before applying, which can mean missing out on a lower interest rate or better repayment terms.

Some applicants also overlook their existing EMI obligations when applying for a new loan, not realising that lenders calculate a fixed obligation to income ratio before approving any new credit. If your existing EMIs already take up a large portion of your monthly income, even a good score may not be enough to secure approval for the full amount you are requesting.

Finally, many people submit incomplete or mismatched documents, such as an address on the application that does not match the address proof submitted, which can lead to unnecessary delays or outright rejection. Taking a few extra minutes to double-check your application before submitting it can save weeks of back-and-forth with the lender.

How Your Score Affects Interest Rates

It is a common misconception that approval is the only thing at stake. In reality, your score also has a direct impact on the interest rate you are offered. Applicants with excellent scores are typically rewarded with the lowest possible rates, since lenders view them as low-risk borrowers. Those with average scores may still get approved, but often at a noticeably higher rate, which can add up to a significant amount over the full tenure of the loan.

For example, a difference of just two or three percentage points on a large loan amount spread over several years can translate into tens of thousands of rupees in additional interest paid. This is one of the most practical reasons to work on your score before applying, rather than after receiving an unfavourable offer. Even a short delay of a few months to bring your score up can result in meaningful long-term savings.

Prepayment and Foreclosure Considerations

Once your loan is approved, maintaining discipline does not stop there. Making prepayments whenever you have surplus funds, or opting for foreclosure once you can afford to clear the outstanding balance, can further strengthen your long-term credit profile. Lenders view a track record of responsible loan closure positively, which can make future borrowing, whether for a car, a home, or any other need, considerably smoother.

It is also worth checking whether your lender charges any prepayment or foreclosure penalty, since some loans carry additional charges for early repayment. Reading the fine print before signing the loan agreement can help you avoid unexpected costs down the line.

How Lenders Evaluate Your Overall Application

While your score plays a central role, lenders also look at a combination of factors together before making a final decision. Your monthly income, job stability or business continuity, existing debt obligations, age, and even your city of residence can all influence the final outcome. Salaried employees working with well-established companies are often viewed more favourably than those in newer or less stable organisations, simply because of the perceived security of income.

Self-employed applicants, on the other hand, may need to demonstrate consistent business income over at least the past two to three years through income tax returns and bank statements. This is why two applicants with an identical score can sometimes receive very different loan offers, depending on how the rest of their financial profile stacks up.

Tips To Improve Your CIBIL Score For Personal Loan Approval

If your current score falls short of what lenders expect, there are practical steps you can take to strengthen your cibil score for personal loan approval over time.

Pay EMIs and credit card bills on time, every single time. Even one missed payment can stay on your report and affect your credit score for months.

Keep your credit utilisation low by not maxing out your credit cards. Paying off balances in full each month rather than carrying them forward is one of the fastest ways to strengthen your cibil score for personal loan approval.

Avoid applying for multiple loans or credit cards in a short span of time. Each hard inquiry adds a small dent, and too many inquiries together can hurt your score more than a single one would.

Do not close old credit accounts unnecessarily. A longer credit history generally works in your favour when lenders assess your creditworthiness.

Keep a healthy mix of credit types instead of relying only on unsecured borrowing. This balance can gradually support a stronger cibil score for personal loan approval over the long term.

Monitor your credit report periodically so that any inaccurate entries can be corrected before they damage your score further.

What Happens If Your Score Is Too Low

If your cibil score for personal loan approval does not meet a lender’s minimum requirement, you still have a few options. Some NBFCs and digital lenders cater specifically to applicants with lower scores, though usually at a higher interest rate. Adding a co-applicant with a strong credit history can also improve your chances. In some cases, opting for a smaller loan amount or a secured loan against a fixed deposit may be a more realistic path until your score improves.

Rather than applying to multiple lenders at once out of desperation, which can further lower your score through repeated hard inquiries, it is generally better to pause, work on the factors mentioned above, and reapply after a few months once your score has recovered.

How This Fits Into Your Broader Financial Picture

Your cibil score for personal loan approval does not exist in isolation. It reflects your overall financial discipline, which also affects how you handle market-linked investments and unexpected events. For instance, during periods of economic uncertainty, such as the one covered in our detailed report on the share market crash 2026, having a strong credit profile and low existing debt gives you far more flexibility to manage your finances without relying on high-interest borrowing. A good cibil score for personal loan approval essentially acts as a financial safety net that keeps your options open even when circumstances change.

For an authoritative and official explanation of how credit scores are calculated and regulated in India, you can refer to the Reserve Bank of India, which oversees credit bureau operations and lending norms across the country.

Frequently Asked Questions

Q1.What is the minimum CIBIL score for personal loan approval?

Most banks and NBFCs prefer a minimum of 700, though a score of 750 or above is considered ideal for a smooth cibil score for personal loan approval experience with better interest rates.

Q2.Can I get a personal loan with a CIBIL score below 650?

It is possible but difficult. Some digital lenders and NBFCs may still approve your application, but usually at a higher interest rate and with stricter terms.

Q3.How long does it take to improve a CIBIL score?

Depending on your financial habits, noticeable improvement can take anywhere from three to six months of consistent, on-time payments and responsible credit usage.

Q3.Does checking my own CIBIL score lower it?

No. Checking your own score is considered a soft inquiry and does not impact your cibil score for personal loan approval in any way.

Q4.Does income affect my CIBIL score?

Income itself is not a direct factor in your CIBIL score, but it does influence the loan amount a lender is willing to approve alongside your score.

Q5.How often should I check my CIBIL score?

It is a good practice to check your score at least once every few months, especially before applying for any new credit, so you know where you stand for a cibil score for personal loan approval evaluation.

Conclusion

A strong cibil score for personal loan approval can make the difference between a quick, hassle-free approval and a frustrating rejection. By understanding what lenders look for, keeping track of the factors that influence your score, and following consistent financial habits like timely repayments and low credit utilisation, you can steadily build a score that works in your favour.

Whether you are applying for the first time or trying to recover from a low score, small, consistent actions over a few months can significantly improve your cibil score for personal loan approval and open the door to better loan terms in the future.

Disclaimer

This article is intended for general informational purposes only and should not be considered financial or legal advice. CIBIL scores, lending criteria, and interest rates are subject to change and vary by lender. Readers are advised to consult a certified financial advisor or their respective bank before making any borrowing decisions.

Pingback: Why Gold Price Is Falling: 6 Shocking Reasons Explained"