Every salaried employee in India is asking the same question right now: which tax regime is better 2026? With the new Income Tax Act 2025 coming into effect from April 2026, and ITR filing season just around the corner, this decision has never been more important.

In this complete guide, we break down both regimes — new and old — with real salary examples, updated tax slabs, and a clear comparison so you can decide with confidence.

What Is the New Tax Regime?

The most common question during ITR season is which tax regime is better 2026 — and the answer starts with understanding the new regime first.

This means if you do not actively choose the old regime, you are automatically placed in the new one.

The most common question during ITR season is which tax regime is better 2026 — and the answer starts with understanding the new regime first.

Key Features of New Tax Regime 2026:

Default tax regime — no action needed to stay in it

Income up to ₹12 lakh is effectively tax-free (Section 87A rebate)

Standard deduction of ₹75,000 for salaried individuals

Gross salary up to ₹12.75 lakh is effectively tax-free after standard deduction

No deductions under Section 80C, 80D, HRA, LTA

Simpler and faster filing process

What Is the Old Tax Regime?

The old tax regime is the traditional system of income tax in place for decades.Which Tax Regime Is Better 2026 It offers higher tax rates but allows a wide range of deductions and exemptions that reduce your taxable income.

To fully answer which tax regime is better 2026, we need to understand how the old regime works and who it benefits.

Key Features of Old Tax Regime 2026:

Must be actively opted every year

Basic exemption limit: ₹2.5 lakh

Income up to ₹5 lakh is tax-free due to Section 87A rebate

Standard deduction of ₹50,000 for salaried individuals

Allows: Section 80C (up to ₹1.5 lakh), 80D, HRA, LTA, Home Loan Interest (Section 24b)

Better for those who invest heavily and claim multiple deductions

New vs Old Tax Regime 2026 — Tax Slab Comparison

Understanding which tax regime is better 2026 starts with comparing slabs side by side

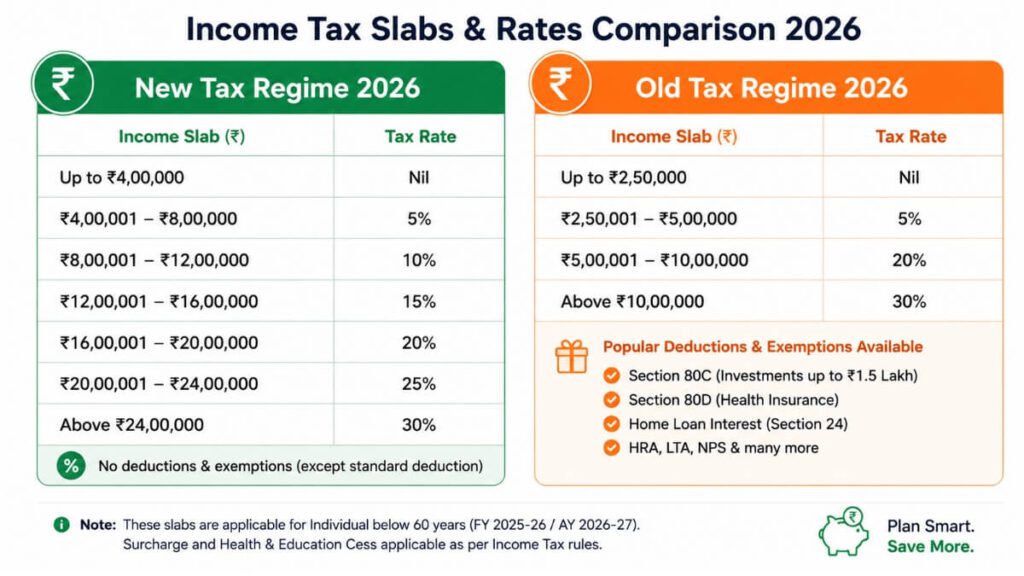

New Tax Regime Slabs (FY 2025-26 / AY 2026-27)

| Income Range | Tax Rate |

| Up to ₹4 lakh | Nil |

| ₹4 lakh – ₹8 lakh | 5% |

| ₹8 lakh – ₹12 lakh | 10% |

| ₹12 lakh – ₹16 lakh | 15% |

| ₹16 lakh – ₹20 lakh | 20% |

| ₹20 lakh – ₹24 lakh | 25% |

| Above ₹24 lakh | 30% |

Note: Income up to ₹12 lakh is effectively tax-free due to Section 87A rebate of ₹60,000.

Old Tax Regime Slabs (FY 2025-26 / AY 2026-27)

| Income Range | Tax Rate |

| Up to ₹2.5 lakh | Nil |

| ₹2.5 lakh – ₹5 lakh | 5% |

| ₹5 lakh – ₹10 lakh | 20% |

| Above ₹10 lakh | 30% |

Note: Income up to ₹5 lakh is tax-free due to Section 87A rebate of ₹12,500.

Key Deductions — What You Can and Cannot Claim

| Deduction | New Regime | Old Regime |

| Standard Deduction | ₹75,000 ✅ | ₹50,000 ✅ |

| Section 80C (PPF, ELSS, LIC) | ❌ | ✅ Up to ₹1.5 lakh |

| Section 80D (Health Insurance) | ❌ | ✅ Up to ₹50,000 |

| HRA | ❌ | ✅ Allowed |

| Home Loan Interest (Sec 24b) | ❌ | ✅ Up to ₹2 lakh |

| LTA | ❌ | ✅ Allowed |

| NPS Employer Contribution (80CCD2) | ✅ | ✅ |

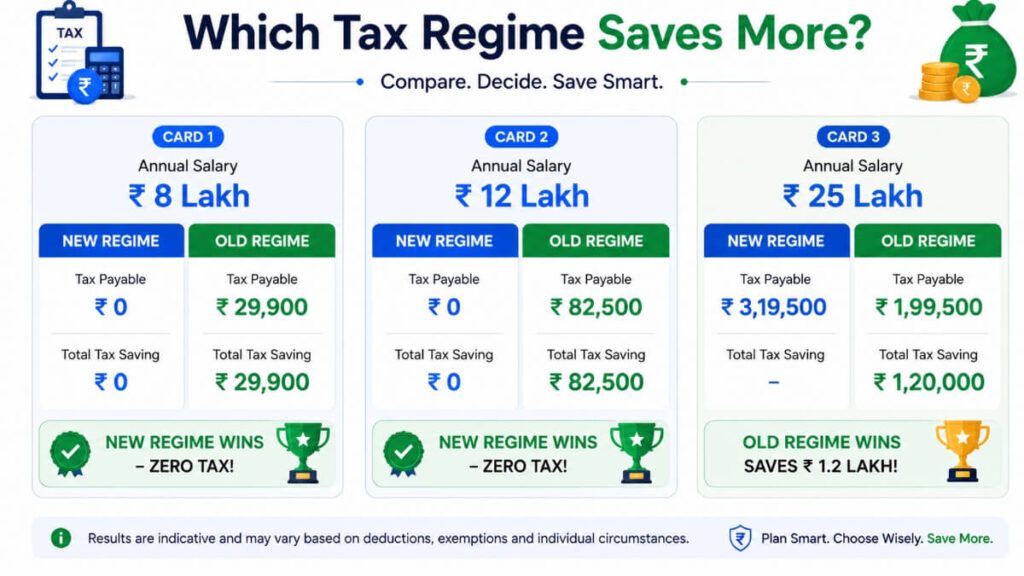

Real Salary Examples — Which Regime Saves More?

Example 1 — Salary ₹8 Lakh (Low Deductions)

New Regime: Taxable income ₹7.25 lakh → Zero tax (Section 87A rebate applies)

Old Regime: Taxable income ₹7.5 lakh → ~₹25,000 tax

New Regime wins

Example 2 — Salary ₹12 Lakh (Moderate Deductions — Rent + 80C + HRA)

Old Regime: After deductions of ₹3.2 lakh → Taxable ₹8.8 lakh → ~₹83,000 tax

New Regime: Taxable ₹11.25 lakh → Zero tax (below ₹12L rebate threshold)

New Regime wins

Example 3 — Salary ₹25 Lakh (Heavy Deductions — Home Loan + 80C + 80D + HRA)

Old Regime: After ₹4.5 lakh deductions → Taxable ₹20.5 lakh → ~₹3,97,500 tax

New Regime: Taxable ₹24.25 lakh → ~₹5,18,750 tax

Old Regime wins — Saves over ₹1.2 lakh

New Tax Regime — Pros and Cons

Pros:

Zero tax up to ₹12.75 lakh for salaried employees

Simpler filing — fewer documents needed

Higher standard deduction of ₹75,000

Great for young earners with no major investments or loans

Cons:

No 80C benefit (PPF, ELSS, LIC)

HRA exemption not available

Home loan interest deduction not allowed

No flexibility for tax planning

Old Tax Regime — Pros and Cons

Pros:

Multiple deductions — 80C, 80D, HRA, LTA, Home Loan

Encourages savings and long-term investment

Better for salary above ₹15 lakh with heavy deductions

Home loan borrowers save up to ₹2 lakh

Cons:

Higher tax rates on middle income slabs

Complex filing — requires proofs and investment declarations

Must actively opt in every year

Lower standard deduction of ₹50,000

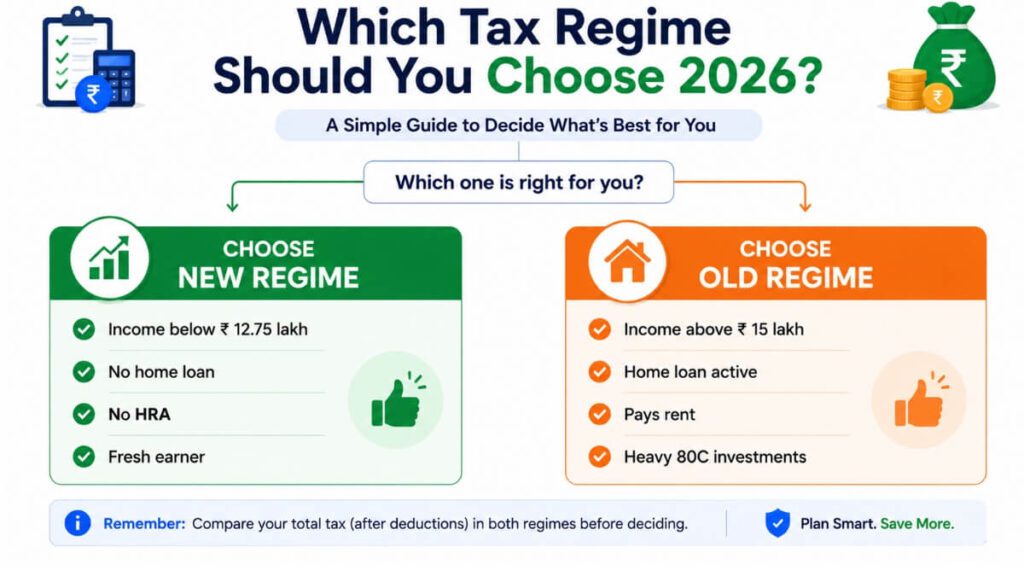

When Should You Choose the New Tax Regime?

Choose the new tax regime in 2026 if:

Your income is below ₹12.75 lakh — you pay zero tax

You are a fresh earner with no HRA, home loan, or heavy investments

Your total deductions under old regime are less than ₹3 lakh

You want simple, hassle-free tax filing

For most young salaried employees, which tax regime is better 2026 is an easy answer — the new regime saves more with zero effort.

When Should You Choose the Old Tax Regime?

The answer to which tax regime is better 2026 is the old regime if:

Your income is above ₹15 lakh

You invest heavily in PPF, ELSS, or LIC (claiming full ₹1.5 lakh under 80C)

You live in a rented house and claim HRA

You have an active home loan and claim interest deduction

Your total deductions exceed ₹4–5 lakh per year

If you are choosing the old tax regime and investing in ELSS under Section 80C, make sure you also explore the best SIP plan for beginners in India to maximise your tax savings and build long-term wealth.

Important Update — New Income Tax Act 2025

The Income Tax Act 2025 has come into effect from April 1, 2026, replacing the Income Tax Act 1961. For ITR filing in 2026, salaried employees should note:

Last date for ITR-1 and ITR-2: July 31, 2026

New simplified ITR forms have been notified

New tax regime remains the default regime

This makes understanding which tax regime is better 2026 even more critical before you file your return.

How to Switch Between Regimes

Salaried employees can switch every year. Here is how:

1 .inform your employer about your preferred regime during investment declaration at the start of the year Which Tax Regime Is Better 2026

2 .Or choose directly in the ITR form before the filing due date

3 .Business owners and professionals can switch only once — limited flexibility

Before you switch, calculate your exact tax using the official income tax calculator on the Government of India website.

Quick Decision Table — Which Tax Regime Is Better 2026?

| Your Situation | Best Choice |

| Income below ₹12.75 lakh | New Regime ✅ |

| No deductions to claim | New Regime ✅ |

| Fresh job, no loans | New Regime ✅ |

| Paying house rent | Old Regime ✅ |

| Home loan active | Old Regime ✅ |

| Investing in 80C heavily | Old Regime ✅ |

| Income above ₹20 lakh with deductions | Old Regime ✅ |

| High income, no deductions | New Regime ✅ |

FAQs — Which Tax Regime Is Better 2026

Q1. Which tax regime is better 2026 for a salary of ₹10 lakh?

The new tax regime is better. After ₹75,000 standard deduction, taxable income is ₹9.25 lakh — below the ₹12 lakh threshold, making tax liability zero.

Q2. Can I switch tax regime every year?

Yes. Salaried employees can switch between new and old tax regime every year — at investment declaration or at ITR filing time.

Q3. Is HRA allowed in new tax regime?

No. HRA exemption is not available in the new tax regime. If you pay rent, the old regime is better for you.

Q4. What is the standard deduction in 2026?

New regime: ₹75,000. Old regime: ₹50,000 for salaried individuals and pensioners.

Q5. Is Section 80C available in new tax regime?

No. PPF, ELSS, LIC and other 80C investments do not give tax benefit under the new regime.

Q6. What is the tax-free income limit in 2026?

New regime: ₹12 lakh (₹12.75 lakh for salaried after standard deduction). Old regime: ₹5 lakh.

Q7. Which tax regime is better 2026 for home loan borrowers?

Old tax regime is better. You can claim up to ₹2 lakh on home loan interest under Section 24b — not allowed in the new regime.

Q8. What if I do not choose any regime?

You will automatically be placed in the new tax regime, as it is the default since FY 2023-24.

Final Verdict — Which Tax Regime Is Better 2026?

New Regime — best for income below ₹12.75 lakh, fresh earners, and those with minimal deductions..

Old Regime — best for income above ₹15–20 lakh with heavy investments, home loan, or HRA.

Before deciding, compare both using the official calculator at incometaxindia.gov.in or ClearTax. A few minutes of comparison can save you thousands of rupees.

So the next time someone asks you which tax regime is better 2026 — you now have all the facts to decide smartly.

Also Read:

What Is SIP and Why Is It the Best Investment Option for Beginners?

50/30/20 Rule Kya Hai — Apni Salary Smart Tarike Se Manage Karo

Pingback: CIBIL Score Kaise Badhaye 2026 – 10 Proven Tips

Pingback: Retirement Benefits Tax India — 7 Rules 2026