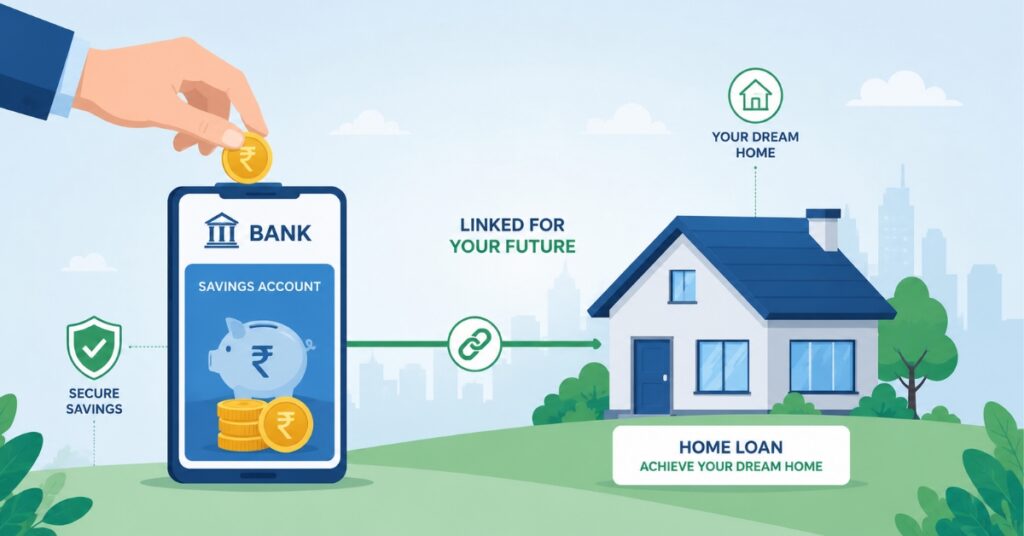

Owning a home is one of life’s biggest milestones, but the home loan that comes with it often stays with borrowers for 15 to 30 years, quietly shaping household budgets throughout this long journey. While prepayments are the most common way to reduce this burden, a growing number of Indian banks are now offering a smarter, more flexible alternative known as the home loan overdraft facility. This facility links your housing loan to a savings or current account, and every rupee parked there works silently to reduce your interest cost, while still remaining fully accessible whenever you need it.

For borrowers who want the best of both worlds, interest savings and liquidity, understanding how this product works can make a real difference to long-term financial planning. Many people spend years repaying EMIs without realising that a small change in structure could save them lakhs of rupees, and this is exactly where the right loan product makes all the difference. In this article, we break down everything about the home loan overdraft facility, including how it works, its benefits, drawbacks, eligibility, real-life examples, tax implications, and which banks in India currently offer it.

What Is a Home Loan Overdraft Facility?

A home loan overdraft facility is a lending arrangement where your home loan account is directly connected to a savings or current account. Instead of simply paying a fixed EMI every month with no additional flexibility, borrowers using this facility can deposit any extra funds, such as an annual bonus, rental income, business profits, or regular savings, into this linked account.

The bank then calculates interest not on the entire sanctioned loan amount, but on the net outstanding balance, which is the total loan amount minus whatever money is currently sitting in the linked account. This single difference is what makes the product so powerful for financially disciplined borrowers.

Unlike a traditional prepayment, where money paid toward the loan is locked away and cannot be retrieved without a fresh loan application, funds parked in this account remain fully liquid. You can withdraw them at any time for emergencies, medical needs, education expenses, or any other purpose, without paperwork or penalties. This is precisely why this facility has become popular among professionals whose income fluctuates seasonally.

How Does a Home Loan Overdraft Facility Work?

The working of this facility becomes clear once you understand its interest calculation method. Banks compute interest daily, based on your net loan balance rather than the original sanctioned amount.

For example, suppose you have a home loan of 40 lakh rupees, and you park 5 lakh rupees in your linked overdraft account. For that period, interest will be calculated only on 35 lakh rupees instead of the full 40 lakh. This directly reduces the total interest payable over the loan tenure, even though your EMI amount usually stays the same.

Consider another scenario. A borrower with a 30 lakh rupee loan receives a yearly bonus of 3 lakh rupees and deposits it into the linked account instead of spending it immediately. Over the following months, interest is calculated on only 27 lakh rupees. If an unexpected expense arises six months later, the borrower can withdraw the full amount without any penalty, having still enjoyed months of reduced interest in the meantime. This flexibility is the core appeal of the home loan overdraft facility for households managing irregular cash flow.

The moment you need funds again, say, for a medical emergency or a large expense, you can simply withdraw the parked money from the linked account. There is no prepayment penalty and no requirement to reapply for a fresh loan, which is what makes this structure fundamentally different from, and often more attractive than, a standard home loan.

Key Features of a Home Loan Overdraft Facility

Interest is calculated on the net outstanding balance, not the full loan amount. Surplus funds remain withdrawable at any time without restrictions. EMI typically remains fixed throughout the tenure. No prepayment charges apply when withdrawing parked funds. Well suited for salaried individuals and business owners with variable income. Loan tenure can effectively shorten without any formal prepayment process. Most banks allow unlimited deposits and withdrawals through net banking, mobile apps, or cheque facilities linked to the account.

These features together make this facility particularly attractive for people who receive irregular income, run a business, or simply want to maintain liquidity while still working to reduce their interest outgo.

Benefits of a Home Loan Overdraft Facility

Interest Savings: Parking surplus money directly reduces the principal amount used for interest calculation. Over a long tenure, this can translate into savings of several lakhs of rupees.

Instant Liquidity: Funds can be withdrawn anytime, unlike a regular prepayment which permanently reduces your outstanding principal without the option of taking that money back.

Flexible Repayment: Borrowers can effectively shorten their loan tenure without going through a formal prepayment process, simply by maintaining a higher balance in the linked account.

No Penalty on Withdrawal: Since the structure functions like an overdraft account, there are no charges for withdrawing money that has already reduced your interest liability.

Useful for Business Owners: Those with fluctuating cash flow can park idle funds temporarily during high revenue periods and withdraw them later when cash flow tightens, all while benefiting from reduced interest during the parked period.

Better Use of Idle Savings: Money that would otherwise sit in a low-interest savings account can instead work harder by lowering your loan’s interest burden, effectively earning a return equal to your home loan interest rate.

Overall, the biggest advantage of choosing this facility is the balance it offers between saving on interest and staying liquid for future needs, something a conventional home loan simply cannot provide.

Drawbacks to Consider Before Choosing This Facility

While beneficial for many borrowers, this facility is not without its limitations. The interest rate offered is usually 0.25 percent to 0.50 percent higher than a standard home loan, since banks are essentially offering additional flexibility in exchange for a small premium.

Borrowers who are not financially disciplined about keeping money parked in the linked account may not see meaningful interest savings at all, since the benefit only materializes when surplus funds are actually maintained. Additionally, not every bank or NBFC offers the home loan overdraft facility, and processing may involve slightly more documentation compared to a standard housing loan application.

It is also worth noting that because the EMI usually stays fixed regardless of how much you park, borrowers need to actively track their loan statement to understand how much interest they are actually saving month to month. Some borrowers also find the linked account structure slightly more complex to manage compared to a straightforward EMI-only home loan, especially if they are not comfortable with active financial tracking.

Home Loan Overdraft Facility vs Regular Home Loan

| Feature | This Facility | Regular Home Loan |

| Interest Calculation | On net balance, loan minus parked funds | On fixed reducing balance |

| Liquidity | High, withdraw parked funds anytime | Low, prepaid amount is not withdrawable |

| Interest Rate | Slightly higher | Usually lower |

| Ideal For | Variable income earners, business owners | Fixed income, disciplined long-term savers |

| Documentation | Slightly more, due to linked account | Standard |

This comparison shows that choosing the home loan overdraft facility suits people who prioritize flexibility and liquidity, while a standard loan may work better for borrowers seeking the lowest possible fixed interest rate with no additional complexity.

Who Should Opt for a Home Loan Overdraft Facility?

This type of loan works particularly well for self-employed professionals, business owners, and salaried individuals who receive periodic bonuses, incentives, or seasonal income. If you often find yourself with surplus cash sitting idle in a regular savings account earning minimal interest, redirecting that money into a linked overdraft account can generate far better returns in the form of interest saved on your home loan.

It may not be the ideal choice, however, for borrowers with a completely fixed monthly income and no significant surplus to park, since the added interest rate premium of the home loan overdraft facility may not be offset by meaningful savings. In such cases, a standard home loan with a lower base interest rate combined with occasional lump-sum prepayments may prove more cost-effective over the long run.

Eligibility Criteria for a Home Loan Overdraft Facility

Most banks require applicants to meet the same basic eligibility conditions as a standard home loan, along with a few additional requirements specific to the overdraft structure. These typically include a stable source of income, a good credit score, a clear property title, and an active operative account with the same bank for linking purposes. Self-employed applicants may also need to submit business financials and income tax returns for the past two to three years to demonstrate income stability.

Since the home loan overdraft facility is offered at the bank’s discretion and often carries a slightly higher interest rate, some lenders also set a minimum loan amount threshold for this product, making it more common among mid to high-value home loans rather than smaller ticket sizes.

Banks Offering Home Loan Overdraft Facility in India

Several major banks in India currently provide this facility, including State Bank of India under its popular SBI Maxgain scheme, ICICI Bank with flexible withdrawal options, Axis Bank with competitive terms for salaried and self-employed borrowers, Kotak Mahindra Bank with digital account management, and Central Bank of India through its Cent Home Double Plus scheme.

Each bank has its own eligibility criteria, interest rate structure, and minimum balance requirements for its version of the home loan overdraft facility, so comparing offers carefully before applying is strongly recommended. It is advisable to check the effective interest rate, minimum average balance requirements, and any annual maintenance charges before finalising a lender.

How to Apply for a Home Loan Overdraft Facility

1 .Check eligibility with your existing bank or a preferred lender offering this product

2 .Compare interest rates for overdraft-linked loans versus standard home loans

3 .Submit income proof, KYC documents, and property papers as required

4 .Get the linked savings or current account activated alongside your loan account

5 .Begin parking surplus funds regularly to start reducing your effective interest burden

Applying for the home loan overdraft facility is broadly similar to applying for a regular home loan, with the added step of linking an operative account specifically for parking surplus funds. Most banks now allow this entire process to be completed digitally, reducing the need for repeated branch visits.

Tips to Maximise Savings With This Facility

To get the most out of this arrangement, try to route your salary or business income directly into the linked account rather than a separate savings account. Avoid withdrawing funds unnecessarily, since even short withdrawals reduce the interest-saving benefit for that period. Periodically review your loan statement to track how much interest you have saved compared to a standard EMI-only structure. Treating the linked account as an extension of your loan repayment strategy, rather than a regular spending account, will help you extract the maximum benefit from the home loan overdraft facility over time.

It is also useful to set up automatic transfers of any surplus salary component at the start of each month, ensuring that funds start reducing your interest liability as early as possible rather than sitting idle until manually deposited.

For borrowers looking to build additional savings that could later be parked in such an account to further reduce interest costs, exploring safer investment instruments is equally important. You can read our detailed guide on the Sovereign Gold Bond 2026 scheme to understand how gold-backed investments can complement your overall financial strategy.

For official guidelines on housing finance and interest computation norms followed by regulated lenders, you may also refer to the Reserve Bank of India website.

Common Mistakes Borrowers Make With This Facility

Even though the concept is simple, many borrowers fail to gain the full benefit due to a few avoidable mistakes. One common error is treating the linked account like a regular savings account and withdrawing funds frequently for everyday expenses, which sharply reduces the interest-saving effect. Another mistake is not comparing the effective interest rate against a standard loan before switching, since the premium charged for this flexibility can sometimes outweigh the benefit for borrowers who rarely maintain a surplus.

Some borrowers also forget to monitor their loan statements regularly, missing out on the chance to track exactly how much interest they have saved over a given period. Others assume that simply opening the linked account is enough, without actually routing salary or business income into it consistently, which defeats the entire purpose of choosing this structure over a conventional loan.

Finally, a number of borrowers overlook the minimum balance or annual maintenance charges that some banks apply to the linked account, which can quietly eat into the savings generated. Reading the fine print carefully and asking the bank for a clear breakdown of charges before signing up can help avoid unpleasant surprises later.

Tax Implications to Keep in Mind

It is worth noting that the tax benefits available under Sections 24(b) and 80C of the Income Tax Act for home loan interest and principal repayment continue to apply in largely the same way, regardless of whether you choose a standard loan or an overdraft-linked structure. However, since the interest payable each month can vary depending on how much surplus is parked, the exact figure eligible for deduction may fluctuate slightly year to year. It is advisable to obtain a proper interest certificate from your bank at the end of each financial year and, where needed, consult a tax professional to ensure accurate claims while filing returns.

Frequently Asked Questions

Q1. What is a home loan overdraft facility?

A home loan overdraft facility is a loan structure where your home loan is linked to a savings or current account, allowing surplus deposits to reduce your interest liability while remaining withdrawable at any time.

Q2. Is a home loan overdraft facility better than a regular home loan?

It depends on your income pattern and financial discipline. This facility suits individuals with variable income and regular surplus savings, while a regular home loan may be better suited to those seeking the lowest fixed interest rate without added complexity.

Q3. Which banks offer a home loan overdraft facility in India?

SBI Maxgain, ICICI Bank, Axis Bank, Kotak Mahindra Bank, and Central Bank of India are among the most popular providers of this product in India.

Q4. Does this facility affect my monthly EMI amount?

No, your EMI usually remains unchanged. However, the effective tenure or total interest paid can reduce significantly depending on how much surplus you consistently maintain in the linked account.

Q5. Are there any charges for withdrawing money from a home loan overdraft facility?

No, withdrawals from the linked account are generally free of prepayment penalties, which is one of the key differences compared to withdrawing a standard home loan prepayment.

Q6. Can self-employed individuals apply for a home loan overdraft facility?

Yes, self-employed professionals and business owners are often ideal candidates, since their income tends to be irregular and they can benefit significantly from parking surplus funds during high-earning periods.

Conclusion

Choosing between a fixed-rate home loan and a flexible overdraft-linked option ultimately depends on your income stability and financial habits. For disciplined savers with regular surplus funds, the home loan overdraft facility can meaningfully reduce interest costs over the loan tenure while still keeping money fully accessible for emergencies. Before making a final decision, it is important to compare interest rates across multiple banks, honestly evaluate your own cash flow pattern, and consult a qualified financial advisor to determine which loan structure best aligns with your long-term financial goals.

Disclaimer

This article is for informational purposes only and does not constitute financial or investment advice. Please consult a certified financial advisor or your bank directly before making any loan-related decisions.

Pingback: Earn Money From Mobile For Students: 20 Easy Ways