Paying off your last debt feels incredible. Whether it was a credit card, a student loan, or a personal loan — that final payment is one of the greatest financial moments of your life. But here is the truth that most people never hear: becoming debt-free is not the finish line. It is the starting point of your debt free financial freedom journey.

Millions of people pay off their debt, celebrate for a few weeks, and then slowly drift back into old habits — lifestyle inflation, impulse spending, and eventually, new debt. If you want to make sure that never happens to you, you need a clear and proven plan for what comes next.

This guide gives you exactly that — 7 powerful steps to go from debt-free to achieving true debt free financial freedom, with practical actions you can start today.

Why Debt-Free and Debt Free Financial Freedom Are Not the Same Thing

Before we go into the steps, let us clear up the most common misconception in personal finance.

Most people assume that once they pay off all their debts, they have achieved debt free financial freedom. But that assumption is wrong. Being debt-free simply means you no longer owe money to anyone. Debt free financial freedom means your investments, savings, and passive income are large enough to cover your lifestyle — without you needing to work.

Consider this example. Someone pays off ₹5 lakh in credit card debt. They are now debt-free. But if they have zero savings, no investments, and no emergency fund — a single medical emergency or job loss pushes them straight back into debt. That is not debt free financial freedom. That is financial fragility with no debt label on it.

True debt free financial freedom is the state where your money grows every month on its own — whether you work or not. Your investments produce returns. Your savings earn interest. Your income streams flow without constant effort. That is the goal this guide is built around.

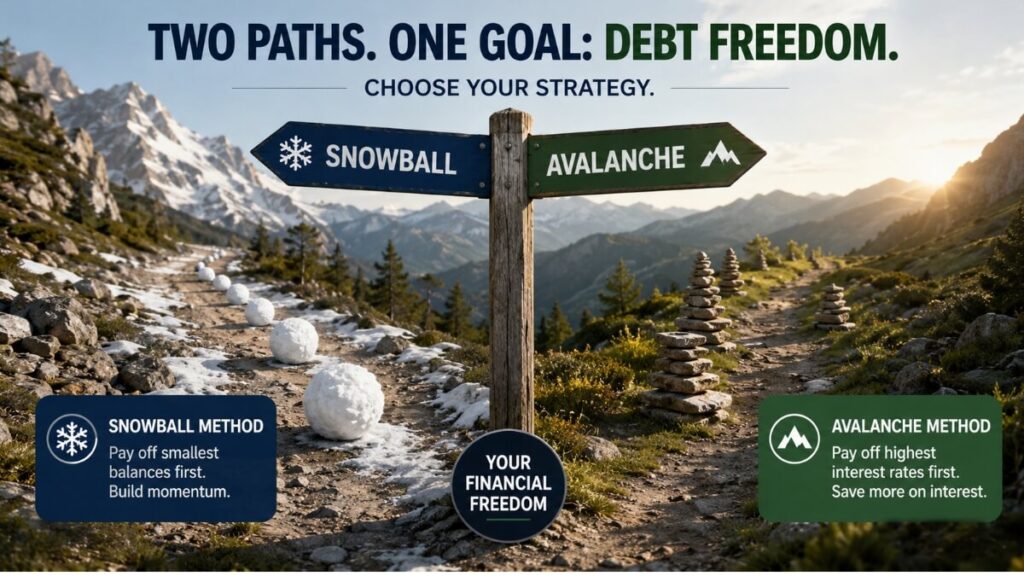

If you are still working on paying off your debt and need the right strategy, read our complete guide on Debt Snowball vs Avalanche before you begin applying these steps toward debt free financial freedom.

7 Steps to Achieve Debt Free Financial Freedom

Step 1 — Build a Fully Funded Emergency Fund

The first and most important step toward debt free financial freedom is building a solid emergency fund. This step is not exciting — but skipping it is the number one reason people fall back into debt after paying it all off.

Before you invest a single dollar, before you open any brokerage account, before you think about building passive income — you need cash reserves that can protect you from life’s unexpected events. A car breakdown, a hospital visit, a sudden job loss — any of these without a cash buffer will send you right back to square one on your debt free financial freedom journey.

How large should your emergency fund be?

The universal recommendation from financial experts is 3 to 6 months of your total monthly living expenses. If your monthly expenses are $2,000, your target emergency fund is between $6,000 and $12,000. If your income is irregular or your job is uncertain, build toward the full 6 months.

Where to keep your emergency fund:

Store it in a high-yield savings account — accessible immediately but separate from your daily spending account. In 2026, high-yield savings accounts offer 4% to 5% annual returns, so your emergency fund earns while it waits. This cash cushion is the foundation that makes everything else in your debt free financial freedom plan work safely.

Step 2 — Redirect Every Old Debt Payment Into Investments

This is the step that truly separates people who are debt-free from people who achieve real debt free financial freedom — and most people miss it completely.

Every month you were paying off debt, a fixed amount of money was leaving your account. Now that the debt is gone, that money is freed up. The critical question is: where does it go next?

Most people unconsciously absorb that freed-up money into lifestyle spending. They eat out more, upgrade their phone, spend a little more here and there. Within months, the extra money has vanished — and their debt free financial freedom timeline has quietly extended by years.

The right move is to immediately redirect every rupee or dollar of your former debt payments into investments. Set up an automatic transfer on your payday so the money moves before you can spend it.

Smart investment options after becoming debt-free:

Index funds and ETFs — Low cost, globally diversified, proven long-term performance

Retirement accounts (401k, IRA, NPS, PPF) — Tax-advantaged compounding over decades

SIP in mutual funds — Systematic investment plan for consistent Indian market exposure

REITs — Real estate returns without buying property directly

Dividend stocks — Build a portfolio that pays you regularly

The compounding math behind this step is the engine of debt free financial freedom. Redirecting $500 per month into investments at 10% annual return produces over $378,000 in 20 years. That money came entirely from payments you were already making — just redirected toward wealth instead of interest.

Step 3 — Set Clear and Written Financial Goals

Achieving debt free financial freedom without written goals is like driving to an unknown destination without a map. You may keep moving, but you will not know where you are going or when you have arrived.

Now that the burden of debt is behind you, this is the moment to sit down and define exactly what debt free financial freedom looks like in your life. Do you want to retire at 50? Do you want to travel the world? Do you want your children’s education fully funded? Do you want a home bought completely with cash?

Every one of these visions requires a specific number and a specific timeline — and that is exactly what your written goals give you.

How to set effective financial goals:

Short-term (1–2 years): Full emergency fund, first investment account opened, one debt-funded vacation

Medium-term (3–7 years): $50,000 net worth, house down payment saved, side income stream active

Long-term (10–30 years): Full retirement savings, passive income covering expenses, complete debt free financial freedom achieved

Assign a rupee or dollar amount to every goal. Set a deadline. Then calculate exactly how much you need to save or invest each month to hit it. Review these goals every 6 months and adjust as your income and life situation change.

Written goals transform debt free financial freedom from a concept into a personal roadmap.

Step 4 — Build Multiple Streams of Income

Here is a truth that the fastest achievers of debt free financial freedom all understand: you cannot cut expenses fast enough to become wealthy. You must grow your income.

Expense cutting has a hard floor — there is only so much you can remove before your quality of life suffers. But income growth has no ceiling. Every new income stream you build accelerates your debt free financial freedom timeline dramatically.

Practical income streams to build in 2026:

Freelancing — Writing, design, coding, consulting, video editing

Digital products — Ebooks, online courses, templates, Notion systems

Affiliate marketing — Earn commissions promoting products you genuinely use

Rental income — A spare room, a parking spot, or short-term rental platforms

Dividend investing — Stocks that pay you quarterly regardless of your activity

Blogging or content creation — Build an audience that generates AdSense and affiliate income over time

When your income arrives from multiple sources, you are no longer financially vulnerable to losing any single one. That resilience is a core component of real debt free financial freedom — not just the absence of debt, but the presence of multiple income flows.

Step 5 — Get the Right Insurance Coverage

This step is the one that most personal finance guides skip — and it is one of the most important protections for your debt free financial freedom.

You have spent months or years eliminating debt and building financial stability. One serious medical event, one disability, one major accident without adequate insurance coverage can erase everything in weeks. Medical debt is the leading cause of personal bankruptcy in many countries — affecting people who were otherwise financially responsible and on track toward debt free financial freedom.

Insurance coverage every debt-free person needs:

Health insurance — Non-negotiable. One hospitalization without coverage can cost tens of thousands of dollars.

Term life insurance — Affordable and essential if anyone depends on your income

Disability insurance — Replaces your income if illness or injury stops you from working. Most people ignore this until it is too late.

Home and vehicle insurance — Protects your two largest physical assets from unexpected loss

Insurance is not an expense that hurts your debt free financial freedom plan. It is the wall that keeps one bad event from destroying it entirely.

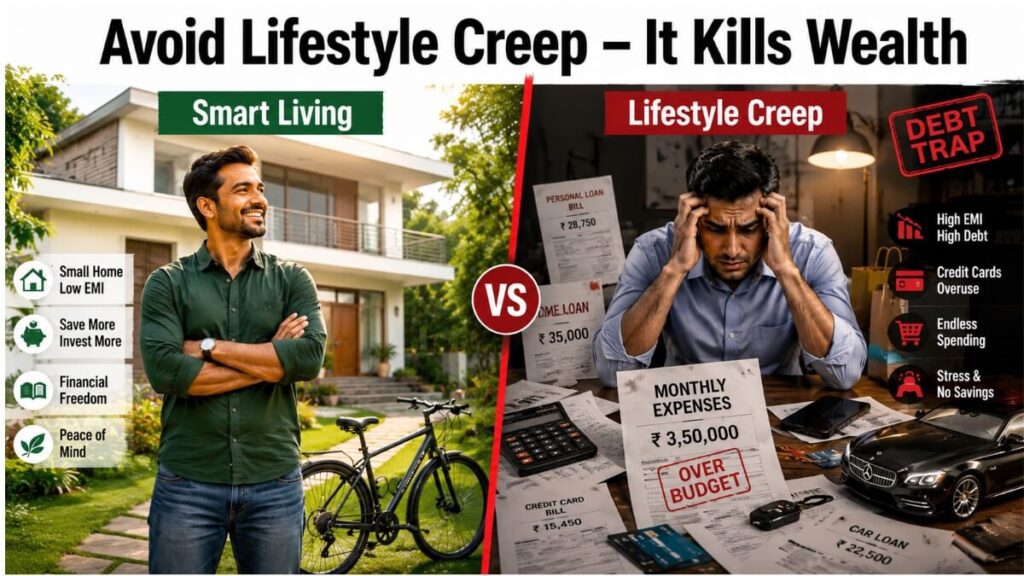

Step 6 — Fight Lifestyle Creep Every Single Month

Of all the threats to debt free financial freedom, lifestyle creep is the quietest and most destructive. It does not announce itself. It grows slowly, silently, one small upgrade at a time — until your increased income has entirely disappeared into a more expensive lifestyle and your wealth-building progress has stalled.

Lifestyle creep happens when your spending rises in proportion to your income. You get a salary raise — and somehow your savings rate stays identical. You pay off your car — and immediately finance a newer, more expensive one. You free up $600 a month from debt payments — and within three months that $600 has been absorbed into dining, subscriptions, and impulse purchases.

Every person who achieves debt free financial freedom has learned to recognize and resist this pattern.

How to protect your debt free financial freedom from lifestyle creep:

Automate investments before spending — Move money to investment accounts on payday, before you see it

Use the 24-hour rule — Wait one full day before any unplanned purchase over $50

Audit subscriptions every 3 months — Cancel everything you do not actively use weekly

Maintain your debt-payoff lifestyle — Live at the same level for at least 12 months after becoming debt-free

Track net worth monthly, not just spending — Watching your wealth grow is the most powerful motivation to keep lifestyle in check

The wealth gap — the difference between what you earn and what you spend — is where debt free financial freedom lives. Protect it fiercely.

Step 7 — Commit to Lifelong Financial Education

The final step toward debt free financial freedom is the one that sustains everything else over decades: never stop learning about money.

Tax laws change every year. New investment vehicles emerge. Economic conditions shift. Interest rates move. The people who achieve debt free financial freedom and keep it are the ones who treat financial education as an ongoing commitment — not a one-time event.

The best ways to stay financially educated:

Books — The Psychology of Money by Morgan Housel, Rich Dad Poor Dad by Robert Kiyosaki, The Millionaire Next Door by Thomas Stanley

Finance blogs and websites — Read regularly about investing, budgeting, tax planning, and wealth building

Podcasts — Turn daily commutes into financial learning sessions

Certified financial planner (CFP) — Consult one for major decisions involving real estate, retirement, or business investment

Tax optimization — Learn every legal deduction and tax-advantaged account available to you. This l can accelerate debt free financial freedom by years.

Every concept you understand makes you a sharper decision-maker. And sharp, consistent decisions made over 10 to 20 years are the actual mechanism behind every story of debt free financial freedom you have ever admired.

Month-by-Month Debt Free Financial Freedom Roadmap

Months 1–3: Build your full emergency fund. Do not invest yet. Establish your safety net completely before anything else.

Months 4–6: Open investment accounts. Automate your former debt payments into index funds or mutual funds. Set up SIPs if you are an Indian investor.

Months 7–12: Write your 5-year and 10-year financial goals with specific numbers and deadlines. Review your insurance coverage. Launch one new income stream.

Year 2 and beyond: Increase your investment rate with every income raise. Review net worth every quarter. Expand income streams. Continue financial education. Stay disciplined on lifestyle.

This roadmap gives your debt free financial freedom journey a structured timeline — transforming abstract goals into concrete monthly actions.

5 Mistakes That Destroy Debt Free Financial Freedom

Mistake 1 — Stopping at debt-free. Paying off debt is step one, not the destination. Debt free financial freedom requires active wealth-building after the debt is gone.

Mistake 2 — Investing without an emergency fund. When markets drop and life gets expensive simultaneously, you are forced to sell at losses. Build the safety net first.

Mistake 3 — Ignoring income growth. Saving alone cannot build real wealth fast enough. Growing your income is the accelerator of debt free financial freedom.

Mistake 4 — Skipping tax optimization. Legal tax reduction through retirement accounts, deductions, and smart investing structures can save thousands of dollars per year — money that compounds directly toward debt free financial freedom.

Mistake 5 — Lifestyle creep acceptance. Every rupee absorbed by lifestyle inflation is a rupee removed from your debt free financial freedom timeline. Guard the wealth gap relentlessly.

Frequently Asked Questions

Q1. How long does it realistically take to achieve debt free financial freedom?

With a consistent savings and investment rate of 20% to 30% of income, most people can achieve debt free financial freedom within 10 to 20 years of becoming debt-free. The exact timeline depends on income level, investment returns, and lifestyle discipline.

Q2. What should I do immediately after making my last debt payment?

Celebrate briefly — then build your emergency fund. This is the single most important first move after becoming debt-free, and it protects your entire debt free financial freedom plan from being derailed by unexpected expenses.

Q3. Should I invest or save first after paying off debt?

Build your emergency fund first — 3 to 6 months of expenses in a high-yield savings account. Then begin investing your former debt payments into diversified index funds or retirement accounts.

Q4. How do I make sure I never go back into debt?

Automate investments, track your net worth monthly, avoid lifestyle creep, and keep an emergency fund fully funded at all times. These four habits together make debt free financial freedom permanent rather than temporary.

Q5. Can someone with an average salary achieve debt free financial freedom?

Yes — absolutely. Debt free financial freedom is determined by the gap between income and expenses, not by income level alone. Millions of average earners worldwide have achieved it through consistent habits, disciplined investing, and growing multiple income streams over time.

Conclusion

Paying off your debt was a major victory — one that required real sacrifice and discipline. But the chapter that follows is even more important. The path from debt-free to debt free financial freedom is built on seven consistent steps: a strong emergency fund, redirected investments, clear written goals, multiple income streams, proper insurance, lifestyle discipline, and continuous financial education.

None of these steps requires a high income or perfect timing. They require consistency. Start with step one today — build your emergency fund. Then move to step two. Then step three. Each step builds on the last, and over months and years, the compounding effect of these habits creates something remarkable: true debt free financial freedom — the life where your money works for you, and your time belongs entirely to you.

Your debt free financial freedom journey starts now.

Disclaimer

This article is for informational and educational purposes only. It does not constitute professional financial, investment, or tax advice. Please consult a certified financial advisor before making major financial decisions. Individual results may vary based on income, expenses, investment returns, and personal financial circumstances

Pingback: Vanguard India Stocks 2026: 7 Powerful Picks to Watch