TDS on rent FY 2026-27 has become one of the most searched tax topics in India right now — and for good reason. The Government of India has introduced the new Income Tax Act 2025, which is effective from 1st April 2026. Under this new law, the entire TDS framework has been restructured and consolidated under Section 393. If you are a tenant, landlord, business owner, or individual paying rent in India, understanding TDS on rent FY 2026-27 is not optional — it is a legal compliance requirement.

In this complete guide, we will cover everything you need to know about TDS on rent FY 2026-27 — including applicable rates, threshold limits, who needs to deduct, due dates, penalties, and the impact of the new Income Tax Act 2025. We have also added an FAQ section at the end to answer your most common questions.

What is TDS on Rent?

TDS stands for Tax Deducted at Source. It is a mechanism under the Indian Income Tax system where the person making a payment deducts a certain percentage of tax before transferring the amount to the recipient. The deducted amount is then deposited directly with the government on behalf of the recipient.

In the context of rent, TDS on rent means that the tenant (the person paying rent) is required to deduct a fixed percentage of tax from the rent amount before paying the landlord. The landlord can later claim this deducted amount as a tax credit while filing their Income Tax Return (ITR).

TDS on rent FY 2026-27 is now governed under Section 393 of the Income Tax Act 2025, which replaces the earlier Sections 194-I and 194-IB of the Income Tax Act 1961.

TDS on Rent FY 2026-27 has become an important compliance requirement for both tenants and landlords after the implementation of the new Income Tax Act 2025. Understanding the latest TDS rules, deduction rates, and filing procedures can help taxpayers avoid penalties and ensure smooth tax compliance throughout the financial year.

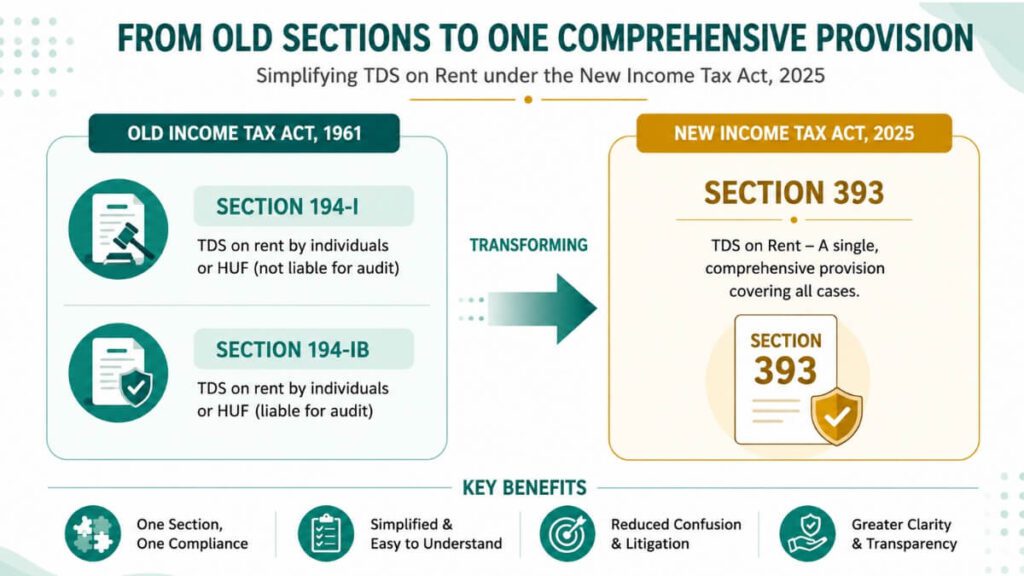

What is Section 393 of Income Tax Act 2025?

Section 393 is the new consolidated TDS section under the Income Tax Act 2025, applicable from 1st April 2026. Before this, TDS provisions were scattered across more than 20 different sections of the Income Tax Act 1961 — such as 194A, 194C, 194H, 194-I, 194-IB, and many others. This made compliance complex and confusing.

The new Income Tax Act 2025 has simplified this by bringing all TDS provisions (except salary TDS, which is under Section 392) under one umbrella — Section 393. This structural change does not alter the TDS rates or threshold limits. Only the section numbering has changed.

Many taxpayers still remain confused about the applicability of TDS on Rent FY 2026-27 after the introduction of Section 393 under the new Income Tax Act 2025. However, the government has mainly restructured the law for easier understanding, while the existing TDS rates and threshold limits continue to remain the same for most taxpayers.

For TDS on rent specifically:

Taxpayers can verify latest TDS rules and compliance updates on the official income tax portal.

Old Section 194-I (for businesses, companies, firms) → Now Section 393(1) [Table Sl. No. 2(ii)]

Old Section 194-IB (for individuals/HUFs not under tax audit) → Now Section 393(1) [Table Sl. No. 2(i)]

Who Needs to Deduct TDS on Rent FY 2026-27?

There are two categories of rent payers under TDS on rent FY 2026-27:

Category 1 — Businesses, Companies, Firms, LLPs & Tax-Audited Individuals/HUFs

If you fall under any of the following, you are in Category 1:

Companies (private or public)

Partnership firms and LLPs

Individuals or HUFs whose business turnover exceeds ₹1 crore or professional receipts exceed ₹50 lakh in the preceding year (i.e., subject to tax audit)

Applicable Section: Section 393(1) [Table Sl. No. 2(ii)] — previously Section 194-I

TAN Required: Yes

Category 2 — Individuals & HUFs Not Under Tax Audit

If you are an individual or HUF who is not required to get accounts audited, you fall under Category 2. These are typically salaried individuals or small business owners who pay rent and are not under tax audit.

Applicable Section: Section 393(1) [Table Sl. No. 2(i)] — previously Section 194-IB

TAN Required: No — PAN is sufficient

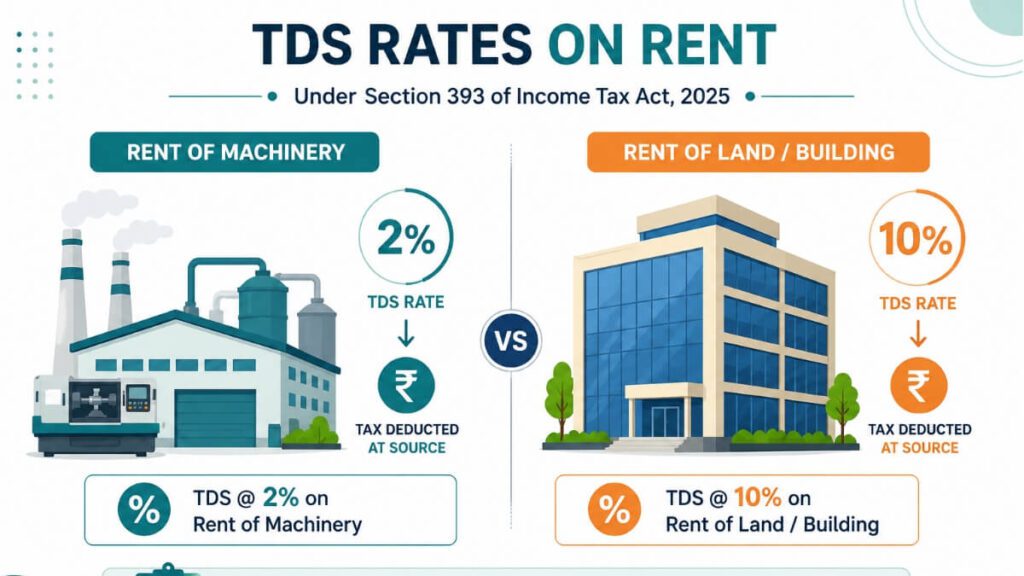

TDS on Rent Rates FY 2026-27

Here are the applicable TDS on rent FY 2026-27 rates based on the type of property:

For Category 1 (Businesses, Companies, Tax-Audited Individuals/HUFs):

| Type of Property | TDS Rate |

| Land, Building, Furniture | 10% |

| Plant, Machinery, Equipment | 2% |

Annual Threshold: ₹2,40,000 per year per payee. If annual rent payment does not exceed ₹2,40,000, no TDS is required.

For Category 2 (Individuals/HUFs not under Tax Audit):

| Type of Property | TDS Rate |

| Any property (land/building) | 2% |

Monthly Threshold: ₹50,000 per month. If monthly rent does not exceed ₹50,000, no TDS is required.

Important Note: There is no change in TDS rates under the new Income Tax Act 2025. The rates of 2% and 10% remain exactly the same as under the Income Tax Act 1961.

What is Covered Under “Rent” for TDS Purposes?

Under TDS on rent FY 2026-27, the definition of “rent” is broad. It includes any payment made under a lease, sub-lease, tenancy, or any other arrangement for the use of:

Land

Building (including factory buildings)

Land appurtenant to a building

Machinery

Plant and equipment

Furniture and fittings

This means that even if you are paying for the use of a machine or equipment — not just a house or office — TDS on rent FY 2026-27 provisions will apply if the threshold is crossed.

Threshold Limits for TDS on Rent FY 2026-27

Understanding threshold limits is critical to determine whether TDS needs to be deducted or not.

For Category 1 (Businesses, firms, companies):

Annual rent to a single landlord must exceed ₹2,40,000 for TDS to apply

Calculated on aggregate annual basis — not monthly

For Category 2 (Individuals/HUFs not under tax audit):

Monthly rent must exceed ₹50,000 for TDS to apply

TDS is deducted only once a year — from the rent of the last month of the financial year or the last month of tenancy, whichever is earlier

Before making any rental payment, taxpayers should carefully check whether TDS on Rent FY 2026-27 provisions are applicable based on the prescribed threshold limits. Proper deduction, timely deposit, and accurate return filing are essential to avoid interest charges and legal complications under the Income Tax Act 2025.

Is TDS on Rent Applicable on GST Amount?

This is one of the most common questions about TDS on rent FY 2026-27. The answer depends on how GST is mentioned in the rent agreement or invoice.

If GST is separately mentioned in the invoice or rent agreement → TDS is applicable only on the rent amount excluding GST

If GST is not separately mentioned → TDS is applicable on the gross amount including GST

The CBDT has issued a circular confirming that TDS is not applicable on the GST component when it is indicated separately. So it is always advisable for landlords to issue proper GST invoices with the rent and GST amounts

When to Deduct TDS on Rent FY 2026-27?

TDS on rent must be deducted at the time of:

Credit of rent to the landlord’s account, OR

Actual payment of rent — whichever is earlier

If rent is credited monthly (e.g., on a journal entry basis) but paid quarterly, TDS must be deducted at the time of monthly credit — not at the time of actual payment.

For Category 2 (Individuals/HUFs): TDS is deducted only once a year — at the time of paying the last month’s rent of the financial year, or the last rent payment if the tenancy ends mid-year.

To ensure smooth tax compliance, tenants should always verify PAN details of the landlord before deducting TDS on Rent FY 2026-27. Incorrect PAN information can lead to higher TDS deduction rates and complications while filing TDS returns or claiming tax credit.

Due Dates for TDS Deposit — TDS on Rent FY 2026-27

After deducting TDS, the tenant must deposit the amount to the government within the following due dates:

| Month of Deduction | Due Date for Deposit |

| April to February | 7th of the following month |

| March | 30th April |

For example, if TDS on rent is deducted in June 2026, it must be deposited by 7th July 2026.

For Category 2 (Individuals/HUFs): The TDS must be deposited within 30 days from the end of the month in which the deduction is made, using Challan 26QC.

TDS Return Filing for TDS on Rent FY 2026-27

After depositing TDS, the deductor must also file TDS returns:

For Category 1 (Businesses with TAN):

File Form 26Q quarterly

Due dates: 31st July, 31st October, 31st January, 31st May

For Category 2 (Individuals/HUFs without TAN):

File Form 26QC — a one-time challan-cum-statement

No quarterly filing required

Must be filed within 30 days from the end of the month of deduction

With increasing scrutiny by the Income Tax Department, accurate reporting of TDS on Rent FY 2026-27 has become more important than ever. Taxpayers should maintain proper documentation of rent payments, challans, and TDS certificates to avoid future disputes or compliance issues.

TDS Certificate — Form 16C and Form 16A

Once TDS is deducted and deposited, the deductor must issue a TDS certificate to the landlord:

Category 1 (Businesses): Issue Form 16A — generated from TRACES portal

Category 2 (Individuals/HUFs): Issue Form 16C — generated from TRACES portal

The landlord uses this certificate to claim TDS credit while filing their ITR.

How to Avoid TDS Deduction on Rent — Form 121

Under the new Income Tax Act 2025, if a landlord’s total estimated income for the financial year is nil or below the taxable threshold, they can submit Form 121 to the tenant requesting nil TDS deduction.

Under the old Income Tax Act 1961, this was done via Form 15G or Form 15H. The new Income Tax Act 2025 has replaced these with Form 121.

The landlord must submit Form 121 to each payer separately. The tenant can then process rent without deducting TDS, provided the form is valid.

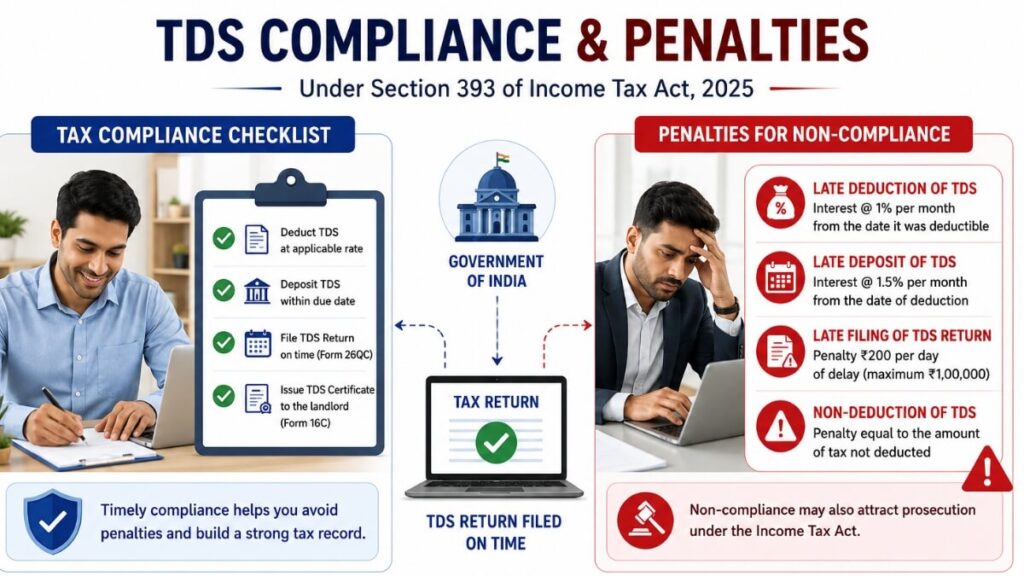

Penalties for Non-Compliance — TDS on Rent FY 2026-27

Non-compliance with TDS on rent provisions can result in severe penalties. Here is what you need to know:

1. Interest for Late Deduction

1% per month (or part of month) from the date TDS was supposed to be deducted until the date it was actually deducted

2. Interest for Late Deposit

1.5% per month (or part of month) from the date of deduction until the date of deposit with the government

3. Disallowance of Expense

If TDS is not deducted or deposited, 30% of the rent expense will be disallowed while computing business income — leading to higher tax liability for the payer

4. Penalty for Late Filing of TDS Return

₹200 per day under Section 234E until the return is filed

Maximum penalty cannot exceed the TDS amount

5. Prosecution for Wilful Default

Under Section 276B, wilful failure to deposit TDS after deduction can result in rigorous imprisonment from 3 months to 7 years along with a fine

These penalties make it absolutely critical to comply with TDS on rent FY 2026-27 obligations on time.

Proper compliance with TDS on Rent FY 2026-27 can help businesses and individuals avoid unnecessary notices, penalties, and interest charges from the Income Tax Department. Maintaining accurate rent agreements, GST invoices, and TDS records is highly recommended for smooth tax filing and future verification purposes.

Key Changes in TDS on Rent Under New Income Tax Act 2025

Here is a quick summary of what has changed and what remains the same under TDS on rent FY 2026-27 with the new Income Tax Act 2025:

| Parameter | Old Act (1961) | New Act (2025) |

| Section for businesses | 194-I | Section 393(1) [Sl. No. 2(ii)] |

| Section for individuals | 194-IB | Section 393(1) [Sl. No. 2(i)] |

| Rate for land/building | 10% | 10% (unchanged) |

| Rate for machinery | 2% | 2% (unchanged) |

| Annual threshold | ₹2,40,000 | ₹2,40,000 (unchanged) |

| Monthly threshold (individuals) | ₹50,000 | ₹50,000 (unchanged) |

| Nil TDS form | Form 15G/15H | Form 121 |

| TDS credit form | Form 26A | Form 149 |

| Effective date | Until 31 March 2026 | From 1 April 2026 |

The change is primarily structural — aimed at simplifying the law and reducing litigation. The actual financial impact on taxpayers remains the same.

Practical Examples of TDS on Rent FY 2026-27

Example 1 — Business Renting Office Space

ABC Pvt Ltd pays ₹40,000 per month rent for office space to Mr. Sharma.

Annual rent = ₹40,000 × 12 = ₹4,80,000 → Exceeds ₹2,40,000 threshold

TDS rate = 10% (land/building)

Monthly TDS = ₹4,000 | Annual TDS = ₹48,000

Example 2 — Individual Paying House Rent

Agar aap rent ke saath apne monthly expenses aur savings ko better manage karna chahte hain, to hamara detailed monthly budget planning guide bhi padhein.

Rahul (salaried, not under tax audit) pays ₹55,000 per month house rent.

Monthly rent = ₹55,000 → Exceeds ₹50,000 threshold

TDS rate = 2%

TDS deducted once a year (in March) = 2% × ₹55,000 × 12 = ₹13,200

Example 3 — Below Threshold — No TDS

Priya pays ₹18,000 per month as office rent. Annual total = ₹2,16,000 → Below ₹2,40,000 threshold. No TDS required.

FAQs — TDS on Rent FY 2026-27

Q1. What is the TDS rate on rent for FY 2026-27?

For land, building, and furniture the TDS rate is 10% for businesses and companies. For individuals and HUFs not under tax audit, the rate is 2% on any property type.

Q2. What is the threshold limit for TDS on rent in FY 2026-27?

For businesses, the annual threshold is ₹2,40,000. For individuals and HUFs not under tax audit, the monthly threshold is ₹50,000.

Q3. Which section governs TDS on rent in FY 2026-27?

TDS on rent in FY 2026-27 is governed by Section 393 of the Income Tax Act 2025, which replaced Sections 194-I and 194-IB of the Income Tax Act 1961. It is applicable from 1st April 2026.

Q4. Do I need a TAN to deduct TDS on rent as an individual?

No. Individuals and HUFs who are not under tax audit do not need a TAN. They can use their PAN to file Form 26QC for TDS on rent.

Q5. Is TDS applicable on GST portion of rent?

No. TDS on rent is applicable only on the rent amount excluding GST, provided GST is separately mentioned in the invoice or rent agreement.

Q6. What is Form 121 under the new Income Tax Act 2025?

Form 121 is the new form under the Income Tax Act 2025 that replaces the old Form 15G and Form 15H. A landlord can submit Form 121 to the tenant to request nil TDS deduction if their estimated annual income is below the taxable limit.

Q7. What happens if I forget to deduct TDS on rent?

If you fail to deduct TDS on rent, you will be charged interest at 1% per month from the date TDS was due. Additionally, 30% of the rent paid may be disallowed as a business expense, increasing your tax liability.

Q8. Has the TDS rate on rent changed in the new Income Tax Act 2025?

No. The TDS rates on rent remain unchanged. Only the section numbers have changed from 194-I and 194-IB to Section 393 under the new Income Tax Act 2025.

Q9. When should TDS on rent be deposited?

For April to February, TDS must be deposited by the 7th of the following month. For March, the due date is 30th April.

Q10. Can a landlord avoid TDS deduction on rent?

Yes. If the landlord’s total income is below the taxable threshold, they can submit Form 121 to the tenant requesting nil deduction of TDS. This replaces the earlier Form 15G and Form 15H under the Income Tax Act 2025.

Conclusion

TDS on rent FY 2026-27 is a critical tax compliance obligation for both tenants and landlords in India. While the new Income Tax Act 2025 has restructured the TDS framework under Section 393, the rates and threshold limits remain unchanged. Businesses must continue deducting 10% TDS on land and building rent exceeding ₹2,40,000 annually, while individuals paying more than ₹50,000 per month in rent must deduct 2% TDS once a year.

For businesses and salaried individuals paying high-value rent, TDS on Rent FY 2026-27 plays a crucial role in maintaining proper financial records and tax transparency. Keeping updated with the latest rules and compliance deadlines can help both tenants and landlords manage taxation more efficiently.

The key takeaway is this — the law has changed structurally, but your compliance obligations have not reduced. Missing TDS on rent FY 2026-27 deadlines can lead to interest, penalty, and disallowance of expenses. Stay compliant, file your returns on time, and use Form 121 wisely if you are a landlord with lower income.

For more tax planning tips and finance guides, keep reading sksmartdigitalhub.blog.

Pingback: Should You Stop or Continue SIP Investments in 2026?