Retirement is one of the biggest financial milestones in any working person’s life. After decades of hard work, employees receive a bouquet of terminal benefits — gratuity, leave encashment, pension, EPF, NPS, and sometimes VRS compensation. But the big question every retiree asks is: how much retirement benefits tax India rules allow to be kept tax-free, and how much actually goes to the government?

Understanding retirement benefits tax India rules is not just for people who are about to retire. Even if you are 30 or 35 years old and just started your career, knowing these rules helps you plan smarter, choose the right instruments, and avoid nasty tax surprises at the end of your working life.

In this complete guide, we cover every retirement benefit — gratuity, leave encashment, pension, EPF, NPS, commuted pension, and VRS — and explain exactly how retirement benefits tax India laws treat each one for AY 2026-27.

Why Retirement Benefits Tax India Rules Matter in 2026

The retirement benefits tax India framework has seen important updates in recent years. The leave encashment exemption was raised to ₹25 lakh in 2023. NPS withdrawal rules changed in December 2025. The new Income Tax Act 2025 came into effect from April 2026. All these changes make it critical to understand the current retirement benefits tax India position before you file your ITR or plan your retirement corpus.

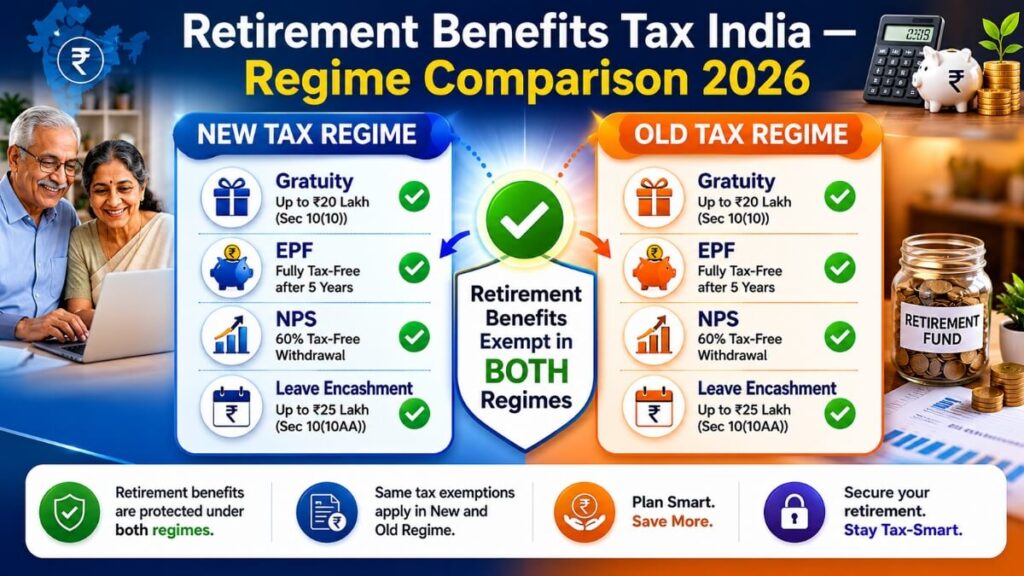

One important thing to know upfront: all major retirement benefit exemptions are available under both the old and new tax regimes. Unlike HRA or LTA which are lost in the new regime, retirement benefits tax India exemptions — gratuity, leave encashment, EPF, NPS — remain fully intact regardless of which regime you choose. We have covered the full regime comparison in our article on which tax regime is better 2026.

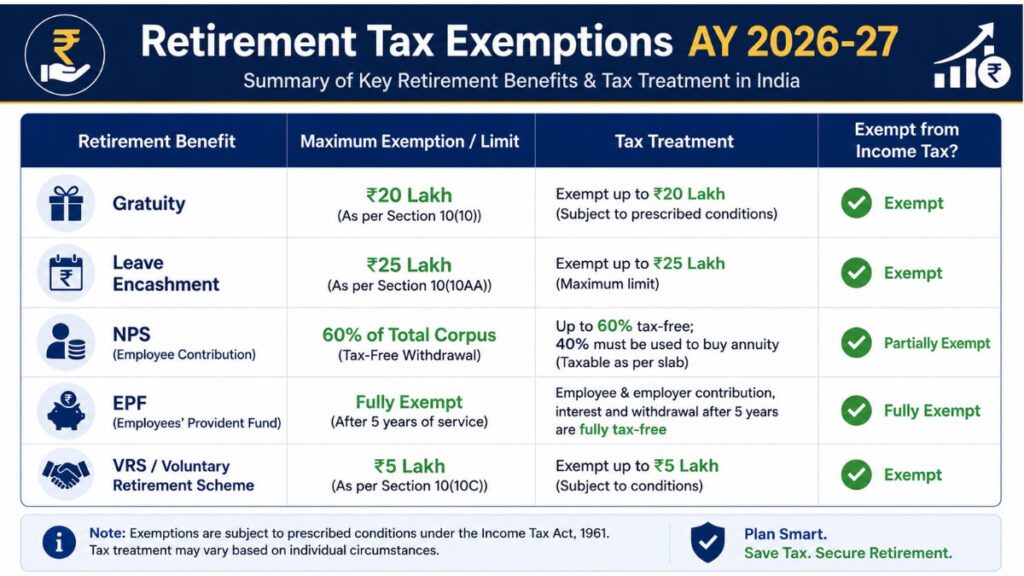

Quick Snapshot — Retirement Benefits Tax India Exemption Table

| Retirement Benefit | Government Employees | Private Employees | Section |

| Gratuity | Fully Exempt | Up to ₹20 lakh | 10(10) |

| Leave Encashment | Fully Exempt | Up to ₹25 lakh | 10(10AA) |

| Commuted Pension | Fully Exempt | 1/3rd or 1/2 exempt | 10(10A) |

| Uncommuted Pension | Taxable as Salary | Taxable as Salary | — |

| EPF Withdrawal | Fully Exempt (5 yrs) | Fully Exempt (5 yrs) | 10(12) |

| NPS Lump Sum (60%) | Tax-Free | Tax-Free | 10(12A) |

| VRS Compensation | Up to ₹5 lakh | Up to ₹5 lakh | 10(10C) |

| Family Pension | — | 1/3rd or ₹25,000 deduction | 57(iia) |

This table gives you the retirement benefits tax India overview at a glance. Now let us go deep into each one.

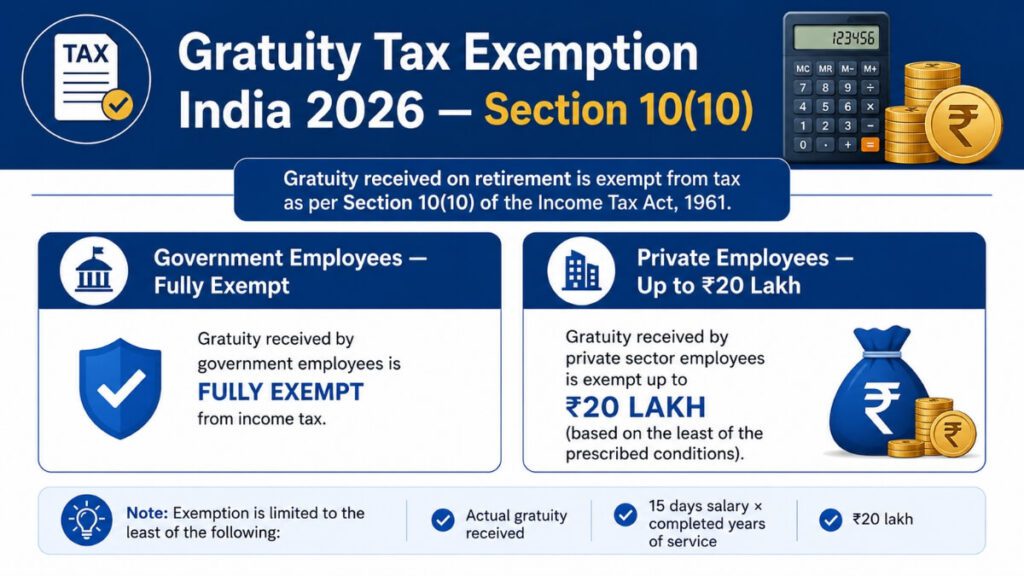

1. Gratuity — Section 10(10)

Gratuity is a lump sum payment made by an employer as a token of gratitude for long service. It is one of the most generous retirement benefits tax India rules offer, especially for government employees.

Eligibility

To receive gratuity, an employee must complete a minimum of 5 years of continuous service. The 5-year rule is waived in case of death or permanent disability.

A. Government Employees

For Central Government, State Government, and local authority employees, gratuity received at retirement is 100% tax-free with no upper limit. This is one of the best retirement benefits tax India provisions for government servants.

B. Private Sector — Covered Under Payment of Gratuity Act 1972

The exemption is the least of the following three:

Actual gratuity received

₹20,00,000 (statutory limit)

15/26 × Last drawn salary (Basic + DA) × Completed years of service

A part-year of more than 6 months is rounded up to one full year.

Example: Ramesh has worked for 22 years. Last drawn basic + DA = ₹60,000/month.

Formula: 15/26 × ₹60,000 × 22 = ₹7,61,538 — fully tax-free.

C. Private Sector — NOT Covered Under Gratuity Act

The exemption is the least of:

Actual gratuity received

₹20,00,000

½ × Average salary of last 10 months × Completed full years of service

Important: The ₹20 lakh limit is a lifetime cumulative limit across all employers — not per employer. If you received ₹8 lakh from one company and now receive ₹15 lakh from another, only ₹12 lakh of the second gratuity is tax-free.

This is a crucial retirement benefits tax India rule many employees miss.

2. Leave Encashment — Section 10(10AA)

Leave encashment is cash paid for unused earned leave at the time of retirement or resignation. The retirement benefits tax India treatment depends on when and why it is received.

Leave Encashment During Service

If you encash leave while still employed — fully taxable as salary. No exemption available.

Leave Encashment at Retirement or Resignation

Government Employees: Entire amount received is fully exempt — no upper limit.

Non-Government Employees: Exempt up to the least of the following:

Actual leave encashment received

₹25,00,000 (raised from ₹3 lakh in April 2023)

10 months’ average salary (Basic + DA)

Cash equivalent of earned leave (leave not exceeding 30 days per year of service)

This ₹25 lakh limit was one of the biggest improvements in retirement benefits tax India rules in recent years. Earlier the limit was just ₹3 lakh — making this an 8x increase in tax protection.

Note: The ₹25 lakh limit is also a lifetime aggregate limit across multiple employers.

3. Pension — Commuted and Uncommuted

Pension is another major retirement benefit, and retirement benefits tax India rules treat commuted and uncommuted pension very differently.

Uncommuted Pension (Monthly Pension)

Monthly pension received regularly is fully taxable as salary income. There is no exemption on regular monthly pension for private sector employees.

For government pensioners receiving pension through banks, standard deduction of ₹75,000 (new regime) or ₹50,000 (old regime) applies just like salary.

Commuted Pension — Section 10(10A)

Commuted pension means a lump sum received in exchange for surrendering a part of your monthly pension.

Government Employees: Commuted pension is fully tax-free — no limit.

Private Sector Employees:

With gratuity: 1/3rd of the full value of commuted pension is exempt

Without gratuity: 1/2 of the full value of commuted pension is exempt

The balance is taxable as salary income.

Family Pension

Family pension received by the spouse or dependants after the death of an employee is taxed under “Income from Other Sources” — not salary.

A standard deduction of 1/3rd of family pension OR ₹25,000 — whichever is lower is available. The balance is added to taxable income.

This is an important retirement benefits tax India rule that many families are unaware of when filing returns after a pensioner’s death.

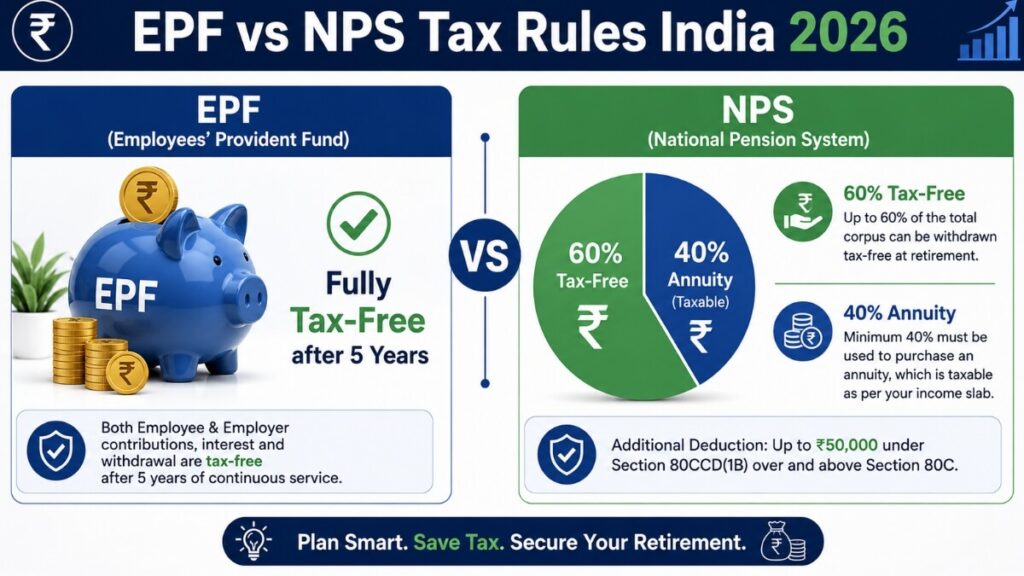

4. Employees’ Provident Fund (EPF) — Section 10(12)

EPF is the most common retirement benefit for private sector employees, and the retirement benefits tax India treatment is one of the most favorable.

EPF withdrawal ya NPS lump sum section ke paas — jaise: “Retirement ke baad apna EPF ya NPS paise receive karne ke liye aaj kal digital payments ka role badh raha hai — samjhiye UPI vs Digital Rupee ka fark.

Tax Treatment of EPF

Withdrawal after 5 years of continuous service: Fully tax-free — no limit on amount.

Premature withdrawal (before 5 years): Taxable. TDS at 10% is deducted (if PAN is provided). If PAN is not provided, TDS is at 34.608%.

EPF Interest

EPF interest is tax-free on employee contributions up to ₹2.5 lakh per year. Interest on contributions above ₹2.5 lakh per year is taxable — this rule has been in effect since FY 2021-22.

Employer’s EPF Contribution

Employer’s contribution up to 12% of salary is exempt. Beyond 12%, it is added to the employee’s taxable income.

The EPF remains one of the true EEE (Exempt-Exempt-Exempt) instruments in the retirement benefits tax India framework — contributions deductible, interest tax-free, and maturity tax-free (after 5 years).

If you are filing your ITR and want to understand how EPF withdrawals are reported, check out our step-by-step guide on ITR filing online kaise kare.

5. National Pension System (NPS) — Section 10(12A)

NPS is a government-backed retirement savings scheme regulated by PFRDA. The retirement benefits tax India rules for NPS are slightly different from EPF — it is EET (Exempt-Exempt-Taxed) in structure, though practically very tax-efficient.

NPS Withdrawal at Retirement (Age 60)

60% of corpus withdrawn as lump sum: Fully tax-free under Section 10(12A)

40% used to purchase annuity: Tax-free at the time of purchase. Annuity income received monthly is taxable as per your slab rate.

December 2025 Rule Change — Important Update

PFRDA changed NPS exit rules in December 2025. Private sector NPS subscribers can now withdraw up to 80% as lump sum (only 20% mandatory annuity). However, the retirement benefits tax India position under the Income Tax Act has not changed — only 60% remains tax-free. The extra 20% lump sum withdrawal is taxable at your applicable slab rate.

Smart Strategy: For retirees with income below ₹12 lakh, the new tax regime’s zero-tax threshold means the taxable 20% may attract little or no tax — making the 80% withdrawal much more practical now.

Partial NPS Withdrawal

Up to 25% of your own contributions to NPS Tier-I can be withdrawn tax-free for specific purposes like medical emergency, children’s education, or house purchase.

Employer’s NPS Contribution

Employer’s contribution to NPS up to 14% of salary is fully exempt under Section 80CCD(2) — available under both old and new tax regimes. This is one of the best tax-saving tools available in the new regime.NPS Trust official portal

6. Voluntary Retirement Scheme (VRS) — Section 10(10C)

VRS compensation is paid by employers to employees who voluntarily retire before the normal retirement age. The retirement benefits tax India rule here is:

Exemption limit: Up to ₹5,00,000 — available only once in a lifetime.

Eligible employers: Public sector companies, other companies, local authorities, co-operative societies, IITs, State Government, Central Government.

Conditions:

Employee must be at least 40 years old, OR have completed 10 years of service

The VRS scheme must be genuine and approved

Any VRS compensation above ₹5 lakh is added to taxable income and taxed at your applicable slab rate.

7. Superannuation Fund

Some employers contribute to an approved superannuation fund on behalf of employees. The retirement benefits tax India treatment:

Employer’s contribution up to ₹1,50,000 per year is tax-free

Above ₹1,50,000 is added to the employee’s taxable income

Lump sum received at retirement from an approved superannuation fund is fully tax-free

Retirement Benefits Tax India — New vs Old Tax Regime

One of the most reassuring retirement benefits tax India facts for 2026 is this: all the major retirement exemptions work under both regimes.

| Benefit | New Regime | Old Regime |

| Gratuity Exemption | ✅ Available | ✅ Available |

| Leave Encashment Exemption | ✅ Available | ✅ Available |

| Commuted Pension Exemption | ✅ Available | ✅ Available |

| EPF Withdrawal (5 yrs) | ✅ Tax-Free | ✅ Tax-Free |

| NPS 60% Lump Sum | ✅ Tax-Free | ✅ Tax-Free |

| VRS ₹5 lakh | ✅ Available | ✅ Available |

| HRA | ❌ Not Available | ✅ Available |

| 80C Deductions | ❌ Not Available | ✅ Available |

This is very different from HRA or 80C deductions which are only available in the old regime. Retirement benefits tax India exemptions are regime-neutral — a huge advantage for retirees choosing the simpler new regime.

How to Report Retirement Benefits in ITR

When you file your ITR, retirement benefits need to be correctly reported:

Gratuity: Exempt portion shown under “Exempt Income” — Schedule EI. Taxable portion (if any) added under “Income from Salaries.”

Leave Encashment: Same as gratuity — exempt part in Schedule EI.

Pension: Monthly pension shown under “Income from Salaries.” Family pension shown under “Income from Other Sources.”

EPF: Tax-free withdrawal does not need to be reported as income. Premature taxable withdrawals are reported under “Income from Salaries.”

NPS: 60% tax-free withdrawal goes to Schedule EI. Taxable portion (if any beyond 60%) is added to income.

Incorrect reporting of retirement benefits tax India exemptions is one of the most common reasons for income tax notices. File carefully or consult a CA if your retirement corpus is large.

Common Mistakes to Avoid

1. Forgetting the lifetime limit on gratuity: The ₹20 lakh exemption is across all employers — not per job.

2. Assuming all NPS withdrawal is tax-free: Only 60% lump sum is tax-free. Annuity income is fully taxable.

3. Treating monthly pension as tax-free: Uncommuted pension is fully taxable — many retirees miss this.

4. Not reporting family pension correctly: It goes under “Income from Other Sources” — not salary.

5. Premature EPF withdrawal without PAN: Attracts 34.6% TDS — a costly mistake.

6. Missing the ₹25 lakh leave encashment limit: Many private sector employees still think the limit is ₹3 lakh — it was updated to ₹25 lakh in 2023.

Retirement Benefits Tax India — Real Example

Situation: Suresh, 60 years old, retires from a private company after 30 years of service.

| Benefit Received | Amount | Tax Status |

| Gratuity | ₹18,00,000 | Fully Exempt (below ₹20L) |

| Leave Encashment | ₹12,00,000 | Fully Exempt (below ₹25L) |

| Commuted Pension (1/3rd) | ₹6,00,000 | ₹2,00,000 exempt (1/3rd) |

| EPF Withdrawal | ₹35,00,000 | Fully Exempt (5+ years) |

| NPS Lump Sum (60%) | ₹24,00,000 | Fully Exempt |

| Total Tax-Free | ₹91,00,000+ |

With proper retirement benefits tax India planning, Suresh keeps over ₹91 lakh completely tax-free. This is why understanding these rules early and investing in the right instruments matters.

FAQs — Retirement Benefits Tax India

Q1. Is gratuity fully tax-free in India?

For government employees — yes, fully tax-free with no limit. For private sector employees, up to ₹20 lakh is exempt under Section 10(10).

Q2. What is the leave encashment tax exemption limit in 2026?

For non-government employees, the limit is ₹25 lakh (raised from ₹3 lakh in April 2023). Government employees get full exemption with no cap.

Q3. Is EPF withdrawal taxable?

No, if you have completed 5 years of continuous service. Premature withdrawal before 5 years is taxable and attracts TDS.

Q4. How much NPS is tax-free at retirement?

60% of your NPS corpus withdrawn as lump sum is fully tax-free under Section 10(12A). The remaining 40% used for annuity purchase is tax-free at purchase but annuity income is taxable.

Q5. Is monthly pension taxable in India?

Yes. Uncommuted (monthly) pension is fully taxable as salary income. Only commuted (lump sum) pension gets partial or full exemption.

Q6. Are retirement benefit exemptions available in new tax regime?

Yes. All major retirement benefits tax India exemptions — gratuity, leave encashment, EPF, NPS — are available under both old and new tax regimes.

Q7. What is VRS exemption limit?

Up to ₹5 lakh is exempt under Section 10(10C). This is a one-time lifetime exemption.

Q8. Is family pension taxable?

Yes, but with a deduction of 1/3rd of family pension or ₹25,000 — whichever is lower. The balance is taxable under “Income from Other Sources.”

Conclusion

Understanding retirement benefits tax India rules is one of the smartest financial moves you can make — whether you are 35 and planning ahead, or 58 and retiring next year. The Indian tax system offers generous exemptions on gratuity, leave encashment, EPF, NPS, and commuted pension. With smart planning, a large portion of your retirement corpus can remain completely tax-free.

The key takeaways from the retirement benefits tax India framework for AY 2026-27: gratuity up to ₹20 lakh is tax-free for private sector, leave encashment up to ₹25 lakh is exempt, EPF after 5 years is fully tax-free, NPS gives 60% tax-free lump sum, and best of all — these exemptions work under both old and new tax regimes.

Start planning today. The decisions you make during your working years — EPF contributions, NPS enrollment, gratuity tenure — directly determine how much of your retirement money stays with you.

Disclaimer:

This article is for informational and educational purposes only. Tax laws are subject to change. Please consult a qualified Chartered Accountant or tax advisor for advice specific to your situation.

Pingback: Debt Snowball vs Avalanche: Best Strategy to Crush Debt 2026