Building your first investment portfolio for beginners can feel overwhelming, especially with so many options like stocks, bonds, mutual funds, ETFs, and REITs available today. Many people delay investing simply because they do not know where to start, and that hesitation often costs them years of potential growth. This guide breaks down exactly how to create an investment portfolio for beginners in a simple, practical way, without confusing jargon or unnecessary complexity.

Whether you are twenty-two and just starting your first job, or forty-five and finally ready to take control of your finances, the principles behind an investment portfolio for beginners remain the same. You need clarity, patience, and a plan that matches your goals. This article walks through every step, from understanding what a portfolio actually is, to choosing the right mix of assets, to avoiding common mistakes that trip up new investors.

What Is an Investment Portfolio?

An investment portfolio is simply a collection of financial assets you own, such as stocks, bonds, mutual funds, exchange-traded funds, real estate investment trusts, and cash. The purpose of an investment portfolio for beginners is not to pick the single best stock or fund, but to build a balanced collection of assets that work together to grow your money over time while managing risk.

Think of it like a recipe. No single ingredient makes the dish; it is the combination that creates something valuable. Similarly, an investment portfolio for beginners is not about finding one perfect investment, but about combining different asset types so that if one underperforms, others can help balance the overall result.

Why You Need an Investment Portfolio for Beginners

Many new investors make the mistake of putting all their money into a single stock or a trending asset because they heard about it online. This approach is risky and can lead to significant losses. A properly structured investment portfolio for beginners spreads risk across multiple asset classes, industries, and even geographic regions, reducing the impact of any single investment performing poorly.

Beyond risk management, having an investment portfolio for beginners also helps you stay disciplined. When you have a clear plan for how your money is allocated, you are less likely to panic during market downturns or chase short-term trends. Instead, you can focus on your long-term financial goals, whether that is retirement, buying a home, or building generational wealth.

Step 1: Set Clear Financial Goals Before Building an Investment Portfolio for Beginners

Before you invest a single rupee or dollar, you need to know why you are investing. Are you saving for retirement in thirty years, a home down payment in five years, or your child’s education in fifteen years? Your timeline directly affects how you should structure your investment portfolio for beginners.

Short-term goals, those within three years, generally call for safer, more liquid investments. Long-term goals, such as retirement, allow for more exposure to growth-oriented assets like stocks, since you have time to ride out market volatility. Writing down your goals, along with realistic timelines, gives your investment portfolio for beginners a clear purpose rather than being a random collection of assets.

Step 2: Build an Emergency Fund First

Before diving into the world of investing, make sure you have three to six months of living expenses saved in an easily accessible account. This emergency fund acts as a safety net, so you never have to sell your investments at a loss during a personal financial emergency. Skipping this step is one of the most common mistakes among beginners rushing to build an investment portfolio without a proper foundation.

Step 3: Understand Your Risk Tolerance

Risk tolerance refers to how much volatility you can handle emotionally and financially. Someone in their twenties with a stable income can typically accept more risk than someone nearing retirement. Understanding your personal comfort level with market ups and downs is essential before you start allocating assets, because an investment portfolio for beginners should match your temperament, not just your goals.

Ask yourself honestly: if your investments dropped twenty percent in a month, would you panic and sell, or would you stay calm and wait for recovery? Your answer helps determine whether you should lean toward conservative, moderate, or aggressive asset allocation.

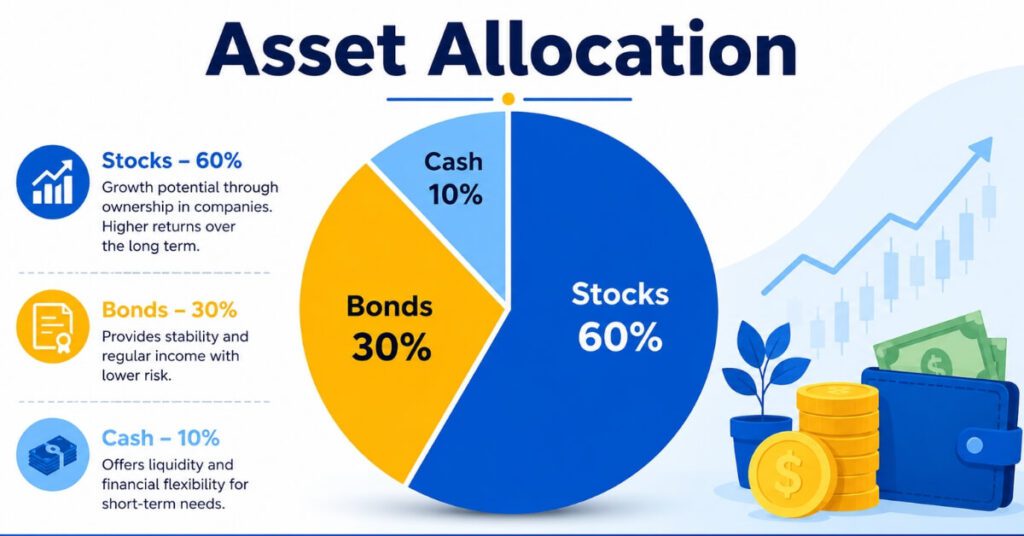

Step 4: Choose the Right Asset Allocation

Asset allocation is the process of dividing your money among different investment categories, such as stocks, bonds, cash, and alternative assets like real estate or commodities. This is arguably the most important decision when building an investment portfolio for beginners, because studies consistently show that asset allocation has a bigger impact on long-term returns than individual stock selection.

A common starting point for a beginner-friendly investment portfolio is a mix of sixty percent stocks and forty percent bonds, though this can be adjusted based on age and risk tolerance. Younger investors with longer time horizons might lean more heavily toward stocks, perhaps eighty or ninety percent, while those closer to retirement may prefer a more conservative split favoring bonds and cash equivalents.

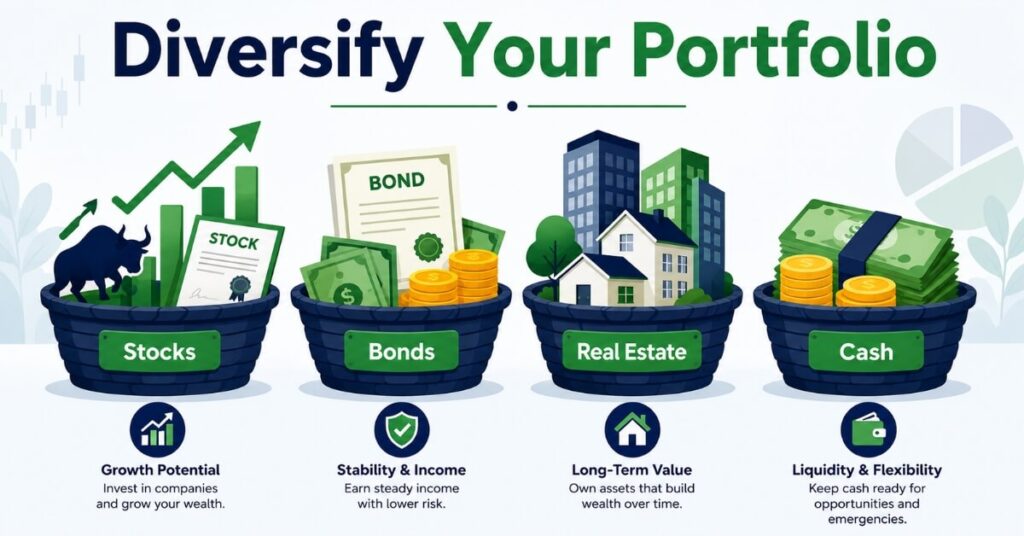

Step 5: Diversify Across Asset Classes

Diversification means spreading your investments across different types of assets, sectors, and geographic regions so that poor performance in one area does not sink your entire portfolio. A well-diversified investment portfolio for beginners typically includes:

Stocks: Ownership shares in companies, offering growth potential but higher volatility.

Bonds: Loans to governments or corporations, offering steady income with lower risk.

Mutual Funds and ETFs: Pooled investments that instantly diversify your money across dozens or hundreds of underlying securities.

Real Estate Investment Trusts: A way to invest in real estate without directly buying property.

Cash and Cash Equivalents: Provides liquidity and stability during market downturns.

By combining these categories thoughtfully, an investment portfolio for beginners becomes more resilient to the unpredictable swings of any single market or sector.

Step 6: Choose Low-Cost Index Funds and ETFs

For most beginners, picking individual stocks is not the ideal starting point, since it requires significant research, time, and expertise. Instead, low-cost index funds and exchange-traded funds offer instant diversification at a fraction of the cost of actively managed funds. These funds track a broad market index, such as a total stock market index or a bond index, giving your investment portfolio for beginners exposure to hundreds of companies with a single purchase.

Over time, fees can quietly eat away at your returns, so paying attention to expense ratios matters. Even a difference of one percent in annual fees can cost you a significant amount over several decades due to the power of compounding.

Step 7: Automate Your Contributions

One of the simplest ways to stay consistent is to automate your investments. Setting up automatic monthly transfers into your investment accounts removes the temptation to time the market or skip contributions during busy months. This strategy, often called dollar-cost averaging, means you buy more shares when prices are low and fewer when prices are high, smoothing out your average purchase price over time.

For anyone building an investment portfolio for beginners, automation also removes emotional decision-making from the equation, which is often the biggest obstacle to long-term investing success.

Step 8: Review and Rebalance Periodically

Over time, some assets in your portfolio will grow faster than others, shifting your original allocation. For example, if stocks perform well, they might grow from sixty percent of your portfolio to seventy percent, increasing your overall risk beyond your comfort level. Rebalancing means periodically adjusting your holdings back to your target allocation, typically once or twice a year.

This discipline ensures your investment portfolio for beginners continues to reflect your goals and risk tolerance, rather than drifting based on market performance alone.

Common Mistakes to Avoid

Even with the best intentions, many beginners make avoidable errors when starting their investment journey. Trying to time the market, chasing hot trends, ignoring fees, and failing to diversify are among the most frequent pitfalls. Another common issue is checking your portfolio too often, which can lead to emotional decisions based on short-term market noise rather than long-term strategy.

Patience is perhaps the most underrated skill in investing. Markets fluctuate in the short term, but historically, they have trended upward over longer periods. Staying invested through volatility, rather than reacting to every headline, is often what separates successful long-term investors from those who struggle.

If you are looking for additional ways to grow your income alongside your investments, you might also explore practical options like earning money from mobile as a student, which can provide extra funds to contribute toward your growing investment portfolio for beginners. (internal link)

How Much Money Do You Need to Start?

One of the biggest myths is that you need a large sum of money to start investing. In reality, many brokerages and investment platforms allow you to begin with very small amounts, sometimes as little as a few dollars or a few hundred rupees. The key is consistency, not the initial amount. Starting small and increasing your contributions as your income grows is a perfectly valid approach to building long-term wealth.

According to resources like Investor.gov, understanding asset allocation and diversification is one of the most important steps for new investors, regardless of how much capital they start with. (external link)

Choosing the Right Investment Account

Before you can start building your investment portfolio for beginners, you need the right account. Depending on your country and goals, this could be a retirement account, a taxable brokerage account, or a tax-advantaged savings vehicle. Each option has different tax implications, contribution limits, and withdrawal rules, so it is worth researching what is available in your region before committing your money.

Retirement-focused accounts often provide tax benefits that make them an attractive starting point, especially for long-term goals. However, if you need more flexibility or plan to use the money before retirement age, a standard brokerage account might be more suitable for your investment portfolio for beginners.

Staying Committed for the Long Term

Building wealth through investing is rarely a fast process. It requires patience, consistency, and a willingness to stay the course even when markets feel uncertain. The beauty of a well-structured investment portfolio for beginners is that it does not require constant attention or expert-level knowledge. Once your allocation is set, automated, and periodically reviewed, you can focus on your career, family, and other priorities while your money works in the background.

Remember that every experienced investor started exactly where you are now, uncertain and perhaps a little intimidated. The difference between those who build wealth and those who do not often comes down to simply getting started and staying consistent.

Useful Tools and Apps for New Investors

Technology has made it far easier for new investors to get started without needing a finance degree or a broker on speed dial. Many brokerage apps now offer fractional share investing, letting you buy a small slice of an expensive stock instead of a full share. Robo-advisors are another popular option, using algorithms to automatically build and manage a diversified mix of assets based on your goals and risk tolerance, often for a small annual fee.

Budgeting apps can also play a supporting role by helping you identify how much you can realistically set aside each month for investing. When your everyday spending is organized and tracked, it becomes much easier to commit to consistent contributions rather than investing only when you happen to have leftover cash at the end of the month.

Before choosing any platform, compare fees, minimum deposit requirements, available asset types, and customer support quality. A slightly lower fee or a more intuitive app interface can make a meaningful difference over the many years you will likely be investing.

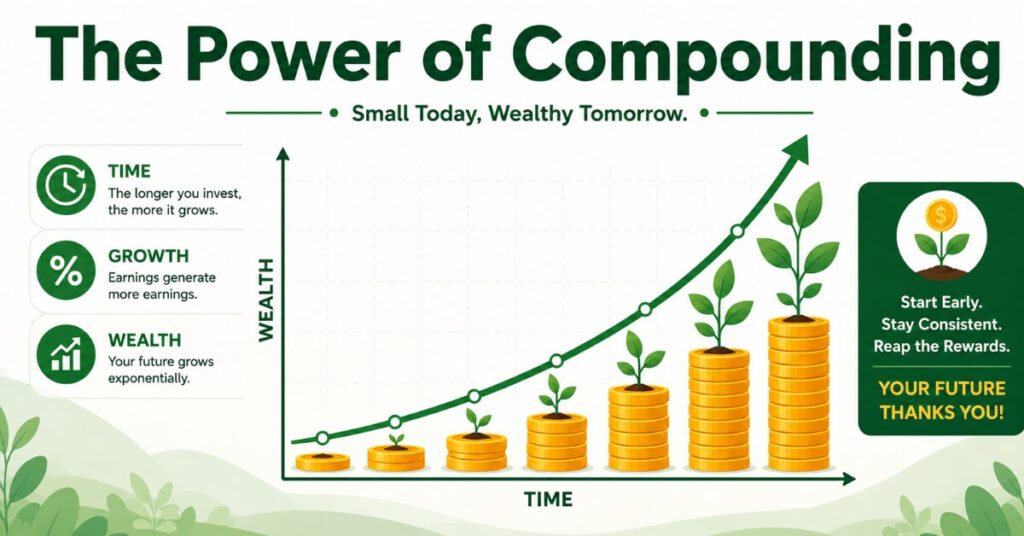

The Role of Time and Compounding

Time is one of the most powerful forces in investing, often more influential than the amount of money you start with. Compounding occurs when your investment returns start generating their own returns, creating a snowball effect that accelerates over the years. A person who starts investing modestly in their twenties can often end up with more wealth by retirement than someone who invests larger amounts but starts a decade later.

This is why delaying the decision to start, even by a few years, can be costly. Every year you wait is a year of potential compounding growth that cannot be recovered later, no matter how much extra money you try to contribute afterward. Starting early, even with modest amounts, gives your money more time to grow through market cycles and reinvested returns.

Balancing Debt and Investing

Many beginners wonder whether they should pay off debt first or start investing right away. The answer often depends on the interest rate of the debt in question. High-interest debt, such as credit card balances, typically costs more than what you are likely to earn from investing, so paying it down aggressively usually makes more financial sense before committing significant funds to the markets.

On the other hand, low-interest debt, such as certain student loans or a mortgage, may not need to be paid off aggressively before you begin investing, especially if your employer offers matching contributions on a retirement account. In such cases, contributing enough to capture the full employer match while making minimum payments on low-interest debt can be a reasonable middle ground.

Staying Informed Without Overreacting

Financial news moves quickly, and headlines are often designed to grab attention rather than provide calm, measured guidance. New investors sometimes fall into the trap of reacting to every piece of market news, buying or selling based on short-term predictions that rarely play out as expected. It is helpful to stay generally informed about the economy and markets, but making frequent changes to your strategy based on daily headlines usually does more harm than good.

Instead, consider setting a fixed schedule, such as once a quarter, to review broader financial news and see whether anything materially affects your long-term plan. This approach keeps you informed without letting short-term noise disrupt a strategy built for the long run.

Frequently Asked Questions

Q1.What is the best investment portfolio for beginners?

There is no single best portfolio for everyone, since the ideal mix depends on your goals, timeline, and risk tolerance. However, a diversified investment portfolio for beginners typically includes a mix of stocks, bonds, and low-cost index funds tailored to your individual circumstances.

Q2.How much money do I need to start investing?

You can start with very small amounts through many modern investment platforms. The most important factor is consistency over time, not the size of your initial contribution.

Q3.Should beginners invest in individual stocks?

Most financial experts recommend that beginners focus on diversified funds, such as index funds or ETFs, rather than individual stocks, since diversification reduces risk while individual stock picking requires significant research and expertise.

Q4.How often should I rebalance my portfolio?

Reviewing and rebalancing your portfolio once or twice a year is generally sufficient for most long-term investors, helping maintain your intended asset allocation without excessive trading.

Q5.Is it risky to invest as a beginner?

All investing carries some level of risk, but a well-diversified investment portfolio for beginners, combined with a long-term perspective, can help manage and reduce that risk over time.

Conclusion

Creating your first investment portfolio for beginners does not have to be complicated or intimidating. By setting clear goals, understanding your risk tolerance, diversifying across asset classes, choosing low-cost funds, and automating your contributions, you can build a solid foundation for long-term financial growth. The most important step is simply beginning, even with a small amount, and staying consistent as your knowledge and confidence grow over time. With patience and discipline, your investment portfolio for beginners can steadily evolve into a powerful tool for building lasting wealth.

Disclaimer

This article is for informational and educational purposes only and should not be considered personalized financial advice. Investing involves risk, including the potential loss of principal. Please consult a qualified financial advisor before making any investment decisions based on your individual circumstances.

Pingback: Cash Transaction Limit Income Tax: 8 Rules & Penalty