Introduction

Kya aap 2026 mein apna sapna ghar khareedne ka plan kar rahe hain? Agar haan, toh sabse pehla sawaal jo dimaag mein aata hai woh yeh hai — home loan interest rates 2026 India mein abhi kitni hain? Kya yeh rates aur gireingi? Kaunsa bank sabse best deal de raha hai? Aur kya 2026 sach mein ghar khareedne ka sahi waqt hai?

Yeh sawaal sirf curiosity ke liye nahi hain — ek chhoti si interest rate ka farq aapki poori financial planning badal sakta hai. Sochiye — 0.50% ka farq ₹50 lakh ke loan par 20 saalon mein lagbhag ₹6-7 lakh ka farak laata hai. Isliye home loan interest rates 2026 India ko samajhna bahut zaroori hai.

Achi khabar yeh hai ki 2026 mein home loan interest rates India mein clearly improvement aaya hai. 2022-2024 ke mukable mein rates neeche aa rahi hain. RBI ka stance positive hai aur banks ke beech competition bhi badh raha hai — jo ultimately aap jaise borrowers ke liye benefit hai.

Is article mein hum detail mein cover karenge — current rates kya hain, kaun se banks best hain, EMI kaise calculate karein, tax benefits kaise milenge, aur aapko 2026 mein home loan lena chahiye ya nahi. Toh shuru karte hain!

Home Loan Interest Rates 2026 India — Current Situation

2022 se lekar 2024 tak RBI ne inflation control karne ke liye repo rate ko aggressively badhaya. Iska seedha asar home loan interest rates India par pada aur rates 9% se bhi upar chali gayi thi. Lekin ab scenario badal raha hai.

2025 ke end se RBI ne rate cut karna shuru kiya aur 2026 mein yeh trend continue hai. Abhi home loan interest rates 2026 India ka overview kuch aisa hai:

Floating Rate Home Loans: 8.25% se 9.50% per annum (bank aur profile ke hisaab se)

Fixed Rate Home Loans: 9.00% se 10.50% per annum

Women Applicants Ke Liye: Additional 0.05% se 0.10% concession

Latest RBI Repo Rate 2026 — Apni EMI Par Impact Samjho

Experts ka maanna hai ki 2026 mein ek ya do aur rate cuts ho sakti hain. Matlab home loan interest rates 2026 India abhi jo hain ussse bhi thodi aur neeche aa sakti hain — jo current borrowers ke liye aur bhi achhi khabar hai agar unhone floating rate loan liya hua hai.

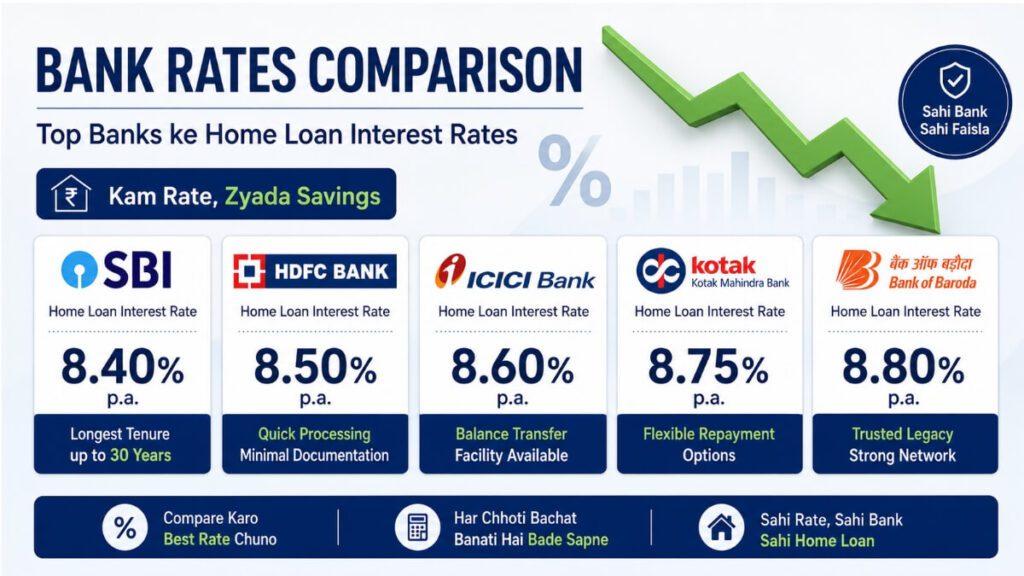

Top Banks Ki Home Loan Interest Rates 2026 India

Neeche top 5 banks ki home loan interest rates 2026 India di gayi hain. Yeh rates indicative hain — aapki actual rate aapke CIBIL score, loan amount, aur income par depend karegi:

1. SBI Home Loan Interest Rate 2026

State Bank of India India ka sabse bada aur trusted bank hai. SBI ki home loan interest rates 2026 mein approximately 8.25% – 8.75% per annum hain. SBI ka “Flexipay” option young borrowers ke liye popular hai jisme starting years mein EMI thodi kam hoti hai aur baad mein badhti hai — jab income bhi badh chuki hoti hai. Government bank hone ki wajah se SBI reliable aur stable option hai.

2. HDFC Bank Home Loan Rate 2026

HDFC Bank private sector ka sabse bada home loan provider hai. Home loan interest rates 2026 India mein HDFC ki rates approximately 8.40% – 9.10% per annum hain. HDFC ka digital application process bahut smooth hai aur approval fast hota hai. Unka customer service bhi kaafi acha maana jaata hai.

3. ICICI Bank Home Loan Rate 2026

ICICI Bank bhi competitive home loan interest rates 2026 India offer kar raha hai — approximately 8.40% – 9.25% per annum. ICICI ka “Step Up Home Loan” un young professionals ke liye acha hai jinki income aane wale saalon mein badhne wali hai. Balance transfer facility bhi ICICI mein convenient hai.

4. Kotak Mahindra Bank Home Loan 2026

Kotak Mahindra Bank ki home loan interest rates 2026 approximately 8.65% – 9.50% per annum hain. Yeh un borrowers ke liye achi choice hai jinhe quick processing chahiye. Kotak ka digital-first approach aur minimal documentation unhe younger borrowers mein popular banata hai.

5. Bank of Baroda Home Loan Rate 2026

Government bank hone ke fayde ke saath Bank of Baroda ki home loan interest rates 2026 India approximately 8.30% – 8.90% per annum hain. Long tenure options aur affordable rates ki wajah se yeh middle-class borrowers ke beech popular choice hai.

Smart Tip: Sirf interest rate mat dekho — processing fee, prepayment charges, aur customer service bhi compare karo.

Home Loan Interest Rates 2026 India Ko Affect Karne Wale Factors

Aapko jo actual home loan interest rate milegi woh kai factors par depend karti hai:

CIBIL Score — Sabse Important Factor

CIBIL score 750 ya usse upar hone par aapko best available home loan interest rates 2026 India milti hain. 700-749 ke beech thoda zyada rate lagti hai aur 650 se neeche application reject bhi ho sakti hai. Loan apply karne se pehle apna CIBIL score zaroor check karo.

Loan Amount Aur LTV Ratio

Loan-to-Value ratio jitna kam hoga — matlab aap jitna zyada down payment denge — utni better home loan interest rate milne ke chances hain. Banks kam LTV wale loans mein kam risk dekhte hain.

Employment Type

Salaried employees ko generally self-employed logon se better home loan interest rates India milti hain. Iska reason hai stable aur predictable income. Self-employed logon ko kuch additional documents aur thodi zyada rate face karni pad sakti hai.

Loan Tenure

Shorter tenure loans mein bank ka risk kam hota hai — isliye kuch cases mein slightly better rate mil sakti hai. Lekin EMI zyada hoti hai. Apni repayment capacity ke hisaab se tenure decide karo.

Women Borrower Benefit

Agar property women ke naam par hai ya women co-applicant hain, toh home loan interest rates 2026 mein 0.05% – 0.10% ki extra chhoot milti hai. Yeh chhoti percentage lagti hai lekin 20 saal mein yeh significant saving ban jaati hai.

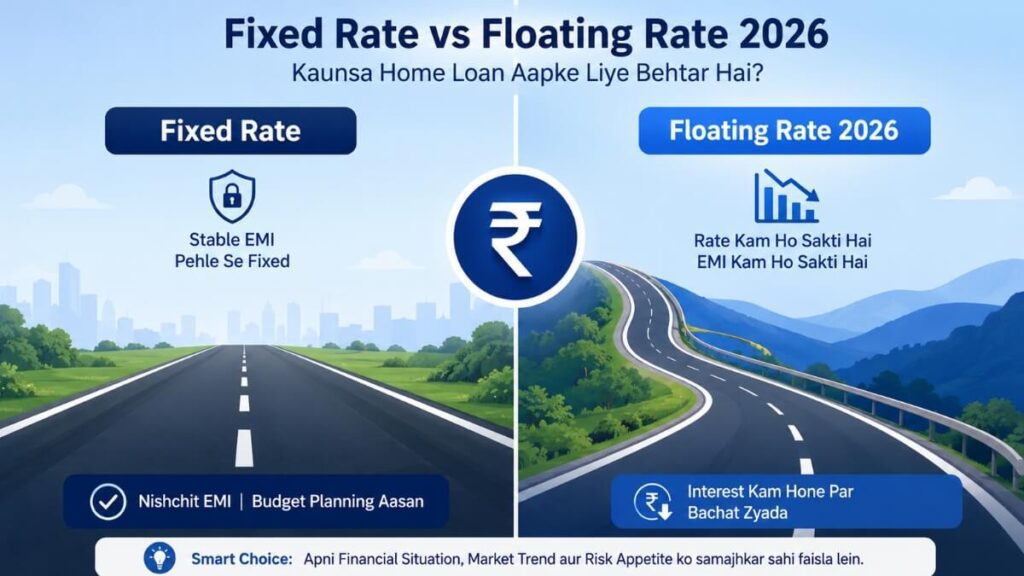

Fixed vs Floating Home Loan Interest Rate — 2026 Mein Kya Chunein?

Home loan interest rates 2026 India ke current trend ko dekhte hue yeh decision bahut important hai:

Fixed Rate Ke Fayde Aur Nuksan

Fixed rate mein poore tenure tak ek hi rate rehti hai. EMI predictable hoti hai — budgeting aasaan ho jaati hai. Nuksan yeh hai ki agar future mein home loan interest rates India aur girein, toh aap us benefit ka faida nahi utha paoge. Fixed rate generally floating se 0.5% – 1% zyada hoti hai.

Floating Rate Ke Fayde Aur Nuksan

Floating rate RBI ke repo rate ke saath change hoti hai. Abhi floating home loan interest rates 2026 India fixed se kam hain. Sabse bada faida — agar RBI aur rate cuts kare (jo 2026-27 mein expected hai), toh aapki EMI automatically kam ho jaayegi. Nuksan — agar rates badhen toh EMI bhi badhegi.

2026 Mein Recommendation

Floating rate lo — kyunki:

1 .Abhi rates already neeche aa rahi hain

2 .Experts ka maanna hai aur cuts hone ki possibility hai

3 .Floating par RBI ne prepayment penalty band ki hai

4 .Fixed se kam rate abhi available hai

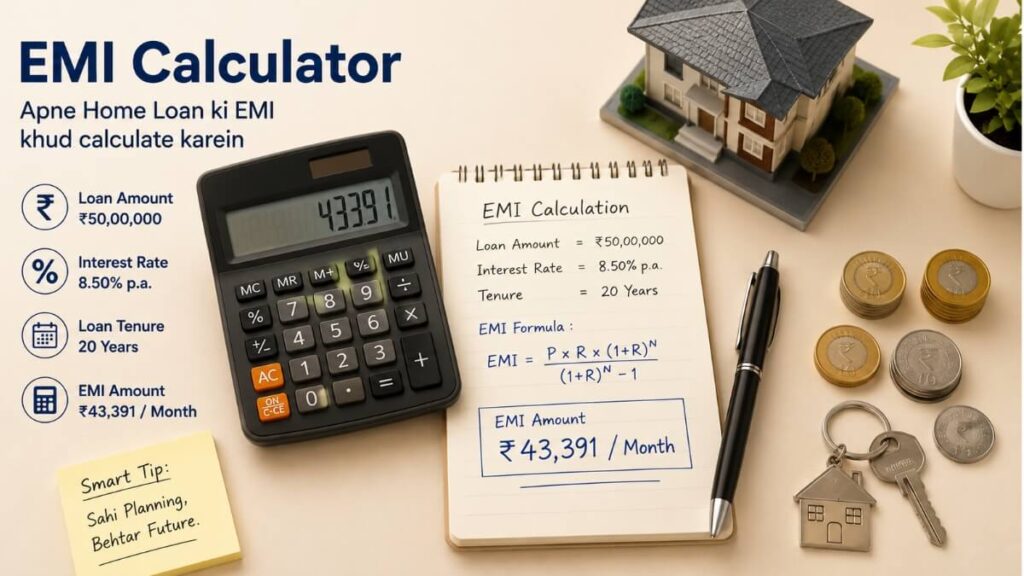

EMI Calculation — Home Loan Interest Rates 2026 India Ka Real Impact

Home loan interest rates 2026 India ka actual impact samjhne ke liye ek practical example:

Scenario A — Current Rate 8.50%:

Loan Amount: ₹50,00,000

Interest Rate: 8.50% p.a.

Tenure: 20 years

Monthly EMI: ₹43,391

Total Interest Payable: ₹54,13,840

Total Amount Payable: ₹1,04,13,840

Scenario B — 2023 Peak Rate 9.50%:

Loan Amount: ₹50,00,000

Interest Rate: 9.50% p.a.

Tenure: 20 years

Monthly EMI: ₹46,607

Total Interest Payable: ₹61,85,680

Total Amount Payable: ₹1,11,85,680

Sirf 1% rate ka fark = ₹7.71 lakh ki extra interest + ₹3,216 zyada EMI har mahine!

Isliye home loan interest rates 2026 India mein sahi time par apply karna itna zaroori hai.

Home Loan Tax Benefits 2026 India

Home loan interest rates 2026 India ke saath tax benefits bhi ek important angle hai — especially Old Tax Regime mein:

Section 80C — Principal Repayment

Home loan ki principal repayment par ₹1.5 lakh tak annual deduction milti hai. Yeh ₹1.5 lakh limit mein PPF, ELSS, life insurance premium sab share karte hain.

Section 24(b) — Interest Deduction

Self-occupied property par home loan ki interest payment mein se ₹2 lakh tak annual deduction milti hai. Agar property let-out hai toh actual interest deduction milti hai bina kisi limit ke.

Section 80EEA — First Time Buyer Benefit

First time home buyers ke liye additional ₹1.5 lakh interest deduction available hai — lekin conditions hain. Property ki stamp duty value ₹45 lakh se zyada nahi honi chahiye aur aapke paas pehle se koi property nahi honi chahiye.

Important Note: New Tax Regime mein yeh deductions available nahi hain. Apne CA se pehle discuss karo ki konsa regime aapke liye better hai home loan interest rates 2026 India ke saath

Tax benefits ka poora faida uthane ke liye sahi tarike se ITR file karna zaroori hai. Agar aapko process nahi pata toh hamara yeh guide padho — Home Loan par Tax Benefit Kaise Milega — Pehle ITR Filing Samjho”.

Home Loan Balance Transfer — Smart Move 2026 Mein

Agar aapne 2022-2024 mein high home loan interest rate par loan liya tha, toh balance transfer aapke liye ek game changer ho sakta hai.

Balance transfer matlab apna existing loan ek bank se doosre bank mein shift karna jahan home loan interest rates 2026 India kam hain.

Balance Transfer Kab Karein?

Naye bank ki rate aapki current rate se 0.50% – 1% kam ho

Loan abhi early stage mein ho (pehle 7-8 saal) — jab interest component zyada hota hai

CIBIL score original loan ke baad improve hua ho

Naya bank better top-up loan ya features offer kar raha ho

Balance Transfer Ka Process

Naye bank mein apply karo aur sanction letter lo. Purane bank se foreclosure letter request karo. Purana bank NOC aur property documents issue karta hai. Naya bank outstanding amount pay karta hai aur aapka loan shift ho jaata hai.

Dhyan rakho: Balance transfer mein bhi processing fee lagti hai — 0.5% se 1% tak. Pehle calculate karo ki net saving positive hai ya nahi.

Home Loan Apply Karte Waqt Yeh Galtiyan Mat Karna

Home loan interest rates 2026 India research karte waqt log sirf rate dekhte hain lekin yeh common mistakes bhi karte hain:

Galti 1 — Processing Fee Ignore Karna

Kuch banks low home loan interest rate dete hain lekin high processing fee lete hain. Net comparison karo.

Galti 2 — Sirf Ek Bank Mein Apply Karna

Kam se kam 3-4 banks se quotes lo. Home loan interest rates 2026 India mein competition ki wajah se banks negotiate bhi karte hain.

Galti 3 — CIBIL Check Kiye Bina Apply Karna

Baar baar rejection se CIBIL score aur girata hai. Pehle self-check karo, phir apply karo.

Galti 4 — Insurance Bundling Accept Karna

Banks loan ke saath insurance attach karte hain. Yeh optional hoti hai — alag se lena generally sasta padta hai.

Galti 5 — Total Cost Calculate Na Karna

Sirf EMI mat dekho. 20 saal mein total interest outgo dekhna zaroori hai — tab sahi picture samjhegi.

Zarori Documents — Home Loan Ke Liye

Home loan interest rates 2026 India mein best deal milne ke baad process smooth rakhne ke liye yeh documents ready rakho:

Identity Proof: Aadhaar Card, PAN Card

Address Proof: Utility bill, Aadhaar, Voter ID

Income Proof: Last 3 months salary slips, Form 16 (salaried ke liye); Last 2 years ITR with computation (self-employed ke liye)

Bank Statements: Last 6 months

Property Documents: Sale agreement, title deed, approved building plan

CIBIL Report: Pehle self-check kar lo

2026 Mein Home Loan Lena Chahiye Ya Wait Karein?

Yeh sabse common dilemma hai home loan interest rates 2026 India ke context mein. Jawab clearly hai — haan, 2026 ek reasonably good time hai.

Reason 1: Rates 2023-24 ke peak se already neeche aa chuki hain — 9.5% se ab 8.25% tak.

Reason 2: Floating rate chunne par future rate cuts ka bhi automatic benefit milega.

Reason 3: Property prices badhte ja rahe hain. Rate thodi aur girne ka wait karoge toh property price bhi badh jaayegi — net benefit zero ya negative bhi ho sakta hai.

Reason 4: Agar aapka CIBIL score acha hai, income stable hai, aur down payment ready hai — toh delay ka koi strong reason nahi hai.

Ek hi case mein wait karo: Agar aapka CIBIL score 700 se neeche hai — pehle 6 mahine score improve karo, phir apply karo. Better home loan interest rates 2026 India milegi aur rejection ka risk bhi nahi rahega.

Frequently Asked Questions (FAQs) — Home Loan Interest Rates 2026 India

Q1. 2026 mein home loan interest rates India mein kitni hain?

2026 mein home loan interest rates 2026 India mein floating rate 8.25% se 9.50% per annum ke beech hain — bank aur aapki credit profile ke hisaab se. Fixed rate 9.00% se 10.50% per annum tak hai. SBI sabse competitive rate 8.25% se offer kar raha hai abhi.

Q2. Kaunsa bank 2026 mein sabse kam home loan interest rate de raha hai?

Abhi home loan interest rates 2026 India mein SBI ki starting rate 8.25% p.a. sabse competitive hai. Uske baad Bank of Baroda 8.30% aur HDFC, ICICI 8.40% se shuru karte hain. Lekin aapki actual rate aapke CIBIL score aur income par depend karegi — isliye multiple banks compare karna zaroori hai.

Q3. Home loan ke liye minimum CIBIL score kitna hona chahiye?

Zyada tar banks home loan approve karne ke liye minimum 700 CIBIL score maangte hain. Lekin home loan interest rates 2026 India mein best rate ke liye 750+ score hona chahiye. 750 se upar score wale borrowers ko generally 0.25% – 0.50% better rate milti hai.

Q4. Fixed aur floating rate mein se 2026 mein kya better hai?

2026 mein floating rate better choice hai. Kyunki rates already neeche aa rahi hain aur RBI ke aur rate cuts ki possibility hai — floating rate mein aap automatically is benefit ka faida uthao ge. Fixed rate sirf tab sahi hai jab aapko EMI stability chahiye aur aap rate movement se bilkul protect rehna chahte ho.

Q5. Kya 2026 mein home loan lena sahi decision hai?

Haan, 2026 ek reasonable time hai home loan lene ke liye. Home loan interest rates 2026 India 2023-24 ke peak se kaafi neeche aa chuki hain. Property prices bhi badh rahi hain — isliye rate aur girne ka wait karna financially wise nahi ho sakta. Agar CIBIL score 750+ hai, income stable hai aur down payment ready hai — toh abhi apply karo.

Q6. Home loan par kitni tax saving ho sakti hai?

Old Tax Regime mein home loan par maximum tax saving is tarah ho sakti hai — Section 80C se ₹1.5 lakh (principal repayment), Section 24(b) se ₹2 lakh (interest payment), aur first time buyers ke liye Section 80EEA se additional ₹1.5 lakh. Matlab total ₹5 lakh tak deduction possible hai. New Tax Regime mein yeh benefits available nahi hain.

Q7. Home loan balance transfer karna chahiye kya?

Agar aapne 2022-2024 mein high rate par loan liya tha aur naye bank mein home loan interest rates 2026 India 0.50% – 1% kam hain, toh balance transfer smart move hai — especially agar loan abhi early stage (pehle 7-8 saal) mein hai. Processing fee ka calculation zaroor karo pehle.

Q8. Home loan ki maximum tenure kitni ho sakti hai?

Zyada tar banks maximum 30 saal tak ki tenure offer karte hain. Lamba tenure EMI kam karta hai lekin total interest zyada hoti hai. Home loan interest rates 2026 India ke current scenario mein 15-20 saal ki tenure generally balanced option hai — EMI manageable bhi rahegi aur total interest bhi zyada nahi badhega.

Q9. Kya self-employed logo ko home loan milna mushkil hota hai?

Self-employed logon ko home loan mil sakta hai lekin process thoda alag hota hai. Unhe last 2-3 saal ka ITR, business proof, aur bank statements dene padti hain. Home loan interest rates 2026 India mein self-employed ko salaried se 0.10% – 0.25% zyada rate lag sakti hai. Strong CIBIL score aur income proof is gap ko kam kar sakta hai.

Q10. Home loan prepayment par koi penalty lagti hai?

RBI ke rules ke hisaab se floating rate home loan par individual borrowers se koi prepayment penalty nahi ली ja sakti. Lekin fixed rate loans par prepayment charges lag sakte hain — usually outstanding amount ka 2%-4%. Isliye 2026 mein floating rate loan lena ek aur reason se faydamand hai.

Conclusion

Home loan interest rates 2026 India mein clearly ek positive shift aa raha hai. RBI ka accommodative stance, banks ke beech competition, aur falling inflation — sab milake ek favorable environment bana rahe hain home buyers ke liye.

Lekin sirf interest rate dekhna kaafi nahi hai. Apna CIBIL score maintain karo, multiple banks compare karo, hidden charges samjho, aur apni repayment capacity ke hisaab se loan lo. Tax benefits ka bhi poora faida uthao — especially agar aap Old Tax Regime mein hain.

2026 mein home loan interest rates India jo hain — woh ek smart buyer ke liye achi opportunity hai. Apna CIBIL score check karo, banks compare karo, documents ready rakho, aur apna sapna ghar is saal pura karo!

Aapka sapna ghar sirf ek sahi decision door hai. Aaj hi pehla kadam uthao!

Disclaimer

Upar di gayi interest rates indicative hain aur market conditions ke saath change ho sakti hain. Apply karne se pehle respective bank ki official website se latest rates verify karein. Yeh article sirf educational purpose ke liye hai — financial advice nahi hai.

Pingback: Best SIP for Students India 2026 — ₹500 Se Shuru Karo