Kya aapne kabhi socha hai ki jis tarah PF (Provident Fund) seedha aapki salary se kata jaata hai, waisi hi suvidha mutual fund investment ke liye bhi ho sakti hai? SEBI salary mutual fund investment ka yeh sapna ab sach hone ke kaafi kareeb aa gaya hai. Market regulator SEBI ne May 2026 mein ek landmark proposal rakha hai jisme employers apne employees ki salary se directly mutual fund units mein payment kar sakenge.

Yeh ek bahut bada badlaav ho sakta hai — khaaskar un salaried investors ke liye jo regularly invest karna chahte hain lekin manually karne ka time ya discipline nahi bana paate. Is article mein hum is SEBI salary mutual fund investment proposal ko detail mein samjhenge — kya hai yeh proposal, kiske liye hai, kya benefits hain, kya risks hain, aur aapko kya karna chahiye.

SEBI Ka Yeh Naya Proposal Kya Hai?

SEBI (Securities and Exchange Board of India) ne 21 May 2026 ko ek consultation paper jaari kiya. Is paper mein SEBI ne mutual funds mein third-party payments allow karne ki baat ki hai. Abhi existing rules ke mutabik, mutual fund investment sirf usi bank account se ho sakti hai jo investor ka khud ka ho. Lekin is naye SEBI salary mutual fund investment proposal ke baad, employers apne employees ki taraf se mutual fund mein consolidated payment kar sakenge.

Yani agar aapka employer is scheme ka hissa banta hai, toh aapki salary ka ek hissa seedha aapke chosen mutual fund scheme mein invest ho jaayega — bilkul waise jaise PF contribution hota hai.

Yeh proposal SEBI ke Mutual Fund Advisory Committee ki recommendations ke baad aaya hai, jisme industry stakeholders ne kuch special cases mein third-party payments ki chhoot maangi thi.

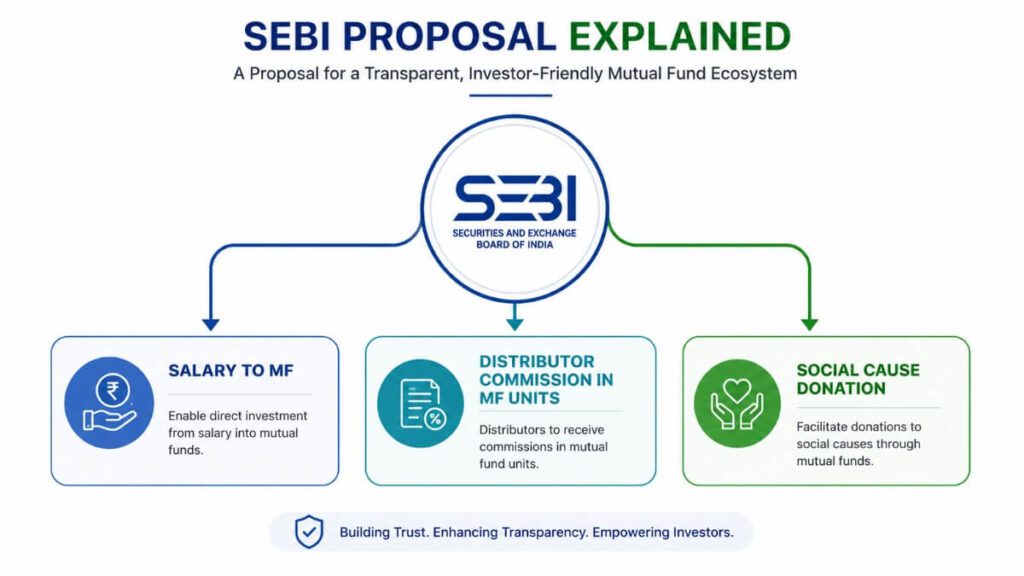

SEBI Salary Mutual Fund Investment Ke 3 Bade Proposals

SEBI ne is consultation paper mein teen important proposals diye hain:

1. Salary Se Seedha Mutual Fund Investment (Payroll-Based MF Investment)

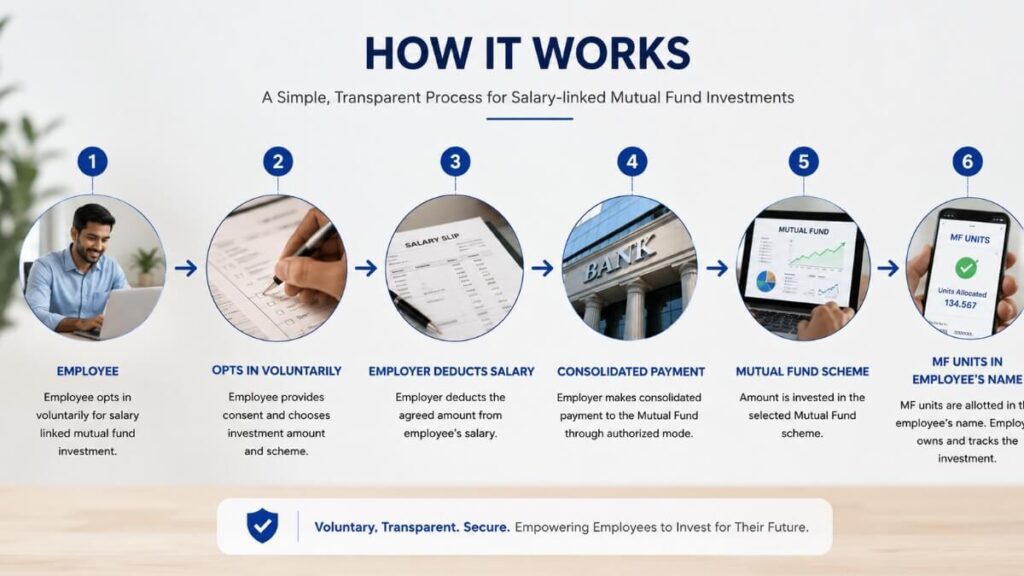

Yeh SEBI salary mutual fund investment proposal ka sabse important hissa hai. Is proposal ke mutabik:

Employees voluntarily apni salary ka kuch hissa MF mein invest kar sakte hain

Employer us amount ko salary se kaat ke directly chosen mutual fund scheme mein daalega

Employer consolidated payment karega — matlab ek baar mein sabhi participating employees ka paisa ek saath MF mein jaayega

Employee khud decide karega ki kaun sa fund choose karna hai

Yeh system un employees ke liye game-changer hai jo discipline ke saath invest karna chahte hain. Jab paisa salary se automatically cut hoga, toh kharch hone ka chance hi nahi rahega.

2. MF Distributors Ko Commission MF Units Mein Milega

Abhi distributors ko commission cash mein milta hai. SEBI ne propose kiya hai ki mutual fund companies apne empanelled distributors ko trail commission partially ya fully MF units ke form mein de sakti hain. Iska faayda yeh hoga ki distributors khud bhi long-term investors ban jayenge, jisse unka focus short-term selling ke bajaye long-term client retention par aayega.

3. Social Causes Ke Liye MF Se Donation

Ek aur innovative proposal hai jisme investors apni MF investment ka kuch hissa, dividend ya redemption proceeds seedha Social Stock Exchange par registered NGOs ko donate kar sakenge. Yeh ek regulated framework hoga jisme transparency poori tarah ensure ki jaayegi.

Yeh SEBI Salary Mutual Fund Investment Kiske Liye Hoga?

Yeh scheme sab ke liye nahi hai — SEBI ne iske liye kuch eligibility conditions propose ki hain:

Listed companies ke employees

EPFO-registered companies ke employees

Asset Management Companies (AMC) ke employees

Sabse zaruri baat — participation bilkul voluntary hoga. Koi bhi employer employee ko force nahi kar sakta. Employee khud decide karega ki invest karna hai ya nahi, aur kaun sa fund choose karna hai.

Abhi Existing Rules Kya Hain? Kyun Change Ho Raha Hai?

Abhi SEBI ke rules ke mutabik, mutual fund investment sirf usi bank account se ho sakti hai jiska naam investor ka ho. Yeh rule anti-money laundering (AML) compliance aur misuse rokne ke liye banaya gaya tha.

Lekin is SEBI salary mutual fund investment proposal ke peeche ka logic yeh hai ki employer-employee relationship ek trusted, verifiable connection hai — jaise EPF mein hota hai. Jab proper KYC, audit trail aur safeguards hon, toh yeh third-party payment risky nahi hai.

SEBI ne khud acknowledge kiya hai ki yeh relaxation tabhi diya jaayega jab strict safeguards in place honge, jaise:

Investor aur payment karne wale ke beech relationship ka verification

Strict KYC compliance

Clear audit trail for all fund flows

Due diligence requirements

SEBI Salary Mutual Fund Investment Se Kya Fayde Honge?

SEBI salary mutual fund investment ka yeh move sirf ek rule change nahi hai — yeh ek bada game changer hai salaried logo ke liye. Socho, jaise PF automatically cut hota hai salary se, waise hi mutual fund mein bhi paisa chala jaayega — bina kuch kiye! Bahut saare countries mein yeh system already chal raha hai aur log bahut achha wealth create kar rahe hain. India mein bhi yeh SEBI salary mutual fund investment scheme un crores of employees ke liye opportunity hai jo invest karna chahte hain but time ya discipline ki wajah se nahi kar paate.

Yeh SEBI salary mutual fund investment proposal implement hone se kaafi saare positive changes aa sakte hain:

Automatic Investment Discipline

Jab salary se automatically mutual fund mein paisa jaayega, toh investor ko har mahine manually SIP chalane ki zarurat nahi hogi. Yeh financial discipline banane ka sabse effective tarika hai.

Mutual Fund Penetration Badega

India mein abhi bhi bahut saare salaried employees stock market ya mutual funds mein invest nahi karte. Salary-based automatic investment se mutual fund penetration tier-2, tier-3 cities mein bhi badh sakta hai.

Inflation Ke Khilaaf Better Protections

Fixed FD ya savings account ke bajaye mutual fund mein invest karna long-term mein inflation ko beat karne ka better tarika hai. SEBI salary mutual fund investment system se zyada log is benefit ko pa sakte hain.

Badhte fuel prices aur inflation ke is daur mein apna budget manage karna bahut zaroori hai. Jaanein Petrol Price Hike Effect on Common Man aur apni savings kaise bachayein.

Retirement Corpus Building

Regular, automatic SIP-like investment retirement planning ke liye bahut effective hai. PF ke saath-saath MF investment hogi toh retirement corpus double track par build hoga.

Employers Ko Bhi Faayda

Employers isse ek additional employee benefit ke roop mein offer kar sakte hain, jisse employee retention aur satisfaction improve ho sakta hai.

Kya Koi Risk Bhi Hai?

Har naye proposal ke saath kuch concerns bhi hote hain. SEBI salary mutual fund investment ke sandarbh mein kuch potential risks hain:

Market Risk: Mutual funds market-linked instruments hain. PF ke khaas khilaaf, yahan guaranteed returns nahi hain. Employees ko yeh samajhna hoga ki unka paisa market ke ups-downs ke saath chalega.

Fund Selection ki Responsibility: Employee ko khud sahi fund choose karna hoga. Galat fund choose karne par returns disappointing ho sakte hain.

Employer Compliance Burden: Employers ko extra compliance karna padega — audit trails maintain karna, consolidated payments karna, employee data handle karna.

Privacy Concerns: Employer ko employee ke investment choices ka pata chalega, jo kuch logon ko uncomfortable laga sakta hai.SEBI salary mutual fund investment ka sabse bada plus point yeh hai ki yeh bilkul voluntary hai — koi pressure nahi, koi force nahi. Aap khud decide karo ki invest karna hai ya nahi, kitna karna hai, aur kaun sa fund choose karna hai. Yeh flexibility hi is scheme ko baaki government investment schemes se alag banati hai. Aur jab employee khud apna fund choose karega, toh uski interest bhi rahegi apni investment track karne mein — jo long term mein bahut beneficial hai.

Abhi Yeh Sirf Proposal Hai — Aage Kya Hoga?

Yeh yaad rakhna zaroori hai ki abhi SEBI salary mutual fund investment ek consultation paper ke roop mein hai, final rule nahi. SEBI ne public se feedback maanga hai. Iske baad:

Lekin yeh wait karne ki wajah nahi hai — balki yeh sahi time hai prepare karne ka. Jab bhi SEBI salary mutual fund investment officially launch ho, aap ready rehna chahiye. Apna KYC complete karo, different fund categories samjho, aur apne financial goals list karo. Jo log pehle se prepared hain, woh scheme launch hote hi pehle adopters mein honge — aur compounding ka faayda bhi zyada milega unhe jo jaldi start karte hain.

1 .Public comments process hogi

2 .SEBI final guidelines taiyaar karega

3 .Operational norms working out honge (probably AMFI aur AMCs milkar karenge)

4 .Phir actual implementation hoga

Implementation timeline abhi officially announce nahi hui hai, lekin industry experts maan rahe hain ki agar consultation period smoothly jaata hai, toh yeh FY2026-27 tak implement ho sakta hai.

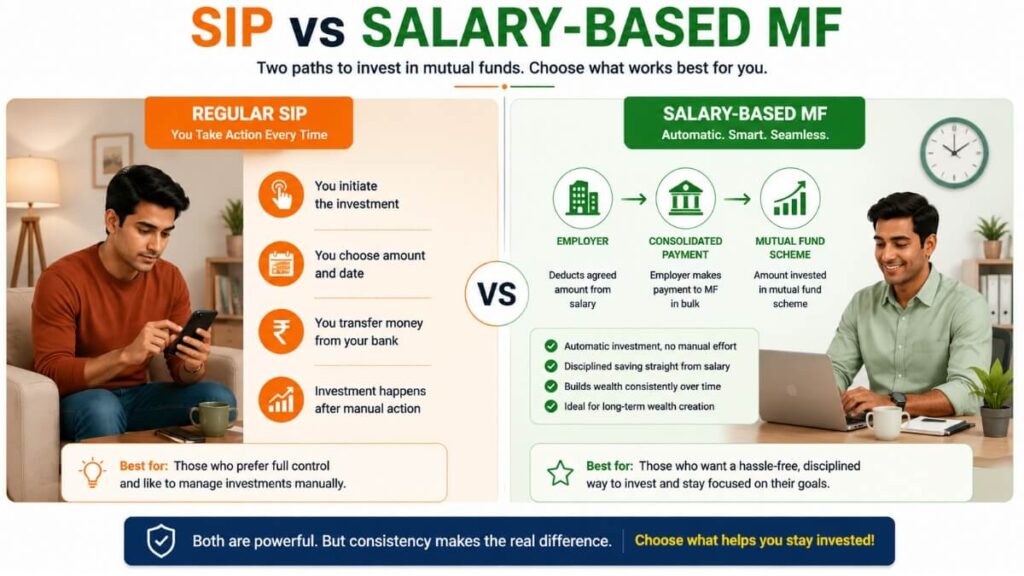

Salary-Based MF Investment vs. Regular SIP: Kya Farq Hai?

| Feature | Regular SIP | SEBI Proposed Salary-Based MF |

| Payment Source | Apna Bank Account | Employer (Salary Deduction) |

| Manual Action | Har mahine set karna padta hai | Automatic, employer ke through |

| Fund Choice | Investor ka | Investor ka (voluntary) |

| Guaranteed Returns | Nahi | Nahi |

| Existing Rule | Allowed | Abhi proposal stage |

| Tax Benefit | Fund type pe depend | Fund type pe depend |

| Target Audience | Koi bhi | Salaried (listed/EPFO companies) |

SEBI Salary Mutual Fund Investment: Investors Ko Kya Karna Chahiye Abhi?

Yeh proposal abhi final nahi hua hai, isliye koi immediate action ki zarurat nahi hai. Lekin kuch preparatory steps aap abhi se le sakte hain:

Step 1: KYC Complete Karein

Agar aapka mutual fund KYC abhi tak nahi hua hai, toh abhi kar lein. CAMS ya Karvy ke through online KYC easily ho jaata hai.

Aur agar aap salaried hain aur abhi tak ITR file nahi ki, toh pehle yeh bhi zaroori hai — ITR Filing Online Kaise Kare — ghar baithe sirf 1 ghante mein apni ITR file karo!

Step 2: Apne Financial Goals Clear Karein

Salary-based investment start karne se pehle yeh decide karein ki aap kis goal ke liye invest karna chahte hain — retirement, child education, ya emergency fund.

Step 3: Fund Categories Samjhein

Large cap, mid cap, flexi cap, ELSS — in sabka basic knowledge rakhein taaki jab yeh facility aaye toh sahi fund choose kar sakein.

Step 4: HR Department Se Poochein

Agar aap kisi listed ya EPFO-registered company mein hain, toh apne HR se poochein ki kya company is facility ko adopt karne ka plan hai.

FAQs: SEBI Salary Mutual Fund Investment Ke Baare Mein Aapke Sawal

Q1. Kya employer mere mutual fund investment ki details dekh sakta hai?

SEBI ke proposal ke mutabik, employer ko invest kiye gaye paisa ka pata hoga lekin fund performance ya detailed account information ke baare mein scope abhi clearly define nahi hua hai. Final guidelines mein privacy norms specify ki jaayengi.

Q2. Kya participation compulsory hoga?

Bilkul nahi. SEBI ne clearly mention kiya hai ki yeh facility purely voluntary hogi. Koi bhi employee participate karne ke liye force nahi kiya jaayega.

Q3. Kaunsi companies ke employees is scheme ka faayda utha sakenge?

SEBI ke proposal ke mutabik, listed companies, EPFO-registered companies aur AMC employees eligible honge.

Q4. Kya main khud fund choose kar sakta hoon?

Haan, employee khud decide karega ki uski salary ka paisa kaun se mutual fund scheme mein jaayega.

Q5. Agar main fund change karna chaahoon toh kya hoga?

Is par abhi detailed norms nahi aaye hain, lekin standard mutual fund rules ke hisaab se investor fund switch kar sakta hai. Final operational guidelines mein yeh clearly mention hoga.

Q6. Kya yeh PF ki tarah tax-free hoga?

Nahi. Mutual fund investment ki taxation fund type pe depend karti hai. ELSS funds pe 80C ke under tax benefit milta hai, lekin baaki equity funds pe LTCG/STCG tax lagta hai.

Q7. Agar company band ho jaaye ya main job chhod doon toh?

MF units aapke naam par hote hain, employer ke nahi. Job chhodne ke baad bhi aapki MF holdings safe rahegi. Sirf nayi deductions band ho jaayengi.

Q8. Yeh scheme kab tak implement ho sakti hai?

Abhi yeh consultation paper stage par hai. SEBI public feedback process ke baad final guidelines taiyaar karega. Industry experts FY2026-27 implementation ki umeed kar rahe hain.

Q9. Kya SEBI salary mutual fund investment se market mein zyada paisa aayega?

Haan. Agar crores of salaried employees is scheme se jud jaayein, toh mutual fund industry mein regular inflows kaafi badh sakte hain, jo overall market stability ke liye bhi positive hoga.

Q10. Main is SEBI proposal par apna opinion kahan share kar sakta hoon?

SEBI ne public consultation paper jaari kiya hai. Aap SEBI ki official website sebi.gov.in par jaake apna feedback submit kar sakte hain.

Is proposal ke baare mein zyada detail ke liye aap SEBI Official Website par jaake consultation paper padh sakte hain.

Aaj jab inflation upar ja rahi hai aur FD returns itne low hain, tab SEBI salary mutual fund investment ek bahut smart option ban sakta hai. Yeh specially unke liye perfect hai jo baar baar kehte hain — “yaar invest karna tha but ho nahi paya!” — kyunki jab salary se automatically cut hoga toh sochna hi nahi padega. Toh is SEBI salary mutual fund investment proposal ko seriously lo aur abhi se apni financial planning ready karo — kyunki jo log early start karte hain, wahi aage jaate hain

Conclusion

SEBI salary mutual fund investment proposal ek bold aur investor-friendly initiative hai. Agar yeh successfully implement hota hai, toh India mein mutual fund participation dramatically badh sakta hai — khaaskar un millions of salaried employees mein jo invest karna chahte hain lekin discipline ya convenience ki wajah se nahi kar paate.

Yeh proposal yeh bhi dikhata hai ki SEBI laqataar mutual fund industry ko zyada accessible, transparent aur investor-friendly banana chahta hai. PF ki tarah MF investment — yeh concept simple hai, powerful hai, aur waqt ki zarurat bhi hai.

Agar aap salaried hain, toh is SEBI salary mutual fund investment scheme ko closely follow karte rahein. Apna KYC ready rakhein, financial goals clear karein, aur jab yeh facility officially launch ho, toh pehle adopters mein shaamil honein.

Disclaimer: Yeh article sirf educational purpose ke liye hai. Mutual fund investments market risks ke adheen hain. Invest karne se pehle apne financial advisor se zaroor salah lein.

Pingback: Why Is Indian Rupee Falling in 2026? Full Guide