Filing your income tax return is one of the most important financial responsibilities of the year. Yet, thousands of Indian taxpayers fall into the same traps year after year. Understanding common ITR filing mistakes can save you from tax notices, penalty charges, and refund delays. Whether you are a salaried employee, a freelancer, or a business owner, avoiding common ITR filing mistakes is essential to stay compliant and financially secure.

In this comprehensive guide, we will walk you through the most critical errors — including ones that most people overlook — and show you exactly how to avoid them this ITR season. Read carefully, because some of these mistakes could cost you lakhs of rupees in penalties and legal trouble.

Why Avoiding These Errors Matters More Than Ever

Every year, the Income Tax Department processes millions of returns. Thanks to advanced data analytics and AI-powered tools, the department can now easily identify discrepancies between what you report and what third-party sources — like banks, employers, and foreign brokerages — report about you.

The common ITR filing mistakes that once went unnoticed are now being flagged in real time. The consequences can be serious: tax notices under Section 139(9) or Section 142(1), withholding of refunds, demand notices, and even penalties under Section 270A for underreporting income. The department’s backend system now automatically cross-checks your return against AIS, Form 26AS, SFT data, and even GST filings.

This is why being careful and thorough during the ITR filing process has never been more important.

Mistake 1: Not Choosing the Right ITR Form

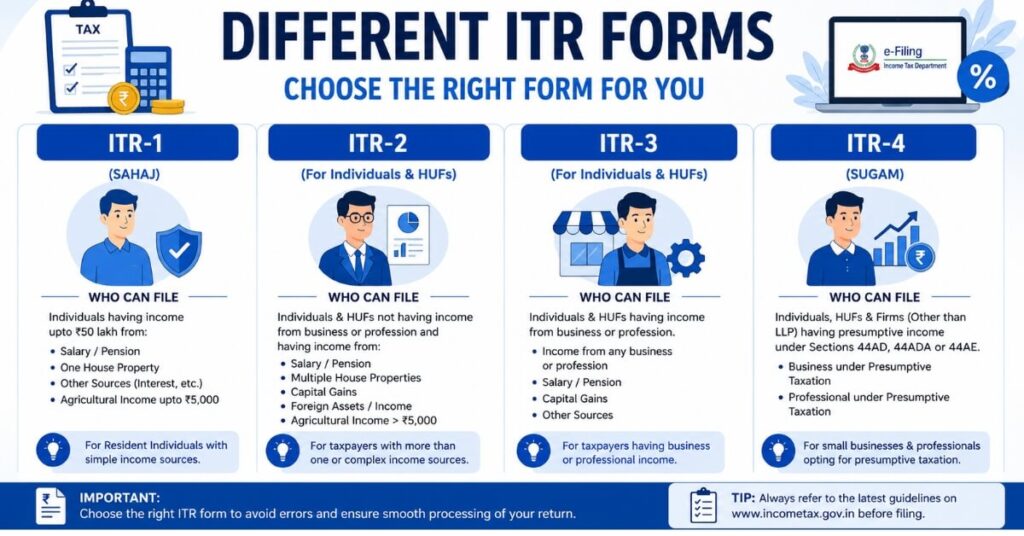

One of the most widespread common ITR filing mistakes is selecting the wrong ITR form. India has multiple ITR forms — ITR-1, ITR-2, ITR-3, ITR-4, and so on — each designed for a specific type of taxpayer.

ITR-1 (Sahaj) is for salaried individuals with income up to ₹50 lakh, one house property, and no capital gains. ITR-2 is for individuals with capital gains, foreign income, or multiple properties. ITR-3 covers those with business or professional income. ITR-4 (Sugam) is for those under the presumptive taxation scheme under Sections 44AD, 44ADA, or 44AE.

Using the wrong form results in a defective return notice under Section 139(9), which gives you only 15 days to correct the error. If you miss that window, your return is treated as not filed at all — a very costly consequence of one of the most avoidable common ITR filing mistakes.

Mistake 2: Failure to Disclose Foreign Assets in Schedule FA

This is perhaps the biggest of all common ITR filing mistakes for the current assessment year 2026-27. With the growing popularity of investing in US stocks, ETFs, and international mutual funds, many Indian residents now hold foreign assets. However, they fail to disclose these in Schedule FA of their return.

Even if you have not sold your foreign stocks or received any dividends, you are still required to declare them under the Foreign Assets schedule. RSUs (Restricted Stock Units) given by multinational employers are held in foreign brokerage accounts and must be disclosed. Employee Stock Options (ESOPs) from foreign parent companies also fall under this requirement.

The Income Tax Department has been sending notices to taxpayers who failed to disclose foreign assets in previous years. Non-disclosure can attract penalties under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, which can be as severe as ₹10 lakh or more per asset.

Always list all your foreign accounts, investments, and assets in Schedule FA, even if they generated zero income during the year. Not doing so is a common ITR filing mistake that can have very serious long-term legal consequences for you and your family.

Mistake 3: Incorrectly Reporting Capital Gains

Incorrectly reporting capital gains is among the most common ITR filing mistakes seen among equity investors and mutual fund holders. With the updated capital gains tax structure applicable from FY 2024-25 onwards, both Short-Term Capital Gains (STCG) and Long-Term Capital Gains (LTCG) must be reported accurately.

Key points to remember: LTCG from equity above ₹1.25 lakh is now taxable at 12.5% without indexation. STCG from equity is taxed at 20%. Debt mutual funds are now taxed as per your income slab with no indexation benefit. Capital losses can be set off and carried forward only if you file your return on time before the due date.

Many taxpayers either ignore capital gains from mutual fund redemptions or enter incorrect holding periods. Both are common ITR filing mistakes that can trigger demand notices. Use your broker’s capital gains statement or the CAMS and KFintech consolidated statement to report mutual fund gains accurately.

Mistake 4: Not Disclosing All Bank Accounts

The Income Tax Department requires you to disclose all savings and current bank accounts held in India during the financial year — even if an account had zero transactions or was dormant throughout the year. Forgetting to list inactive accounts is one of the common ITR filing mistakes that triggers unnecessary scrutiny and defective return notices. This is also among the common ITR filing mistakes that are extremely easy to prevent — just log into each bank’s netbanking portal and note down your account numbers before you start filing.

Your refund can only be credited to one nominated account, but all accounts must be listed in the ITR. Make sure you include all savings accounts, NRE and NRO accounts if applicable, and joint accounts where you are the primary account holder during the financial year.

Mistake 5: Missing Income from a Previous Employer

If you changed jobs during the financial year, you need to consolidate income from all employers. Not showing income from a previous employer is among the common ITR filing mistakes made repeatedly by salaried professionals every year, especially in a job market with frequent career transitions.

Your new employer calculates TDS only on the salary paid by them. If you do not submit your previous Form 16 to your new employer — or if you do not manually combine both employer incomes in your ITR — you end up underreporting your total annual income. This is a serious common ITR filing mistake that can attract a penalty of 50% to 200% of the tax on the underreported amount.

Always collect Form 16 from every employer you worked with during the financial year. Use Form 26AS and AIS to cross-verify your total income before filing.

Mistake 6: Not Reporting Rental Income

Many property owners either forget or skip reporting rental income, making it one of the most recurring common ITR filing mistakes in India. Even if you have a single rented-out property, the rent received must be declared under Income from House Property.

You are eligible for a standard deduction of 30% on net annual value, plus a deduction for municipal taxes paid. You can also claim home loan interest deduction under Section 24(b) up to ₹2 lakh for self-occupied property. However, not disclosing rental income is risky — banks and tenants now report rent payments through SFT (Statement of Financial Transactions), and TDS on rent above ₹50,000 per month is mandatory under Section 194-IB.

Mistake 7: Ignoring Interest Income from FDs and Savings Accounts

Interest income from savings accounts, fixed deposits, recurring deposits, and post office schemes is fully taxable under the head Income from Other Sources. Overlooking it is among the most common ITR filing mistakes, because many taxpayers assume that since TDS has already been deducted by the bank, they do not need to report it separately.

That assumption is incorrect. You must report gross interest income in your return, claim TDS credit in Schedule TDS, and claim deductions under Section 80TTA (up to ₹10,000 for savings account interest) or Section 80TTB (up to ₹50,000 for senior citizens on all interest income). Your bank reports interest details to the IT Department through SFT, so any mismatch gets flagged automatically in your AIS within days.

Mistake 8: Claiming Deductions Without Proper Documentation

Claiming deductions without maintaining supporting documents is one of the most dangerous common ITR filing mistakes you can make. In the past, many taxpayers claimed HRA, LTA, health insurance premiums, and home loan repayments without any proper proof and got away with it without scrutiny.

That era is completely over. The department now uses data matching technology that cross-verifies your claims with insurer databases, employer records, bank statements, and even housing society records. Always maintain rent receipts and rental agreements for HRA claims, insurance premium payment receipts for Section 80C and 80D, home loan repayment certificates from your lender for Section 24 and 80EEA, and donation receipts with 80G certificates for charitable contributions.

If you have already received a notice because of documentation errors, read our detailed guide on how to handle it: How to Respond to an Income Tax Notice

Mistake 9: Relying Blindly on AI Tools to File Returns

AI-powered apps and tools have made return filing more accessible, but blindly relying on them without manual verification is an emerging common ITR filing mistake. These tools can assist with basic income calculations and form filling, but they cannot handle the complexity of foreign asset disclosure, capital gains from multiple instruments, or consolidated income from multiple employers with full accuracy.

The Income Tax Department’s official e-filing portal at incometax.gov.in pre-fills your AIS and Form 26AS data and is a safer, faster option for straightforward returns. Always verify the pre-filled data before accepting it — errors in pre-filled data do occur and you remain responsible for the final accuracy of your submitted return. For complex situations, a qualified Chartered Accountant remains the best and most reliable choice.

Mistake 10: Not Consulting a Tax Professional for Complex Returns

Not seeking professional guidance when your finances are complex is one of the costliest common ITR filing mistakes a taxpayer can make. If you have multiple income sources, foreign assets or RSUs, business or freelance income, capital gains from equity, mutual funds, or property, or a large refund to claim — filing without expert help significantly increases your risk of errors and notices.

A Chartered Accountant fee typically ranges from ₹1,500 to ₹5,000 for most individual taxpayers. Compare that to a penalty of ₹50,000 or more for underreporting, and professional guidance becomes a very sensible and cost-effective investment.

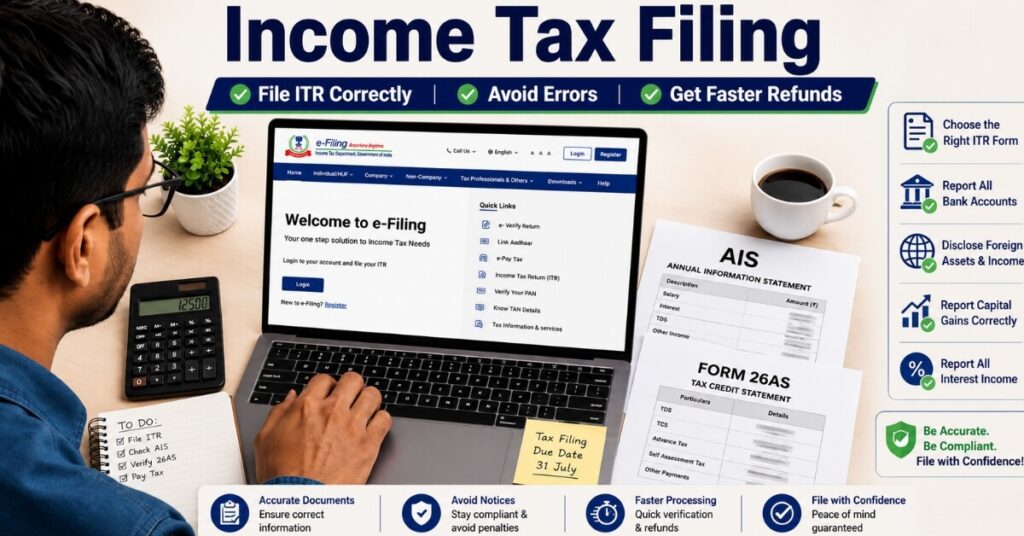

How AIS and Form 26AS Help You File Accurately

The Annual Information Statement (AIS) is the most comprehensive financial document available to Indian taxpayers today. It shows all your financial transactions — from stock market trades to foreign remittances to mutual fund redemptions and interest income credited by your bank. Cross-referencing your AIS with your return is the single best way to catch common ITR filing mistakes before the IT Department does.

Form 26AS shows all TDS and TCS deducted on your behalf by various deductors throughout the year. Any mismatch between your ITR and Form 26AS is a red flag that the automated system catches immediately during processing. Always download both AIS and Form 26AS from the Income Tax e-filing portal before even starting your draft return.

According to the Income Tax Department of India, taxpayers must verify their AIS carefully and report any inaccuracies before filing. For the latest official guidance, updated forms, and filing deadlines, visit the Income Tax e-Filing Portal

Quick Checklist to Eliminate All Errors Before Submitting

Before clicking the final submit button, go through this checklist to eliminate common ITR filing mistakes:

Select the correct ITR form based on your income type and all income sources. Cross-check Form 26AS, AIS, and TIS with your actual income from every source. Disclose all bank accounts including inactive accounts and zero-balance accounts. Report income from all employers during the year and collect all Form 16 documents.

Declare all foreign assets in Schedule FA even if no income was earned on them. Report capital gains from equity, mutual funds, and property accurately with correct dates. Include interest income from all fixed deposits, savings accounts, and post office schemes. Maintain and safely store all documents for every deduction you plan to claim. Verify and correct all pre-filled data before clicking submit. E-verify your return within 30 days of filing to complete the entire process legally.

Following this checklist every year will help you avoid the most costly common ITR filing mistakes before they turn into notices or penalties.

Frequently Asked Questions (FAQs)

Q1: What are the most common ITR filing mistakes made by salaried employees?

The most common ITR filing mistakes for salaried employees include not disclosing income from previous employers, ignoring fixed deposit interest income, incorrectly claiming HRA without proper rent receipts, and not listing all bank accounts. Always collect all Form 16 documents and cross-check with your AIS before filing your return.

Q2: Can common ITR filing mistakes lead to a tax notice?

Yes, absolutely. Common ITR filing mistakes such as not disclosing foreign assets, underreporting income from any source, or claiming deductions without supporting documents can trigger notices under Section 139(9), Section 142(1), or Section 148. Some mistakes also attract penalties of up to 200% of the tax amount under Section 270A for deliberate misreporting.

Q3: How many times can I revise my ITR after realizing I made errors?

If you identify common ITR filing mistakes after submitting your return, you can file a revised return under Section 139(5). You can revise your return multiple times before December 31 of the relevant assessment year or before the completion of the assessment, whichever comes earlier.

Q4: Is it mandatory to disclose foreign investments even if I earned no income from them?

Yes, it is mandatory. Failure to disclose foreign assets is one of the most serious common ITR filing mistakes under Indian tax law. Even unsold stocks held in foreign brokerage accounts must be declared in Schedule FA, regardless of whether they generated any income during the financial year.

Q5: How can I verify that I have not made any errors before submitting my return?

Download your AIS and Form 26AS from the Income Tax e-filing portal and compare every entry with your draft ITR. This comparison is the most reliable and practical method to catch common ITR filing mistakes before the department flags them during automated processing.

Conclusion

ITR filing season brings both opportunity and risk for every Indian taxpayer. The opportunity is to claim every deduction you legitimately deserve and potentially receive a refund from the government. The risk lies in the common ITR filing mistakes that can undo all your financial planning with a single tax notice, penalty demand, or refund hold.

From not disclosing foreign assets and capital gains reporting errors to relying on AI tools without verification and missing income from previous employers, there are many ways taxpayers go wrong during the filing process. But with the right checklist, proper documentation, and professional help when needed, you can file a clean, accurate, and complete return every single year.

Start your preparation early, download your AIS and Form 26AS today, gather all your documents, and if your financial situation is even slightly complex, invest in professional guidance. Avoid common ITR filing mistakes this season and file your return with complete confidence.

Financial Disclaimer

The information provided in this article is for educational and informational purposes only. It does not constitute professional tax, legal, or financial advice. Tax laws and regulations in India are subject to frequent change. Please consult a qualified Chartered Accountant or registered tax professional for personalized advice specific to your individual financial situation before making any tax-filing or financial decisions.

Pingback: SBI FD for Senior Citizens — Ultimate 7.05% Interest Guide