Every parent in India dreams of giving their daughter the best possible start in life, whether that means quality education, a dignified wedding, or simply financial independence. If you have been searching for a safe, government-backed investment option, the Sukanya Samriddhi Yojana 2026 is one of the strongest choices available today. Backed by the Government of India, this scheme offers guaranteed returns, tax benefits, and long-term wealth creation specifically designed for the girl child.

In this complete guide, we will break down everything you need to know about the Sukanya Samriddhi Yojana 2026, including eligibility, interest rates, deposit limits, tax benefits, withdrawal rules, and how to open an account. Whether you are a new parent or planning ahead for your daughter’s future, this article will help you understand why the Sukanya Samriddhi Yojana 2026 deserves a place in your financial plan.

What Is Sukanya Samriddhi Yojana 2026?

This scheme is a government-backed small savings plan launched under the “Beti Bachao, Beti Padhao” initiative. It is specifically designed to encourage parents and legal guardians to build a financial corpus for their girl child’s future needs, particularly higher education and marriage expenses.

Unlike market-linked investment products, it offers a fixed, government-guaranteed interest rate that is reviewed quarterly. This makes it one of the safest long-term savings instruments in India, especially attractive for risk-averse families who want predictable, compounding returns without exposure to market volatility.

The scheme can be opened at any authorised commercial bank or post office branch across India, making it accessible even in smaller towns and rural areas. Given how systematic and disciplined this scheme is, it has become one of the most searched government savings schemes among Indian parents this year.

Key Features of Sukanya Samriddhi Yojana 2026

Before diving deeper, let’s understand the core structure of this scheme:

Account can be opened for a girl child aged 10 years or below

Minimum annual deposit: Rs. 250

Maximum annual deposit: Rs. 1.5 lakh

Account matures 21 years from the date of opening

Deposits can be made for 15 years from account opening

Only one account is allowed per girl child

A family can open accounts for a maximum of two girl children (with exceptions for twins or triplets)

These features make the scheme flexible enough for families across different income levels, while still enforcing enough discipline to ensure long-term wealth accumulation.

Current Interest Rate Under Sukanya Samriddhi Yojana 2026

One of the biggest attractions of this scheme is its interest rate, which remains higher than most fixed deposits and comparable savings instruments. The interest rate is set by the Ministry of Finance and reviewed every quarter, so it can change slightly depending on economic conditions.

Currently, the scheme offers an interest rate of 8.2% per annum, compounded annually. This rate is calculated on the lowest balance maintained in the account between the fifth and last day of each month, and the interest is credited at the end of the financial year.

Compare this to a typical savings account interest rate of 3-4% or even most fixed deposits that hover around 6.5-7.5%, and you can see why this scheme stands out as a genuinely competitive option for long-term, low-risk savings.

Who Is Eligible for Sukanya Samriddhi Yojana 2026?

Eligibility rules under this scheme are straightforward but important to understand fully:

1.The account must be opened by a natural parent or legal guardian of the girl child

2.The girl child must be an Indian resident

3.The account must be opened before the girl child turns 10 years old

4.A maximum of two accounts per family are allowed, one for each girl child (except in cases of twins or triplets)

5.Non-Resident Indians (NRIs) are currently not eligible to open an account under this scheme

If you meet these criteria, opening an account under this scheme is a relatively simple process that can be completed within a single visit to your nearest bank or post office.

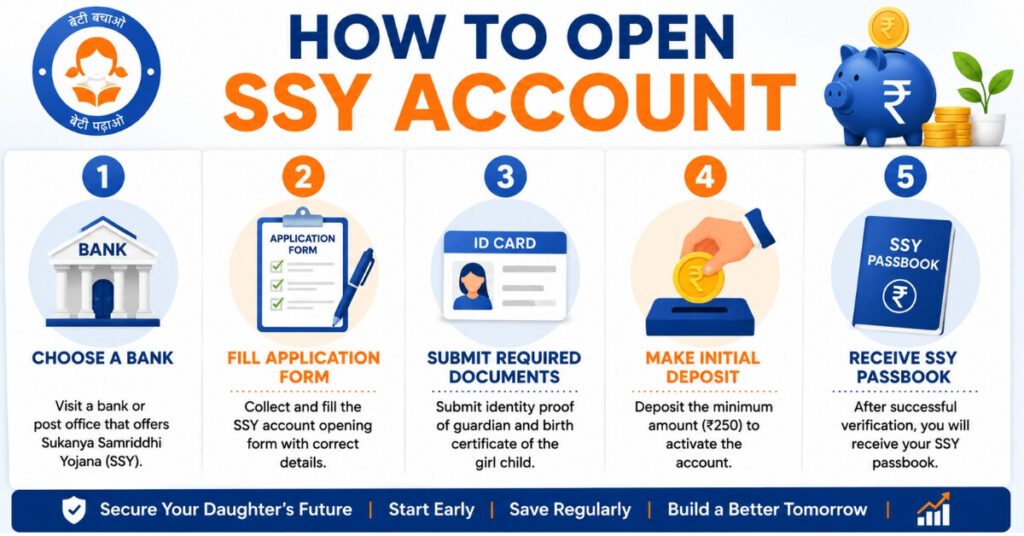

How to Open an Account Under Sukanya Samriddhi Yojana 2026

Opening an account under this scheme involves a few simple steps:

Step 1: Visit any authorised bank branch (SBI, ICICI, HDFC, and most nationalised banks offer this) or your nearest post office.

Step 2: Collect and fill out the SSY account opening form, available both online and offline.

Step 3: Submit the girl child’s birth certificate along with identity and address proof of the parent or guardian (Aadhaar card, PAN card, or passport).

Step 4: Make the initial deposit, which can be as low as Rs. 250.

Step 5: Once verified, the bank or post office will issue a passbook confirming the account has been opened.

The entire process typically takes just one working day, provided all documents are in order.

Documents Required for Sukanya Samriddhi Yojana 2026

To open an account under this scheme, you will need the following documents:

Birth certificate of the girl child

Identity proof of the parent or guardian (Aadhaar, PAN, Voter ID, or Passport)

Address proof (utility bill, Aadhaar, or passport)

Passport-size photographs of the girl child and the guardian

Additional KYC documents as required by the specific bank or post office

Keeping these documents ready in advance will help you avoid delays when opening your account.

Deposit Rules and Limits in Sukanya Samriddhi Yojana 2026

Understanding the deposit structure is essential to making the most of this scheme. Here are the key rules:

Minimum deposit per financial year: Rs. 250

Maximum deposit per financial year: Rs. 1.5 lakh

Deposits can be made in lump sum or in multiple instalments throughout the year

Deposits are required for 15 years from the date of account opening

After 15 years, no further deposits are needed, but the account continues to earn interest until maturity

If the minimum deposit of Rs. 250 is not made in any financial year, the account is treated as a “default account.” However, it can be revived by paying a small penalty along with the minimum required deposit, so even if you miss a year, your account is not permanently lost.

Tax Benefits of Sukanya Samriddhi Yojana 2026

One of the strongest reasons parents choose this scheme is its exceptional tax treatment, often referred to as “EEE” or Exempt-Exempt-Exempt status:

1.Deposits made under this scheme qualify for a deduction of up to Rs. 1.5 lakh per year under Section 80C of the Income Tax Act (applicable only under the old tax regime)

2.Interest earned on the account is completely tax-free

3.The maturity amount, including principal and accumulated interest, is also fully exempt from tax

This triple tax exemption makes this scheme one of the most tax-efficient savings instruments available to Indian families today, especially when compared to other fixed-income products where interest is taxable.

Withdrawal Rules Under Sukanya Samriddhi Yojana 2026

While this scheme is designed as a long-term savings tool, it does allow partial withdrawals under specific conditions:

Up to 50% of the balance can be withdrawn once the girl child turns 18, for higher education expenses

Withdrawal is also permitted if the girl child gets married after turning 18, provided the marriage is at least one month away and not more than three months after the withdrawal date

The account can be closed prematurely in exceptional circumstances such as the death of the account holder or a life-threatening medical condition of the girl child

For education-related withdrawals, proof of admission to a recognised educational institution is usually required.

Sukanya Samriddhi Yojana 2026: A Practical Example

Let’s understand the real wealth-building potential of this scheme with a simple example.

Suppose a parent opens an account for their newborn daughter and deposits Rs. 12,500 every month (Rs. 1.5 lakh annually) for 15 years. Assuming an average interest rate of 8.2% per annum compounded annually, the corpus at maturity (21 years from account opening) could grow to well over Rs. 65-70 lakh, depending on how the interest rate evolves over time.

This example shows why so many financial advisors recommend starting this scheme as early as possible. The longer the money stays invested, the more powerful the effect of compounding becomes, turning even moderate monthly contributions into a substantial corpus by the time your daughter needs it most.

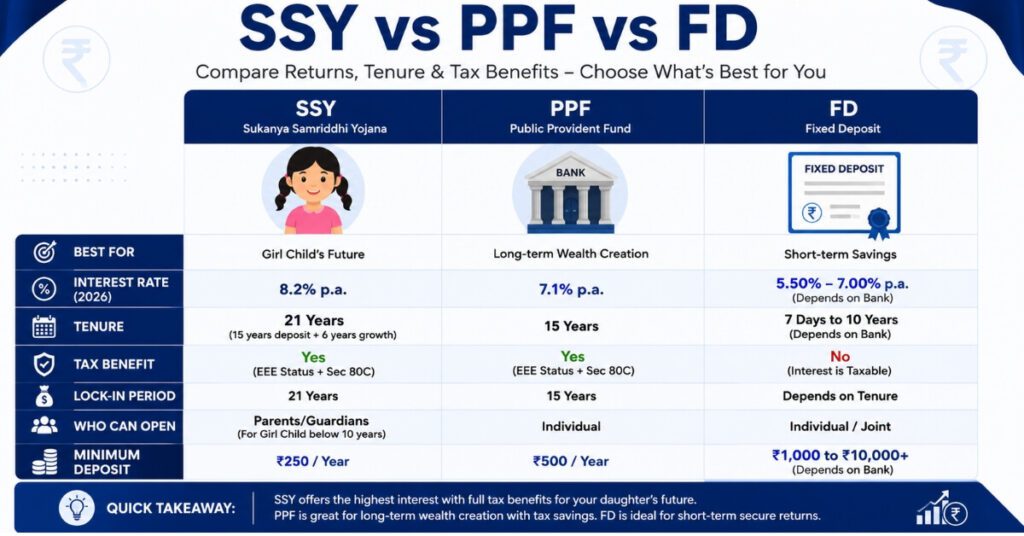

Sukanya Samriddhi Yojana 2026 vs Other Savings Options

It’s natural to wonder how this scheme compares to other popular savings instruments like Public Provident Fund (PPF) or Fixed Deposits (FDs):

Interest Rate: SSY generally offers a higher rate than PPF and most bank FDs

Tax Benefit: Both SSY and PPF offer EEE tax status, while FD interest is fully taxable

Purpose: SSY is exclusively for the girl child, while PPF and FD are open to everyone

Lock-in Period: SSY has a longer effective lock-in (21 years) compared to PPF (15 years) and FDs (varies)

Risk: All three are extremely low-risk, government-backed or bank-guaranteed options

For families with a girl child, this scheme usually offers the best combination of returns, safety, and tax efficiency, making it a preferred choice over generic savings instruments. That said, financial planners often suggest not putting all your savings into a single instrument. A balanced approach, where this account handles the girl child’s dedicated goals while PPF or mutual funds cover broader family objectives like retirement or home ownership, tends to work best for most middle-class Indian households.

Is There a Better Alternative for Every Family?

Not necessarily. While comparison is useful, the right choice ultimately depends on your specific financial goals, time horizon, and risk appetite. Families who prioritise guaranteed, tax-free returns with zero market risk will almost always find this account more suitable than equity-linked options. On the other hand, families with a higher risk tolerance and a longer runway before their daughter needs the funds may choose to combine this scheme with a modest allocation to equity mutual funds for potentially higher, though less certain, growth. There is no one-size-fits-all answer, but for the core, non-negotiable portion of your daughter’s future corpus, few instruments match the safety and tax efficiency offered here.

Common Mistakes to Avoid With Sukanya Samriddhi Yojana 2026

Many parents make avoidable errors while managing their account. Here are some common mistakes to watch out for:

Forgetting to make the minimum annual deposit, which puts the account into default status

Not updating KYC documents when required, which can delay withdrawals later

Assuming NRIs are eligible, when in fact NRI status disqualifies a family from opening or continuing this account

Delaying account opening, thereby losing years of valuable compounding

Not maintaining proper records of deposit receipts and passbook updates

Avoiding these mistakes ensures you get the maximum benefit from your investment over the long term.

Tips to Maximise Returns From This Scheme

Simply opening an account is not enough — how you manage it over the years determines how large the final corpus turns out to be. Here are a few practical tips that can help you get the most out of this investment:

Deposit at the start of the financial year rather than the end, since interest is calculated on the lowest monthly balance, and earlier deposits earn interest for a longer period each year.

Try to deposit the maximum permissible amount if your budget allows, since the compounding effect becomes significantly more powerful over a 21-year horizon.

Set up a standing instruction or auto-debit with your bank so you never accidentally miss the minimum yearly deposit and risk your account going into default status.

Keep your passbook and KYC documents updated regularly, especially if you change your address or contact details, so withdrawals and transfers remain hassle-free later.

Track quarterly interest rate announcements from the Ministry of Finance so you always know the current applicable rate on your account.

Consider this scheme as part of a diversified financial plan for your daughter, alongside health insurance and an emergency fund, rather than relying on a single instrument alone.

Following these simple practices consistently over the years can make a meaningful difference in the final maturity amount your daughter receives, without requiring any additional financial expertise or active management on your part.

If you’re also managing other government savings accounts, staying updated on related services matters just as much. For instance, many families who actively use the Sukanya Samriddhi Yojana 2026 also rely on their EPF accounts for retirement planning, and recently many subscribers faced access issues. You can read our detailed guide on the EPF Passbook Portal Restored to understand how EPFO services have recently improved for millions of members.

For official and updated details directly from the government, you can also refer to the National Savings Institute’s official page on the Sukanya Samriddhi Account Scheme, which outlines the latest rules and interest rate updates.

Frequently Asked Questions About Sukanya Samriddhi Yojana 2026

Q1. What is the current interest rate for Sukanya Samriddhi Yojana 2026?

The current interest rate under the Sukanya Samriddhi Yojana 2026 is 8.2% per annum, compounded annually, though this is reviewed and may change quarterly by the government.

Q2. Can I open more than one Sukanya Samriddhi Yojana 2026 account for the same daughter?

No, only one account per girl child is permitted under this scheme, and it must be opened before she turns 10 years old.

Q3. Is the maturity amount from Sukanya Samriddhi Yojana 2026 taxable?

No, the entire maturity amount, including principal and interest, is completely tax-free under the current tax laws applicable to this scheme.

Q4. Can NRIs open a Sukanya Samriddhi Yojana 2026 account for their daughter?

No, NRIs are currently not eligible to open or continue an account under this scheme.

Q5. What happens if I miss a yearly deposit in my Sukanya Samriddhi Yojana 2026 account?

The account becomes a default account, but it can be revived by paying the minimum deposit along with a small penalty fee.

Q6. Can the Sukanya Samriddhi Yojana 2026 account be transferred between banks or post offices?

Yes, the account can be transferred anywhere in India between authorised banks and post offices without any hassle, in case the family relocates.

Conclusion: Should You Open a Sukanya Samriddhi Yojana 2026 Account?

For any parent looking to secure their daughter’s financial future with a safe, tax-efficient, and high-return savings option, the Sukanya Samriddhi Yojana 2026 stands out as one of the best choices available in India today. With a competitive interest rate, complete tax exemption, and government backing, this scheme offers a rare combination of safety and strong long-term growth.

Whether your goal is funding higher education or planning for your daughter’s wedding, starting this account early can make a meaningful difference to the final corpus you build. The earlier you start, the more you benefit from the power of compounding over the scheme’s long tenure.

Disclaimer

This article is for informational and educational purposes only and should not be considered financial or investment advice. Interest rates, tax rules, and scheme guidelines are subject to change by the Government of India. Please consult a certified financial advisor or refer to official government sources before making any investment decisions related to this scheme.

Pingback: Sensex Prediction Today: 6 Proven Factors Revealed