When it comes to funding higher education, most Indian families face a tough financial decision. Should you apply for an education loan vs personal loan in India? Both options can help cover tuition fees, living expenses, and other academic costs — but they work very differently. Choosing the wrong one could cost you lakhs of rupees in extra interest or put unnecessary financial burden on your family.

In this complete guide, we will break down every important difference between education loan vs personal loan in India — including interest rates, tax benefits, eligibility, repayment terms, and real-life scenarios — so you can make the smartest financial decision for your education journey.

Many students researching education loan vs personal loan in India often overlook the long-term cost difference between the two options.Choosing between education loan vs personal loan in India is not just a financial decision — it is a life decision. The loan you pick today will determine your monthly cash flow for the next 5 to 15 years.

That is why it is important to understand every aspect of both options before signing any loan agreement.This guide covers everything you need to know about education loan vs personal loan in India.

What Is an Education Loan?

An education loan, also called a student loan, is a specialized financial product designed specifically to fund higher education expenses. Banks and financial institutions in India offer education loans to help students pursue undergraduate, postgraduate, or professional courses — both in India and abroad.

Education loans in India are classified under Priority Sector Lending by the Reserve Bank of India (RBI), which is why banks offer them at relatively lower interest rates compared to other loan types.

What Does an Education Loan Cover?

Tuition fees and college admission charges

Hostel or accommodation expenses

Cost of books, study materials, and laptop

Examination and library fees

Travel expenses for students studying abroad

Health insurance (in some cases)

Key Features of Education Loans in India

Interest rates: Typically range between 8.5% to 11.5% per annum at public sector banks

Repayment: Starts after course completion — known as the moratorium period

Collateral: May be required for loans above ₹7.5 lakh

Co-applicant: Usually a parent or guardian

Tax benefit: Interest deduction under Section 80E of the Income Tax Act

Government schemes: PM Vidyalaxmi Scheme, Central Sector Interest Subsidy Scheme

What Is a Personal Loan for Education?

A personal loan is a general-purpose, unsecured loan that can be used for any financial need — including education. Unlike education loans, there are no restrictions on how the funds are used. This makes personal loans a flexible option when students need quick funding or when their course is not covered under standard education loan criteria.

However, this flexibility comes at a cost — personal loans typically carry higher interest rates and shorter repayment tenures compared to education loans.

Key Features of Personal Loans in India

Interest rates: Typically range between 10.5% to 24% per annum depending on credit profile

Repayment: Starts immediately after disbursement — no moratorium period

Collateral: Not required (unsecured loan)

Co-applicant: Not mandatory

Tax benefit: No tax deduction available

Approval: Faster processing, often within 24–48 hours

Education Loan vs Personal Loan in India: Key Differences

The table below gives a complete picture of education loan vs personal loan in India at a glance.

| Feature | Education Loan | Personal Loan |

| Purpose | Strictly for education | Any purpose including education |

| Interest Rate | 8.5% – 11.5% | 10.5% – 24% |

| Repayment Start | After course + 6–12 months | Immediately after disbursement |

| Moratorium Period | Yes (course duration + 1 year) | No |

| Collateral Required | Above ₹7.5 lakh | Not required |

| Tax Benefit | Yes — Section 80E | No |

| Loan Amount | Up to ₹1.5 crore (abroad) | Usually up to ₹40–50 lakh |

| Repayment Tenure | Up to 15 years | 1 to 7 years |

| Processing Time | Slower (7–15 days) | Faster (1–3 days) |

| Co-applicant | Required | Not required |

Interest Rate Comparison: Education Loan vs Personal Loan in India

Interest rate is one of the most critical factors when comparing education loan vs personal loan in India. Even a 2–3% difference in interest rate can translate into lakhs of rupees over the loan tenure.

Before finalizing any bank, always calculate the total repayment amount when comparing education loan vs personal loan in India.

Education Loan Interest Rates (2025)

SBI Student Loan Scheme: 8.15% – 10.15% per annum

You can check the latest education loan interest rates and schemes directly on the SBI Education Loan Official Page

Bank of Baroda Education Loan: 8.85% – 10.85% per annum

HDFC Credila Education Loan: 9.5% – 13% per annum

PM Vidyalaxmi Scheme (PMVL-Utkarsh): 7.15% per annum

Personal Loan Interest Rates (2025)

SBI Personal Loan: 11.45% – 14.60% per annum

HDFC Bank Personal Loan: 10.85% – 24% per annum

Bajaj Finserv Personal Loan: 12% – 26% per annum

Airtel Finance Personal Loan: Starting from 12.75% per annum

Real EMI Comparison Example

Let us compare an education loan vs personal loan in India for the same loan amount of ₹10 lakh:

The numbers speak for themselves when you compare education loan vs personal loan in India side by side. A difference of just 6% in interest rate can result in paying over ₹1.5 lakh extra on a ₹10 lakh loan. Smart borrowers always run an EMI calculation before choosing between the two

options.Education Loan:

Amount: ₹10,00,000

Interest Rate: 9% per annum

Tenure: 10 years

Monthly EMI: ₹10,663 (after moratorium)

Total Interest Paid: ₹2,79,560

Personal Loan:

Amount: ₹10,00,000

Interest Rate: 15% per annum

Tenure: 5 years

Monthly EMI: ₹23,790

Total Interest Paid: ₹4,27,400

Difference: ₹1,47,840 more with a personal loan — just for the same ₹10 lakh.

This real-world comparison clearly shows why choosing education loan vs personal loan in India wisely matters so much for your financial future.

Tax Benefits: A Major Advantage of Education Loans

Tax benefit is one area where education loan vs personal loan in India differ the most significantly.

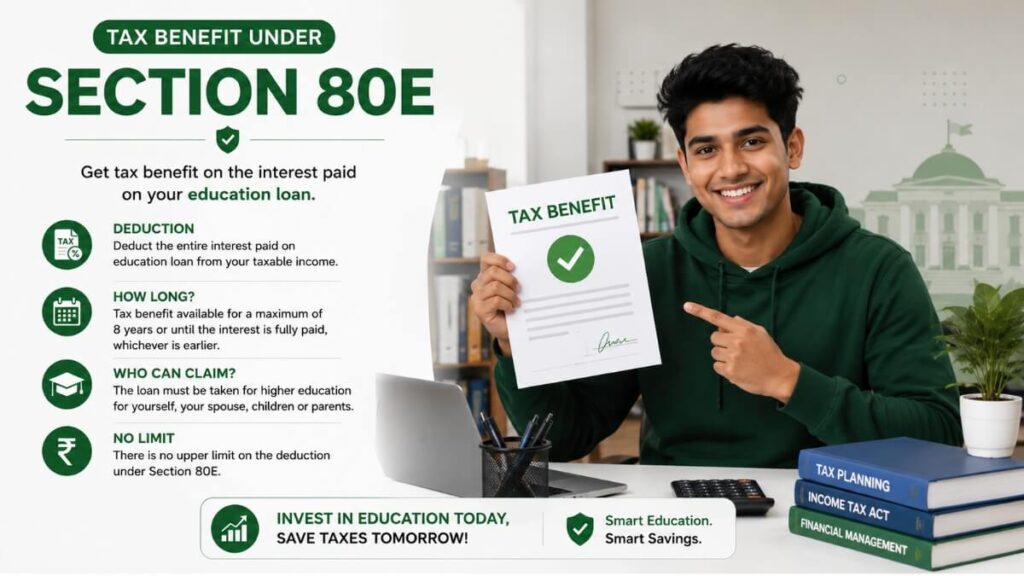

One of the biggest advantages of choosing an education loan over a personal loan in India is the tax benefit under Section 80E of the Income Tax Act.

Section 80E Tax Deduction

Available on the interest paid on education loans

No upper limit on the deduction amount

Available for 8 consecutive years starting from the year repayment begins

Applicable for loans taken for self, spouse, children, or a student for whom you are a legal guardian

Available to individual taxpayers only

Example: If you paid ₹1.2 lakh as interest on your education loan in a financial year, you can claim the full ₹1.2 lakh as deduction from your taxable income.

Personal loans offer zero tax benefit — making education loans significantly more cost-effective for higher income brackets.

Government Schemes for Education Loans in India

When comparing education loan vs personal loan in India, another major advantage is the government support behind education loans.

Most students are unaware that the government actively supports education financing in India. When you compare education loan vs personal loan in India, the government schemes available exclusively for education loans can save you lakhs in interest — something no personal loan can offer. Always check your eligibility for these schemes before making a final decision.

PM Vidyalaxmi Scheme (2024)

Launched by the Government of India to make education loans more accessible:

Collateral-free and guarantor-free loans for students enrolled in Quality Higher Education Institutions (QHEIs)

Interest subvention of 3% on loans up to ₹10 lakh during the moratorium period

Credit guarantee of 75% on loans up to ₹7.5 lakh under CGFSEL

Maximum repayment tenure of 15 years

Central Sector Interest Subsidy Scheme (CSIS)

Full interest subsidy during moratorium for students from economically weaker sections (annual family income up to ₹4.5 lakh)

Available on loans from scheduled banks under the IBA model

Personal loans have no government schemes or subsidies attached to them.

Eligibility Criteria Comparison

Education Loan Eligibility in India

Indian citizen

Secured admission to a recognized institution in India or abroad

Age: Usually 18 to 35 years

Co-applicant (parent/guardian) required

Academic performance may be considered

Collateral required for loans above ₹7.5 lakh

Understanding eligibility criteria is a crucial step when evaluating education loan vs personal loan in India for the first time.

Personal Loan Eligibility in India

Indian citizen

Age: 21 to 60 years

Minimum monthly income: ₹15,000 – ₹25,000 (varies by lender)

Good credit score (usually 700+)

Stable employment or business income

No collateral required

Key insight: Students without income cannot directly qualify for personal loans — they need a co-applicant or guarantor with sufficient income. Education loans are specifically designed for students and are more accessible.

When Should You Choose an Education Loan?

Choosing an education loan vs personal loan in India makes more sense in these situations:

1 .Large loan amounts needed — Tuition fees above ₹5 lakh for domestic or ₹15 lakh for abroad studies

2 .You want lower interest rates — Save lakhs over the loan tenure

3 .Tax benefit is important — You or your co-applicant is in a higher tax bracket

4 .You need repayment flexibility — Moratorium period helps you focus on studies first

5.Government scheme eligibility — PM Vidyalaxmi or CSIS can make education loans almost free for eligible students

6 .Long repayment tenure preferred — Up to 15 years gives breathing room after graduation

When Should You Choose a Education. Lone vs Personal Loan in india ?

There are specific situations where a personal loan may be the better choice over an education loan in India:

1 .Short-term courses or certifications — For skill development courses, coding bootcamps, or professional certifications not covered by standard education loans

2 .Urgent funding needed -Personal loans disburse in 1–3 days vs 7–15 days for education loans

3 .Small loan amounts — For amounts below ₹2–3 lakh, a personal loan may be faster and easier

4 .No co-applicant available — If you have income and a good credit score, personal loans don’t need a co-applicant

5 .Covering miscellaneous expenses — For expenses not covered under education loans like laptops, travel, or exam coaching fees

6 .Rejected education loan application — If your chosen course or institution is not approved for education loans

Impact on Credit Score

Both education loan vs personal loan in India impact your credit score — but differently.

Your repayment behavior on any loan affects your CIBIL score — this applies equally when you choose education loan vs personal loan in India.

Education Loan:

Moratorium period means no EMI payment initially

Credit history building starts only after repayment begins

Long tenure means a longer positive credit history if repaid on time

Personal Loan:

EMI starts immediately — credit history building begins right away

Missed EMIs can severely damage credit score

Shorter tenure means faster credit history completion

For students with no existing credit history, timely repayment of either loan type can be an excellent way to build a strong CIBIL score.

Can You Take Both Loans Together?

Yes — many students combine both options strategically. A common approach is:

Education loan for main tuition and hostel fees (large amount, low interest)

Personal loan for supplementary expenses like laptop, exam fees, or travel (small amount, quick disbursal)

This hybrid approach helps maximize the benefits of both loan types while managing costs efficiently.

Common Mistakes to Avoid

When deciding between education loan vs personal loan in India, avoid these common mistakes:

1 .Not comparing interest rates across multiple banks before applying

2 .Ignoring the moratorium period benefit — many students don’t realize they don’t have to pay during studies

3 .Overlooking Section 80E tax benefit — this can save thousands every year

4 .Not checking government scheme eligibility before applying

5 .Choosing a personal loan for large amounts — the interest difference becomes massive over long tenures

6 .Not reading the fine print on processing fees, prepayment charges, and foreclosure terms

One of the biggest mistakes borrowers make is not researching education loan vs personal loan in

Financial planning starts with the right borrowing decision. Students who take time to properly research education loan vs personal loan in India before applying are always in a better position — both during their studies and after graduation when repayment beginsIndia thoroughly before submitting their application.

Education Loan vs Personal Loan in India: Which Is Better?

After analyzing all factors, here is the final verdict on education loan vs personal loan in India:

Choose an Education Loan if:

Your loan requirement is above ₹3 lakh

You are pursuing a recognized degree or diploma course

You want to benefit from Section 80E tax deduction

You need a long repayment tenure

You qualify for government subsidies

Choose a Personal Loan if:

You need quick disbursement within 24–48 hours

Your course is not eligible for education loans

The loan amount is small (below ₹2–3 lakh)

You have a stable income and good credit score

You want to avoid the paperwork involved in education loans

For the majority of Indian students pursuing higher education — whether in India or abroad — an education loan is the smarter, more cost-effective choice. The lower interest rates, tax benefits, moratorium period, and government schemes make education loans far superior to personal loans for large education funding needs.

However, personal loans remain a useful supplementary tool for quick, small-amount requirements that fall outside the scope of standard education loans.

Here are the most commonly asked questions about education loan vs personal loan in India that students search for online.

Frequently Asked Questions (FAQs)

1. Which is better — education loan vs personal loan in India for higher studies?

Financial experts consistently recommend evaluating education loan vs personal loan in India based on three key factors — loan amount, repayment capacity, and course eligibility. If your course qualifies for an education loan, there is almost no scenario where a personal loan becomes the smarter choice for large funding requirements.

For most students, an education loan is the better choice. It offers lower interest rates (8.5%–11.5%), a moratorium period during studies, Section 80E tax benefit, and government subsidies. A personal loan makes sense only for small amounts, urgent needs, or courses not covered under education loan schemes.

2. Can I get a personal loan for education without a job?

It is difficult to get a personal loan without income or employment. Lenders require a minimum monthly income and a good credit score. However, if a parent or co-applicant with stable income applies, some lenders may approve the loan.

3. Is there any tax benefit on personal loans taken for education?

No. Personal loans do not qualify for any tax deduction, even if the funds are used for education. Only interest paid on a formal education loan qualifies for deduction under Section 80E of the Income Tax Act.

4. What is the maximum amount I can get under an education loan in India?

For studies within India, most banks offer up to ₹10–20 lakh without collateral under government schemes. For studies abroad, the loan amount can go up to ₹1 crore or more depending on the bank and collateral provided.

5. Can I take both an education loan and a personal loan at the same time?

Yes, you can take both loans simultaneously. Many students use an education loan for main tuition fees and a personal loan for additional expenses like laptop, coaching, or travel. However, make sure your repayment capacity covers both EMIs comfortably.

6. How long does it take to get an education loan approved in India?

Education loan approval typically takes 7 to 15 working days, depending on the bank and the documents submitted. Personal loans are faster — they can be approved and disbursed within 24 to 48 hours.

7. What happens if I cannot repay my education loan after graduation?

If you are unable to repay, you should immediately contact your bank and request a restructuring or extension. Banks are generally flexible with education loan borrowers. However, defaulting will severely damage your credit score and may also affect your co-applicant’s credit profile.

8. Is collateral mandatory for education loans in India?

Collateral is not required for education loans up to ₹7.5 lakh under most schemes. For amounts above ₹7.5 lakh, banks may ask for property, fixed deposits, or other assets as security. Under the PM Vidyalaxmi Scheme, eligible students can get collateral-free loans for quality institutions.

Students who carefully compare education loan vs personal loan in India before applying are more likely to save money in the long run.

Conclusion

Choosing between education loan vs personal loan in India is a decision that can impact your financial life for years to come. Both loan types serve different purposes and come with their own set of advantages and limitations

If you are looking to grow your education fund after graduation, learn about What is SIF in India — SEBI’s New Investment Option

Education loans are purpose-built for students — they offer lower interest rates, a moratorium period, Section 80E tax benefits, and government-backed subsidies that make them the most cost-effective option for funding higher education. For any loan requirement above ₹3 lakh, an education loan is almost always the smarter financial choice.

Personal loans, on the other hand, offer speed and flexibility. They are best suited for small funding gaps, short-term courses, or urgent financial needs where quick disbursal is the priority.

The key is to evaluate your specific situation — your loan amount, course type, repayment capacity, and eligibility for government schemes — before making a final decision. Always compare interest rates across multiple lenders, read the fine print carefully, and choose a loan that aligns with your long-term financial goals.

Investing in your education is one of the best decisions you can make. Make sure you fund it wisely with the right loan product.We hope this complete guide on education loan vs personal loan in India helps you make a confident and informed financial decision.

Disclaimer: Interest rates mentioned in this article are indicative and subject to change. Always check with your bank or financial institution for the latest rates before applying.

Pingback: Best SIP Plan to Invest Now — Top 5 in India 2026