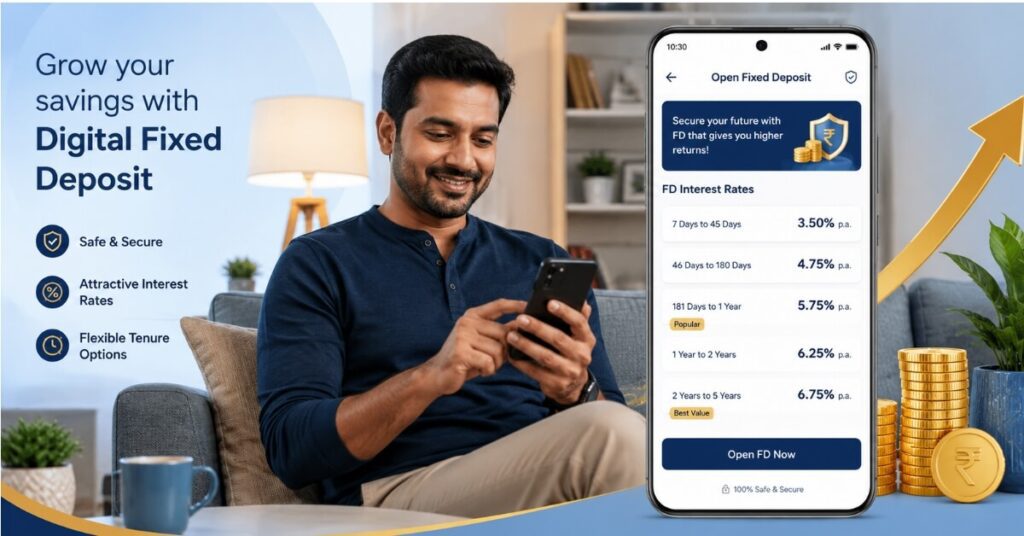

If you have been looking for a smarter, faster, and more rewarding way to grow your savings, a digital fixed deposit is the answer Gone are the days when you had to visit a bank branch, fill out paper forms, and wait in long queues just to open a fixed deposit. Today, a digital fixed deposit lets you invest from your smartphone in minutes — no paperwork, no branch visit, no hassle.

In this complete guide, you will learn everything about what it is, how it works, which platforms offer the best rates, what risks to watch out for, and how to make the most of your investment in 2026.

What Is a Digital Fixed Deposit?

is essentially the same as a traditional bank FD — you lock in your money for a fixed tenure and earn guaranteed interest. The key difference is that a digital fixed deposit is opened, managed, and renewed entirely online through a bank’s mobile app, net banking portal, or a third-party fintech platform.

Whether you are a salaried professional in India, an NRI living in the US, UK, or Canada, or a first-time investor, a digital fixed deposit gives you the flexibility to invest anytime, anywhere, with competitive interest rates that often beat traditional branch-based FDs.

The process is simple:

Choose a bank or fintech platform

Complete online KYC (Aadhaar-based or Video KYC)

Transfer funds via UPI or net banking

Start earning interest immediately

A digital deposit works exactly the same way in terms of interest rates, tenure, and tax rules — the only thing that changes is the convenience.

Why Fixed Deposits Are Trending in 2026

The rise of digital banking has dramatically changed how Indians save and invest. In 2026, a digital fixed deposit is no longer just a convenience feature — it has become the preferred choice for millions of investors across all age groups. Here is why:

1. Instant Account Opening

You can open a digital fixed deposit in as little as 3 to 5 minutes. With Video KYC and Aadhaar-OTP verification, there is zero paperwork involved.

2. Higher Interest Rates

Many banks and fintech platforms offer slightly higher rates on products compared to branch-based FDs — because digital channels reduce operational costs for banks.

3. Competitive Rates From Small Finance Banks

Small Finance Banks (SFBs) like Equitas, AU, Ujjivan, and Suryoday offer deposit rates ranging from 7.25% to 8.05% p.a. for regular investors and up to 8.5% p.a. for senior citizens in 2026.

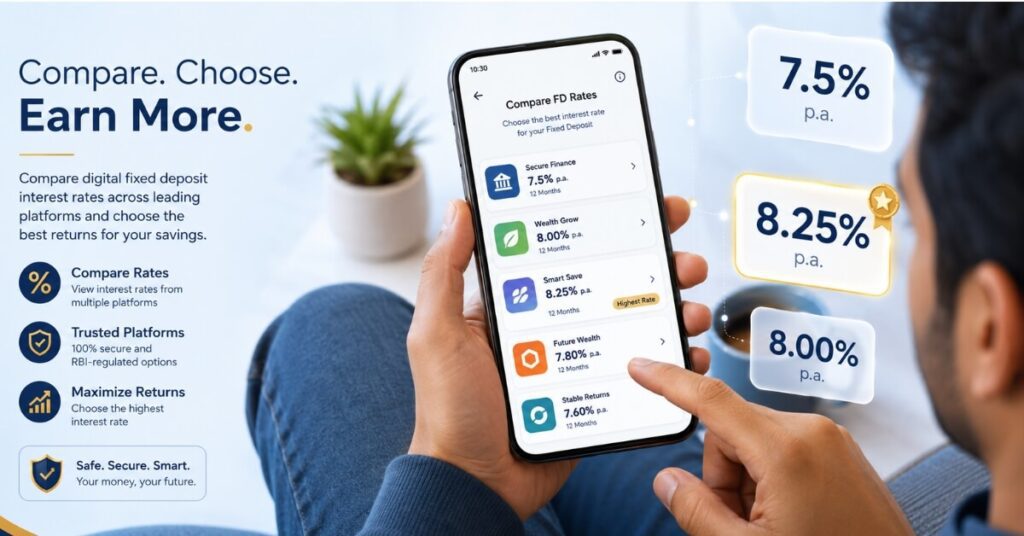

4. Compare and Invest in One Place

Fintech platforms like Stable Money, Paisa Bazaar, and Zerodha’s Kite allow you to compare rates from multiple banks and NBFCs side by side, and invest in the best one — all from one dashboard.

5. Easy Renewal and Premature Withdrawal

With a you can set up auto-renewal, track maturity dates, and even make premature withdrawals online without visiting a branch.

Deposit vs Traditional FD: Key Differences

Many investors wonder — is a really different from a regular FD? Let us break it down clearly:

| Feature | Traditional FD | Digital Fixed Deposit |

| Opening Process | Branch visit required | 100% online |

| KYC | Physical documents | Aadhaar / Video KYC |

| Time to Open | 1–3 days | 3–10 minutes |

| Interest Rates | Standard rates | Same or slightly higher |

| Premature Withdrawal | Branch visit | Online |

| Auto Renewal | Manual request | Automatic option |

| DICGC Insurance | Yes (bank FDs) | Yes (bank FDs) |

| Accessibility | Branch hours only | 24/7 anytime |

From an RBI regulation standpoint, a fixed carries the same legal protection as a branch-based FD. Both are covered under DICGC insurance up to ₹5 lakh per depositor per bank, provided the issuer is an RBI-registered bank. DICGC official website

Best Platforms to Open a Digital Fixed Deposit in 2026

Here are the top platforms where you can open a deposit in India right now:

1. Stable Money

Stable Money is one of the most popular fintech platforms for digital investment in India. It aggregates FDs from multiple banks and NBFCs and shows you the best rates in one place. You can compare fixed deposit options from SFBs, NBFCs, and private banks and invest directly without opening a new savings account.

2. Zerodha Kite (Zerodha Coin)

Zerodha — India’s largest stockbroker — now offers a fixed feature through its platform. Investors already using Zerodha for stocks and mutual funds can invest in FDs from select small finance banks directly from their Zerodha account.

3. Paisa Bazaar

Paisa Bazaar is one of India’s largest financial marketplaces where you can compare and open a deposit from multiple banks. The platform simplifies the comparison process and guides you through the entire KYC and investment journey online.

4. PhonePe

PhonePe has expanded beyond payments and now offers a digital feature through partnerships with banks and NBFCs. With a minimum investment of just ₹1,000, it is ideal for first-time investors.

5. Google Pay

Google Pay partnered with fintech startup Setu and small finance banks to allow users to open a fixed deposit directly from the app. It supports Aadhaar-based KYC and is available to users across India.

6. Amazon Pay

Amazon Pay launched its digital fixed deposit offering in January 2026 in partnership with Shriram Finance, Bajaj Finance, and multiple small finance banks. Users can start with just ₹1,000 and earn up to 8% p.a.

7. Navi

Navi’s app allows you to open a deposit with a few taps. It targets young, first-time investors and offers a clean, simple interface with competitive rates.

8. IND Money

IND Money is a wealth management app that has added fixed as a feature alongside mutual funds, US stocks, and NPS. It is particularly popular with NRIs who want to invest in Indian FDs from abroad.

9. CRED

CRED — known for credit card bill payments — now offers a digital fixed deposit product that rewards users with extra benefits on top of standard interest rates.

10. Fi Money

Fi Money is a neo-banking app that offers a seamless deposit experience with instant activation and competitive rates from partner banks.

Digital Fixed Deposit Interest Rates in 2026

Here is a quick comparison of the best fixed deposit rates available in June 2026:

| Institution | Regular Rate (p.a.) | Senior Citizen Rate (p.a.) |

| Suryoday Small Finance Bank | Up to 8.05% | Up to 8.55% |

| Equitas Small Finance Bank | Up to 7.40% | Up to 8.00% |

| AU Small Finance Bank | Up to 7.50% | Up to 8.00% |

| Ujjivan Small Finance Bank | Up to 7.75% | Up to 8.25% |

| Bajaj Finance (NBFC) | Up to 8.10% | Up to 8.35% |

| Shriram Finance (NBFC) | Up to 8.25% | Up to 8.50% |

| HDFC Bank | Up to 6.60% | Up to 7.10% |

| SBI | Up to 6.45% | Up to 7.05% |

Note: Rates are indicative and subject to change. Always verify current rates on the official platform before investing.

Small Finance Banks and NBFCs offer significantly higher interest on digital deposit products than large public sector or private banks. However, they also come with different risk profiles — more on that below.

Who Should Invest in a Digital Fixed Deposit?

A digital deposit is suitable for a wide range of investors:

Conservative Investors who want guaranteed, risk-free returns without market exposure will find a digital fixed deposit to be the safest choice.

Senior Citizens benefit greatly from a fixed deposit because they receive an additional 0.50% to 0.75% interest over and above the regular rate at most banks.

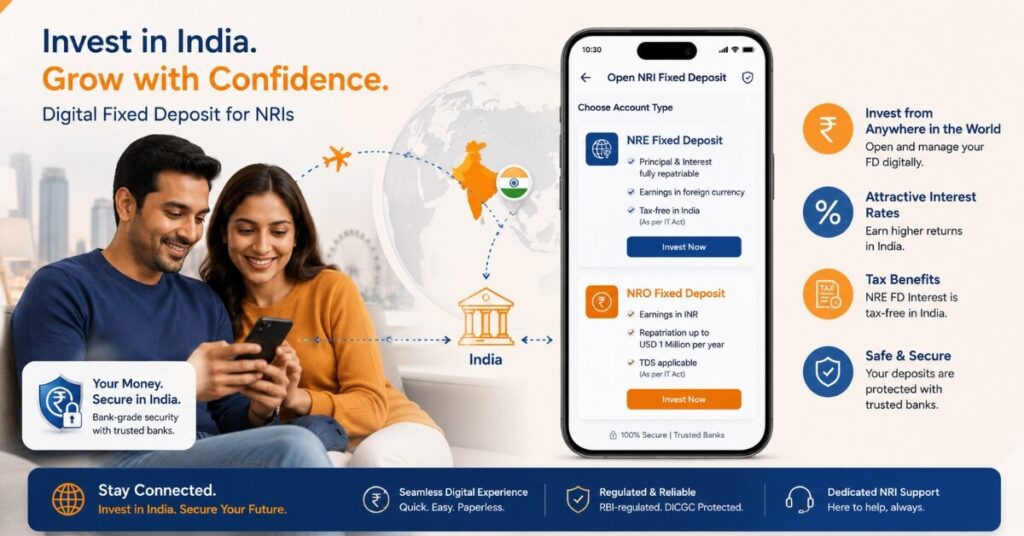

NRIs and Indian Diaspora living in the US, UK, Canada, or Australia can invest in deposit products through NRE or NRO accounts using platforms that support remote KYC. The interest on NRE FDs is fully tax-free in India.

First-Time Investors who are just starting their investment journey will find a deposit to be the most comfortable first step — it is simple, predictable, and completely safe (within the DICGC insurance limit).

Salaried Professionals looking to park their emergency fund or short-term savings in something better than a savings account will benefit from a deposit without tying up their money for too long.

Tax on Fixed Deposit: What You Must Know

Before you open a digital fixed understanding the tax implications is critical. The tax rules for a deposit are identical to those for a traditional FD.

TDS (Tax Deducted at Source)

Banks are required to deduct TDS on FD interest income as follows:

If interest earned in a financial year exceeds ₹40,000 (for individuals below 60 years), TDS at 10% is deducted — provided you have submitted your PAN.

For senior citizens, the TDS threshold is ₹50,000 per year.

If PAN is not submitted, TDS is deducted at 20%.

How to Avoid TDS on Digital Fixed Deposit

If your total income is below the taxable limit, you can submit Form 15G (for individuals below 60 years) or Form 15H (for senior citizens aged 60 and above) to the bank or fintech platform to avoid TDS deduction on your fixed deposit interest.

Income Tax on FD Interest

The interest earned on a digital fixed deposit is added to your total income and taxed as per your income tax slab. For example, if you are in the 30% tax bracket and earn 8.5% on your fixed deposit, your effective post-tax return will be approximately 5.95%.

Tax-Saving FD

You can also invest in a tax-saving deposit under Section 80C of the Income Tax Act. This allows you to claim a deduction of up to ₹1.5 lakh per year. However, tax-saving FDs come with a mandatory lock-in period of 5 years and cannot be withdrawn prematurely.

“FD interest par TDS kaise bachayein, yeh samajhne ke liye hamara guide padhen — How to File ITR Online in 2026″

Risks of Digital Fixed Deposit: What to Watch Out For

A fixed deposit is generally a very safe investment, but there are a few risks you should be aware of before investing:

1. NBFC Digital FDs Are Not Covered by DICGC

This is the most critical risk. DICGC insurance of ₹5 lakh per depositor per bank applies only to RBI-registered banks. If you open a digital fixed deposit with an NBFC like Bajaj Finance or Shriram Finance, your money is NOT covered by DICGC insurance. In the event of the NBFC defaulting, you could lose your principal.

What to do: Invest only in NBFCs with AAA or AA+ credit ratings from CRISIL or ICRA. Limit your exposure to any single NBFC.

2. Fintech Platform Risk

The fintech platform you use to open a digital deposit is only a middleman. The actual deposit receipt comes from the underlying bank or NBFC. If the platform shuts down, your money stays with the issuer — but it may be difficult to access without the platform.

What to do: Always keep your original fixed deposit receipt and note down the issuer’s name and contact details separately.

3. Auto-Renewal at Lower Rates

Many digital fixed deposit platforms set auto-renewal as the default option. If interest rates drop by the time your FD matures, your digital deposit will automatically renew at the new (lower) rate unless you intervene.

What to do: Always set maturity reminders and review your fixed deposit rates at renewal time.

4. Premature Withdrawal Penalty

Breaking a digital fixed deposit before maturity usually attracts a penalty of 0.5% to 1% on the applicable interest rate. This can significantly reduce your effective return.

What to do: Choose the right tenure for your deposit based on your actual financial needs and liquidity requirements.

5. Inflation Risk

If inflation (currently around 4–5% in India) is close to or higher than your fixed interest rate, your real return after tax can turn negligible or even negative.

What to do: Ladder your digital fixed deposit investments across different tenures to balance safety and returns.

How to Open fixed Deposit: Step-by-Step Guide

Opening a fixed deposit is extremely simple. Here is a quick walkthrough:

Step 1: Choose Your Platform

Decide whether you want to open a fixed directly through your bank’s app or through a third-party fintech platform like Stable Money or Paisa Bazaar.

Step 2: Compare Interest Rates

Use a fintech aggregator to compare fixed deposit rates across banks and NBFCs. Even a 0.25% difference in interest rate can make a meaningful difference over a 3-5 year period.

Step 3: Complete KYC

Most platforms require Aadhaar-based OTP verification or Video KYC. Keep your PAN card and Aadhaar handy.

Step 4: Choose Tenure and Interest Payout

Decide the tenure (3 months to 10 years) and whether you want cumulative (interest compounded) or non-cumulative (monthly/quarterly payouts) payout on your digital fixed deposit.

Step 5: Transfer Funds

Fund your digital fixed deposit via UPI (up to ₹1 lakh) or net banking / payment gateway for higher amounts.

Step 6: Save Your Receipt

Download and save your receipt. This is your legal proof of investment.

Smart Tips to Maximize Returns on Digital Fixed Deposit

Ladder Your FDs: Instead of putting all your money in one digital fixed split it across 3-month, 6-month, 1-year, and 3-year tenures. This way you always have some liquidity and can reinvest at higher rates as they mature.

Choose Small Finance Banks for Higher Returns: SFBs consistently offer 0.5% to 2% higher interest on digital products than large private banks — with the same DICGC insurance protection.

Senior Citizens: Always Claim the Extra Rate: If you are 60 or above, always explicitly select the senior citizen category while opening a digital fixed deposit to get the additional 0.50%+ interest rate.

Submit Form 15G/15H Early: Do not wait for TDS to be deducted. Submit Form 15G or 15H at the start of the financial year to avoid unnecessary TDS on your deposit interest.

Diversify Across Banks: DICGC covers up to ₹5 lakh per depositor per bank. If you have more than ₹5 lakh to invest, split your fixed deposit across multiple banks to maximize insurance coverage.

Digital Fixed Deposit for NRIs: What You Should Know

If you are an Indian living abroad — in the US, UK, Canada, or Australia — you can also invest in a deposit in India through:

NRE Fixed Deposit: Interest is fully tax-free in India. Funds are repatriable. Best option for NRIs who earn abroad and want to invest in India.

NRO Fixed Deposit: For income earned in India (rent, pension, dividends). Interest is taxable in India but can be repatriated up to $1 million per year.

Several fintech platforms like IND Money, NRI-focused banking apps, and major private banks like HDFC, ICICI, and Axis Bank support remote digital fixed deposit opening for NRIs with video KYC from anywhere in the world.

Frequently Asked Questions (FAQs)

Q1. Is a digital fixed deposit safe?

Yes, a fixed opened with an RBI-registered bank is protected under DICGC insurance up to ₹5 lakh per depositor per bank. However, products from NBFCs are not covered by DICGC.

Q2. Can I open a fixed deposit without a savings account?

Yes! Platforms like Stable Money and Paisa Bazaar allow you to open a deposit from any bank without having an existing savings account with that bank.

Q3. What is the minimum amount for a fixed deposit?

Most platforms allow you to start a deposit with as little as ₹1,000. Some bank-specific digital FDs may require a minimum of ₹5,000.

Q4. Can I break my fixed before maturity?

Yes, premature withdrawal is allowed on most digital fixed products, but a penalty of 0.5% to 1% on the interest rate is usually applied.

Q5. Is the interest on fixed deposit taxable?

Yes, the interest earned on a fixed is fully taxable as per your income tax slab. TDS is applicable if interest exceeds ₹40,000 per year (₹50,000 for senior citizens).

Q6. Which platform offers the highest interest on fixed deposit?

In 2026, Suryoday Small Finance Bank and Shriram Finance offer some of the highest rates on digital products — up to 8.05% and 8.25% p.a. respectively. However, always compare rates across platforms before investing.

Q7. Can NRIs open a deposit in India?

Yes, NRIs can open NRE or NRO fixed deposit accounts through major private banks and select fintech platforms that support video KYC for overseas customers.

Q8. What happens to my deposit if the fintech platform shuts down?

Your digital fixed deposit is issued by the underlying bank or NBFC — not by the fintech platform. Even if the platform shuts down, your money remains with the issuer and your investment is protected.

Conclusion

A digital fixed in 2026 is one of the smartest, safest, and most convenient ways to grow your savings — whether you are an Indian resident, an NRI, a first-time investor, or a senior citizen looking for steady income. With fintech platforms making it possible to compare and invest in the best rates in minutes, there has never been a better time to switch from branch-based FDs to the fully digital route.

Start with a small amount, choose a reputable bank or NBFC, diversify across tenures, and let your fixed deposit work for you 24/7 — no branch visits required.

Ready to open your first deposit? Start by comparing rates on platforms like Stable Money, Paisa Bazaar, or your bank’s own app today.

Disclaimer

The information provided in this article about digital fixed deposit is for educational purposes only and does not constitute financial advice. Interest rates mentioned are indicative and subject to change. Please verify current rates and terms directly with the issuing bank or NBFC before investing. DICGC insurance applies only to RBI-registered banks and not to NBFC deposits. Consult a certified financial advisor before making any investment decisions.

Pingback: SEO Title: Best Mutual Funds for Students in India 2026