If you have ever been rejected for a loan or offered a higher interest rate than expected, your credit score is likely the reason. In India, your CIBIL score — the three-digit number that determines your financial credibility — decides whether you get the loan, at what rate, and how fast. The empowering reality is that no matter where your score stands today, you can learn how to improve credit score steadily and meaningfully with the right habits.

This complete guide covers seven proven, practical tips that actually work in 2026. Whether your score is 500, 600, or 680, these steps will help you boost it to 750 and beyond.

What Is a Credit Score and Why Does It Matter?

A credit score is a three-digit number — ranging from 300 to 900 in India — calculated by credit bureaus based on your borrowing and repayment history. The four licensed credit bureaus in India are TransUnion CIBIL, Experian, Equifax, and CRIF High Mark. Among these, TransUnion CIBIL is the most widely used, which is why the term “CIBIL score” is used interchangeably with “credit score” in India.

Your score affects far more than just loan approvals:

Loan interest rates — a score above 750 often gets you 1–2% lower interest, saving lakhs over a home loan tenure

Credit card eligibility — premium cashback and rewards cards require a score of 750+

Loan sanction speed — banks approve applications from high-score customers faster

Loan amount — higher scores unlock higher eligible amounts

Rental agreements — many landlords and property agencies now check CIBIL before renting

A low score is not a permanent condition. Once you understand how to improve credit score through disciplined habits, every one of these areas improves with it.

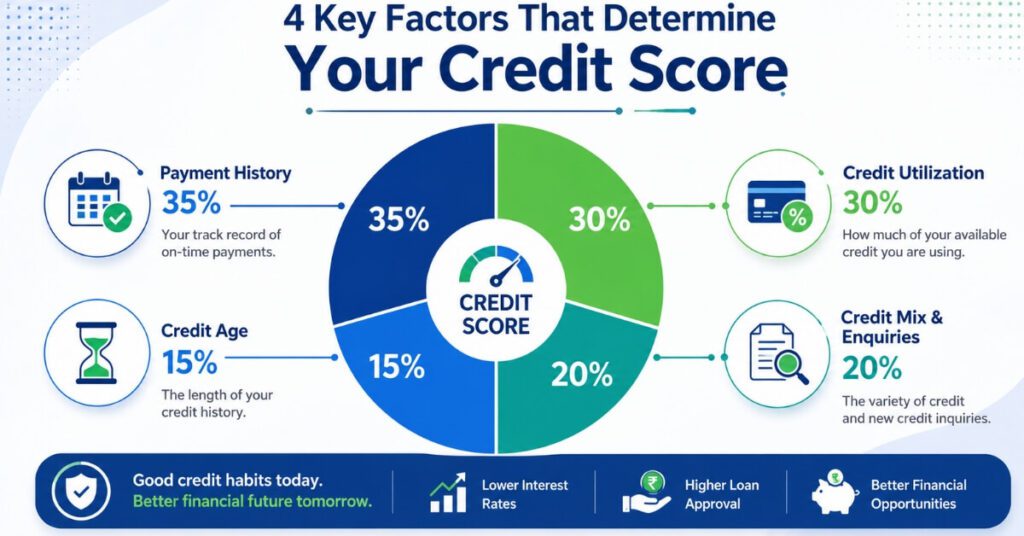

How Is Your Credit Score Calculated?

Understanding the calculation helps you know exactly where to focus your energy. The four main components are:

Payment History (35%): Do you pay EMIs and credit card bills on time every month? This is the single biggest factor. One missed payment can drop your score by 50–100 points.

Credit Utilization (30%): How much of your available credit limit are you using? Lenders prefer this ratio to be below 30%. High utilization signals financial stress.

Credit Age (15%): How long have you held credit accounts? Older accounts improve your score. Closing old cards reduces your average credit age.

Credit Mix and New Enquiries (20%): A balanced mix of secured loans (home, car) and unsecured credit (cards, personal loans) strengthens your profile. Too many loan applications in a short period lowers your score through hard enquiries.

Now let us look at the seven tips that will genuinely help you understand how to improve credit score in 2026.

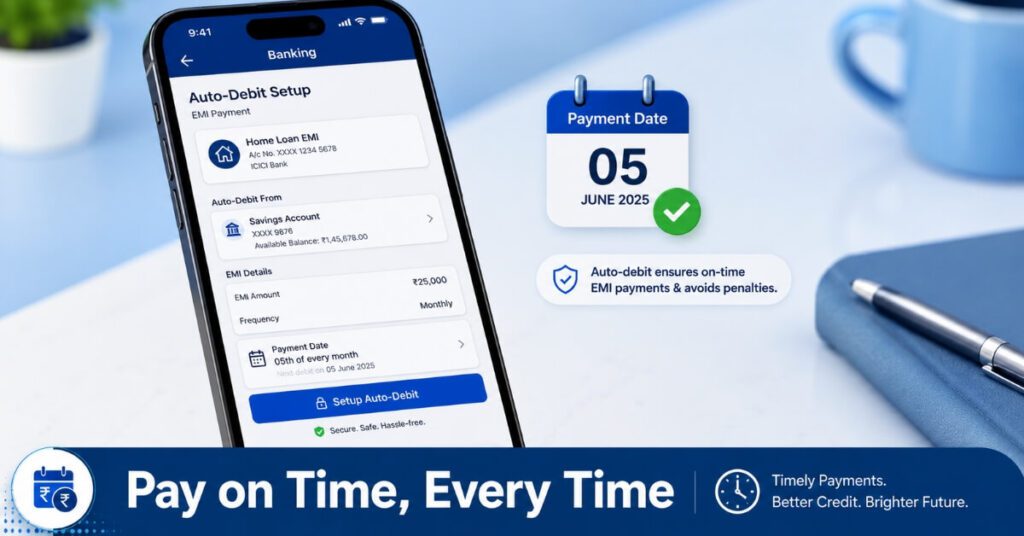

Tip 1: Pay Every EMI and Bill on Time — Without Exception

The most powerful and immediate step in learning how to improve credit score is to pay every EMI, credit card bill, and loan instalment on time — without a single miss. Payment history accounts for 35% of your score, making it the most impactful lever you have.

Even one missed payment leaves a negative mark that can suppress your score for months. Banks report payment data to credit bureaus every 15 days as mandated by the RBI. So a late payment gets recorded quickly.

Practical steps to never miss a payment:

Set up ECS auto-debit for all loan EMIs directly from your bank account

Enable autopay for your credit card for the full outstanding amount — not just the minimum due

Set phone reminders 3 days before each due date as a safety net

If cash is tight, cut discretionary spending rather than delay payments

Paying only the minimum due on credit cards avoids late fees but does not significantly help your score — it keeps your outstanding balance high and utilization elevated. Anyone who is serious about how to improve credit score must pay the full outstanding amount every month.

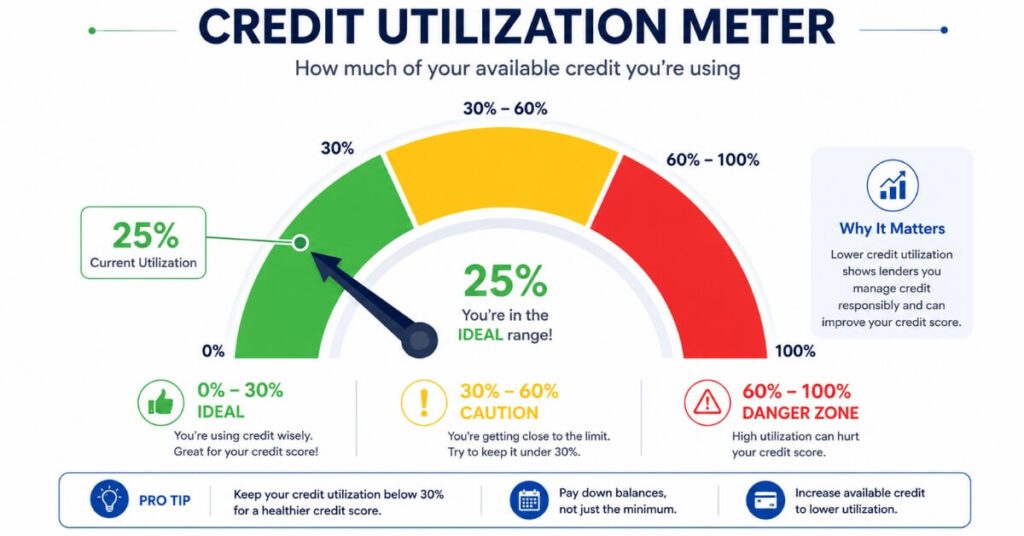

Tip 2: Keep Credit Utilization Below 30%

Credit utilization is the second most influential factor when learning how to improve credit score. It is calculated as: (Total credit used ÷ Total credit limit) × 100.

If your combined credit card limit is ₹2 lakh and you regularly spend ₹1.5 lakh, your utilization is 75% — dangerously high in any lender’s eyes.

How to reduce credit utilization:

Target below 30% — ideally below 20% for maximum benefit

Pay your credit card bill mid-cycle (before the statement is generated) to reduce reported balance

Request a credit limit increase from your bank — if granted, your utilization drops immediately without spending less

Spread spending across multiple cards rather than maxing one

Reducing utilization is one of the fastest ways of how to improve credit score — results are often visible within one to two billing cycles.

Tip 3: Check Your Credit Report for Errors and Dispute Them

Studies indicate that 30–40% of credit reports in India contain at least one inaccuracy. These errors can silently drag your score down for years without you knowing. Fixing them is often the quickest path in how to improve credit score without changing any financial behaviour.

Common errors found in Indian credit reports:

Loans you never took — a possible sign of identity fraud

EMI payments marked as missed when you paid on time

Accounts settled or closed but still showing as active

Duplicate entries for the same loan account

Wrong personal details — incorrect PAN, name spelling, or date of birth

Steps to check and dispute errors:

Step 1: Download your free annual CIBIL report from the TransUnion CIBIL official website

Step 2: Review every entry carefully — especially payment history and account status

Step 3: Raise a dispute through the official CIBIL dispute portal

Step 4: The bureau contacts the lender and resolves within 30–45 days

After correction, your score updates to reflect your accurate financial history — often resulting in a gain of 30–100 points. This is why checking your report is a critical step in how to improve credit score fast.

Tip 4: Do Not Close Old Credit Cards

Closing old credit cards is one of the most common mistakes people make when trying to figure out how to improve credit score. It feels responsible — fewer cards, less complexity — but it actually hurts your score in two ways simultaneously.

First, it reduces your total credit limit, which raises your utilization ratio immediately. Second, it shortens your average credit history, which reduces your credit age score.

What to do instead:

Keep old credit cards open, even if you rarely use them

Make a small purchase — groceries, a utility bill — once every two to three months to keep the account active

Avoid closing any card that has a long history and zero or low annual fee

Close a card only if the annual fee is too high to justify, or you genuinely cannot control spending on it. Understanding this mistake is key to how to improve credit score without making it worse.

Tip 5: Limit New Loan and Credit Card Applications

Every loan or credit card application triggers a hard enquiry on your credit report. Each hard enquiry can drop your score by 5–10 points. Multiple applications in a short period make you appear financially desperate to lenders — the opposite of the impression you want when learning how to improve credit score.

Smart practices:

Apply for new credit only when genuinely needed

Space applications at least 3 months apart

Use pre-qualification or eligibility calculators on bank websites — these use soft enquiries that do not affect your score

If you are shopping for a home loan, complete all applications within a 14-day window — most scoring models count multiple mortgage enquiries in this period as a single enquiry

Being selective with applications signals financial discipline to lenders. This habit alone can dramatically help how to improve credit score over 6–12 months.

Tip 6: Build a Healthy Credit Mix

A one-dimensional credit profile — only credit cards, or only one loan — limits how high your score can go. Lenders and credit bureaus reward borrowers who demonstrate they can responsibly manage different types of credit. This diversity is a smart part of how to improve credit score over the long term.

A strong credit mix includes:

One or two credit cards — used regularly and paid in full

At least one secured loan — home loan, car loan, or gold loan

Optionally one unsecured loan — personal or education loan with a clean repayment record

If you are starting from scratch or rebuilding after a low score:

A secured credit card (deposit ₹10,000–₹50,000 as collateral and receive a card with that limit) is the most accessible entry point

A credit builder loan — monthly payments go into an account and get reported to bureaus, building positive history even as you save

These tools exist specifically to help people learn how to improve credit score from zero or from a damaged base. They are particularly effective for young earners or NRIs looking to establish or rebuild their credit profile.

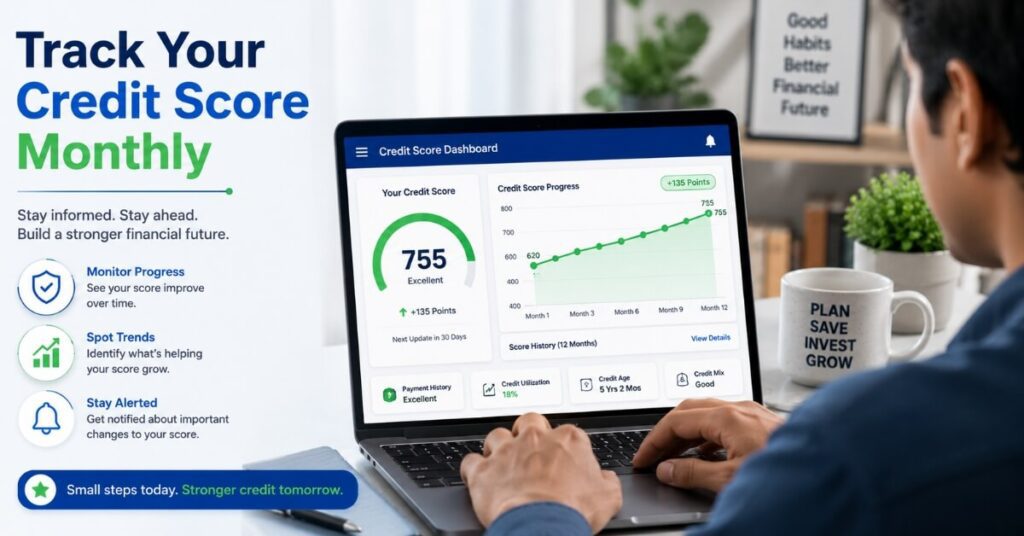

Tip 7: Monitor Your Score Every Month Without Fail

You cannot improve what you do not track. Most people only check their credit score when they need a loan — by which point it is too late to fix problems quickly. Regular monitoring is a non-negotiable habit for anyone who wants to know how to improve credit score and keep it high consistently.

Where to check your credit score in India for free:

cibil.com — official free report once per calendar year

Paisabazaar, BankBazaar, CRED — free monthly score checks with no score impact

Your bank’s mobile app — HDFC, ICICI, Axis, SBI, and most major banks now offer free CIBIL tracking within the app

Important: Checking your own score is a soft enquiry and has zero impact on your score. You can check it as often as you like.

What to review each month:

Overall score — is it trending upward?

Credit utilization percentage

Any new accounts or enquiries you did not initiate (sign of identity fraud)

Payment history status for each account

Any changes after a dispute was raised

Make this a monthly habit — it is a core part of any plan on how to improve credit score sustainably. It keeps you accountable, helps you catch problems early, and keeps you motivated as the number climbs.

How Long Does It Take to See Results?

There are no shortcuts when it comes to how to improve credit score. Anyone promising a 200-point gain in a week is misleading you. Here is a realistic timeline:

Fixing report errors: 30–45 days (after dispute resolution)

Reducing credit utilization: 1–2 billing cycles (30–60 days)

Recovering from a single missed payment: 3–6 months with consistent on-time payments afterward

Moving from 600 to 700: approximately 6–12 months with good habits

Reaching 750 and above: 12–18 months of sustained responsible credit behaviour

But consistent habits compound quickly — and the score you build will last.

Realistic Score Improvement Targets

Score 500–600: Focus on error correction, stop all missed payments, reduce utilization immediately. Timeline: 6–12 months to reach 650+.

Score 600–700: All of the above plus disciplined credit mix building. Timeline: 6–12 months to reach 700+.

Score 700–750: Fine-tune utilization, limit new enquiries, maintain perfect payment history. Timeline: 6–12 months to reach 750+.

Score above 750: Maintain habits, monitor monthly, avoid complacency.

How to Improve Credit Score: Common Mistakes to Avoid

Paying only the minimum due on credit cards — this does not help how to improve credit score and keeps you in a debt cycle

Closing old credit cards — reduces available limit and credit age simultaneously

Applying for multiple loans or cards at once — triggers multiple hard enquiries

Ignoring small outstanding amounts — even ₹500 unpaid can affect your score if reported

Co-signing a loan for someone with poor repayment history — their defaults become your problem

Not checking your credit report annually — errors can accumulate silently and delay how to improve credit score through quick dispute resolution

Tracking Progress Month by Month

Once you start following these seven steps, here is how to know they are working:

Your monthly score check shows an upward trend — even 5–10 points a month is excellent progress

Your credit utilization percentage is dropping

All accounts show “on time” payment status

No unexplained new enquiries appear

Pre-approved loan or credit card offers begin appearing — banks send these when your score improves

If you have ever received an income tax notice due to financial discrepancies — a situation that can add complexity to your overall financial profile — it is important to address those promptly and correctly. Read our detailed guide on How to Respond to Income Tax Notice for a complete step-by-step process.

For checking your official CIBIL score and raising disputes, visit the TransUnion CIBIL official website — it is the most trusted source for your credit report in India.

Frequently Asked Questions

Q1. What is a good credit score in India to get a loan?

Most lenders in India prefer a score of 750 and above. Scores between 700 and 750 may still qualify for standard loans but at slightly higher interest rates. Below 650, loan approvals become difficult.

Q2. How to improve credit score from 600 to 750?

Pay every bill and EMI on time, reduce credit utilization below 30%, fix any errors in your credit report, and avoid new loan applications for 3–6 months. A realistic timeline is 12–18 months.

Q3. Does checking my own CIBIL score affect it?

No. Self-checks are soft enquiries and have zero impact. Only lender-initiated hard enquiries — when you apply for a loan or card — affect your score.

Q4. How long does a missed payment affect credit score?

A missed payment can suppress your score for up to 3 years, though its impact reduces as you build positive history afterward. Consistent on-time payments for 6 months typically start to offset one missed payment.

Q5. Can I learn how to improve credit score without taking a loan?

Yes. A secured credit card used responsibly — small purchases, paid in full every month — builds credit history effectively without needing a loan.

Q6. Does closing a credit card help how to improve credit score?

No — it generally hurts your score by reducing available credit limit and shortening credit history. Only close a card if annual fees are high and the card is not useful.

Q7. What is the fastest way on how to improve credit score in India in 2026?

The two fastest actions are raising a dispute for report errors (can add 30–100 points in 30–45 days) and reducing credit utilization below 30% (visible improvement in 1–2 billing cycles).

Q8. Is it safe to use third-party apps to check CIBIL score?

Yes — established platforms like Paisabazaar, BankBazaar, and CRED use soft enquiries with zero score impact. Always use platforms regulated by RBI-licensed bureaus.

Conclusion

Your CIBIL score is not a verdict — it is a reflection of your habits. Every step you take toward how to improve credit score brings measurable, lasting results. It is not complicated — it just requires consistency. The seven strategies in this guide — paying on time, managing utilization, correcting report errors, keeping old cards, limiting new applications, building a credit mix, and monitoring monthly — are entirely within your control and cost nothing to implement.

Start with one change today. And within 12 to 18 months of consistent effort, you will not just understand how to improve credit score — you will have built the financial credibility to access the best loans, the lowest interest rates, and the financial freedom that a score of 750+ unlocks.

Financial Disclaimer

The information provided in this article is for general educational and informational purposes only and does not constitute professional financial or credit advice. Credit score factors, bureau policies, and lending criteria may vary and change over time. Readers are advised to consult a certified financial advisor before making any credit-related decisions. SK Smart Digital Hub is not responsible for any financial decisions made based on the content of this article.

Pingback: EPFO 3.0 New Features and Benefits: Complete Guide