If you are a daily wage worker, construction laborer, farmer, street vendor, or anyone working without a formal salary, retirement can feel like a distant and uncertain dream. No PF. No gratuity. No pension. Just hard work and hope.

The Government of India created the Atal Pension Yojana 2026 exactly for this reality. It is a government-backed pension scheme that guarantees you a fixed monthly income after the age of 60 — no matter what happens in the market. As of April 2026, over 9 crore Indians have already enrolled in the Atal Pension Yojana 2026, making it the most successful social security scheme in the country’s history.

In this complete guide, you will learn everything about the Atal Pension Yojana 2026 — how it works, who is eligible, how much to contribute, tax benefits, how to apply online, and how to claim your pension. Let us begin.

What Is Atal Pension Yojana 2026?

The Atal Pension Yojana 2026 (APY) is a voluntary pension scheme launched by the Government of India on May 9, 2015. It is managed by the Pension Fund Regulatory and Development Authority (PFRDA) and is available through banks and post offices across India.

The core promise of Atal Pension Yojana 2026 is simple: you contribute a small fixed amount every month until the age of 60, and the government guarantees you a monthly pension ranging from ₹1,000 to ₹5,000 for life after retirement.

The scheme was designed especially for workers in the unorganized sector — those who do not have access to Employee Provident Fund (EPF) or other formal retirement benefits.

In January 2026, the Union Cabinet officially extended the Atal Pension Yojana 2026 till FY 2030–31, ensuring millions of new subscribers can still join and secure their retirement future.

For official scheme details, Visit the official PFRDA website

Key Facts About Atal Pension Yojana 2026

| Feature | Detail |

| Launched | May 9, 2015 |

| Managed By | PFRDA (Government of India) |

| Pension Range | ₹1,000 to ₹5,000/month |

| Lump Sum on Death | Up to ₹8.50 lakh to nominee |

| Age Eligibility | 18 to 40 years |

| Contribution Period | Until age 60 |

| Scheme Extended Until | FY 2030–31 |

| Total Subscribers (April 2026) | 9 crore+ |

| New Enrollments FY 2025–26 | 1.35 crore (highest ever) |

Why Atal Pension Yojana 2026 Matters More Than Ever

The Atal Pension Yojana 2026 extension to FY 2030–31 came at a critical time. India’s unorganized sector employs over 90% of the workforce — and most of these workers have zero retirement savings.

Three reasons make Atal Pension Yojana 2026 essential in today’s environment:

1. No Market Risk — Unlike mutual funds or stocks, APY offers a government-guaranteed pension. Your corpus is protected regardless of market performance.

2. Extremely Low Entry Point — An 18-year-old can secure a ₹5,000/month pension by contributing just ₹210 per month. No other retirement product offers this affordability.

3. Family Protection Built In — If the subscriber dies before 60, the spouse continues receiving pension for life. After both pass away, the nominee receives the full corpus (up to ₹8.50 lakh).

For anyone who wants to understand how different retirement accounts work globally, including the US market, check out our detailed guide on Best SIP Plan to Start Investing Now — a must-read for diaspora investors comparing Indian and international retirement tools.

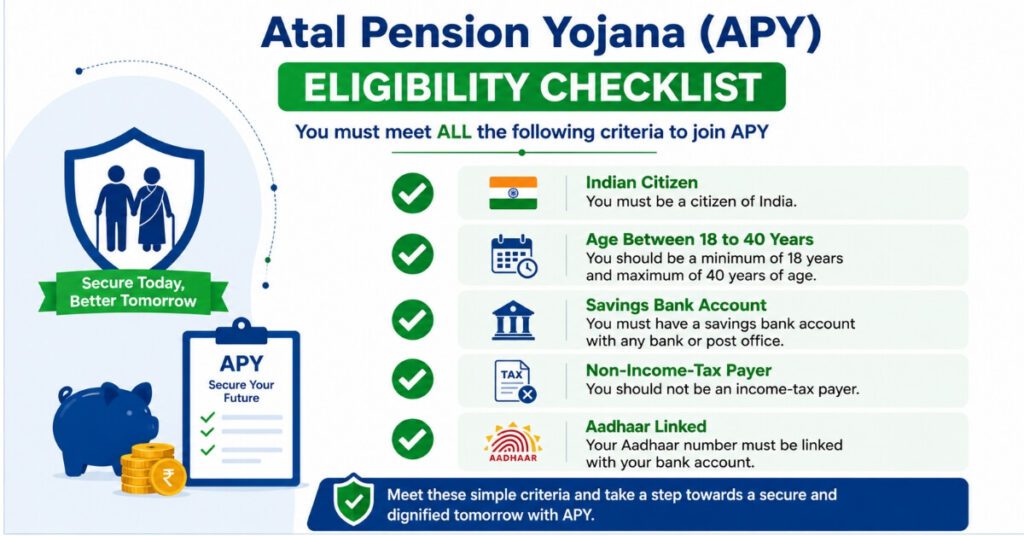

Atal Pension Yojana 2026 — Eligibility Criteria

To join Atal Pension Yojana 2026, you must meet all of the following conditions:

Age: Between 18 and 40 years at the time of enrollment

Citizenship: Indian resident citizen

Bank Account: Active savings bank account or post office savings account (Aadhaar and mobile number linked)

Taxpayer Rule: Since October 1, 2022, income tax payers are NOT eligible to join APY. This rule ensures the scheme stays focused on lower-income groups. If a taxpayer joins and is later identified, the account is closed and only accumulated savings are returned.

No Existing APY Account: A subscriber can hold only one APY account

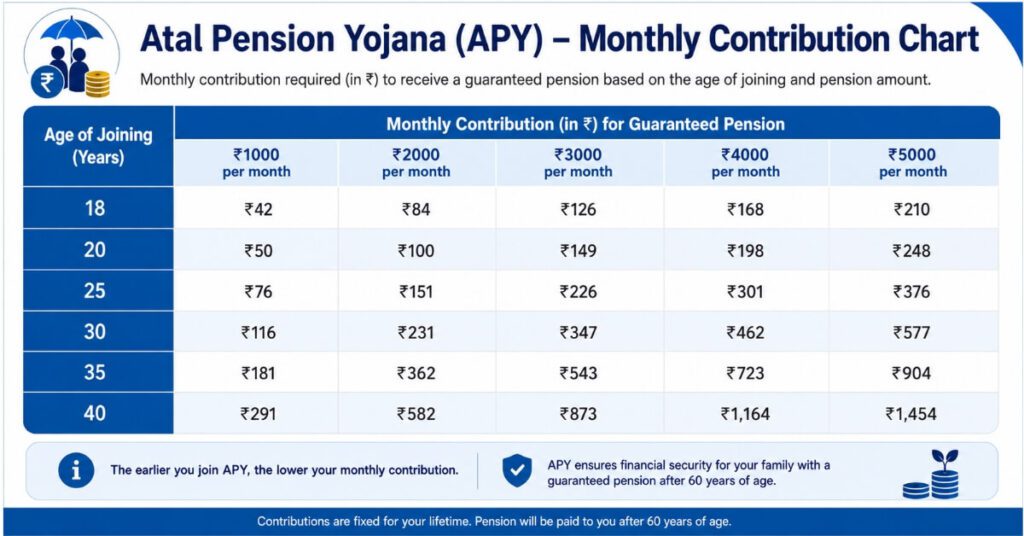

Atal Pension Yojana 2026 — Monthly Contribution Chart

The Atal Pension Yojana 2026 contribution amount depends on two factors: your age when you join and the monthly pension amount you want to receive after 60.

For ₹5,000/month Pension Target (Most Popular)

| Age at Entry | Monthly Contribution | Total Contribution Period |

| 18 years | ₹210 | 42 years |

| 20 years | ₹248 | 40 years |

| 25 years | ₹376 | 35 years |

| 30 years | ₹577 | 30 years |

| 35 years | ₹902 | 25 years |

| 40 years | ₹1,454 | 20 years |

For ₹1,000/month Pension Target (Minimum)

| Age at Entry | Monthly Contribution |

| 18 years | ₹42 |

| 25 years | ₹76 |

| 30 years | ₹116 |

| 40 years | ₹291 |

The message is clear: join Atal Pension Yojana 2026 as early as possible. The earlier you start, the lower your monthly contribution — and the more you benefit from compounding.

Atal Pension Yojana 2026 — Benefits Explained

1. Guaranteed Monthly Pension for Life

After turning 60, you receive a fixed monthly pension of ₹1,000, ₹2,000, ₹3,000, ₹4,000, or ₹5,000 — whichever you chose at the time of enrollment in Atal Pension Yojana 2026. This pension continues for the rest of your life.

2. Spouse Pension Continuation

In case the subscriber passes away, the spouse receives the same pension amount for life. This makes Atal Pension Yojana 2026 a household-level protection plan, not just individual coverage.

3. Nominee Gets Full Corpus

After both subscriber and spouse pass away, the nominee receives the accumulated pension corpus — up to ₹8.50 lakh. This corpus is paid as a lump sum.

4. Government Co-Contribution (Historical)

Earlier subscribers who enrolled between 2015 and 2019 received a 50% co-contribution from the government (up to ₹1,000/year) for the first 5 years. This benefit was for those not covered by other social security schemes and not income tax payers.

5. Flexibility of Contribution Frequency

You can contribute monthly, quarterly, or half-yearly through auto-debit from your savings account. The Atal Pension Yojana 2026 system automatically deducts the amount — you do not need to manually transfer each time.

Tax Benefits Under Atal Pension Yojana 2026

One of the most underrated advantages of Atal Pension Yojana 2026 is its tax benefit:

Contributions to APY are eligible for deduction under Section 80CCD(1) of the Income Tax Act

Additional deduction available under Section 80CCD(1B) up to ₹50,000 over and above the ₹1.5 lakh Section 80C limit

Combined, this means contributions to Atal Pension Yojana 2026 can help you save up to ₹2 lakh per year in tax deductions

Note: Tax benefits apply under the Old Tax Regime. Under the New Tax Regime, these deductions are not available.

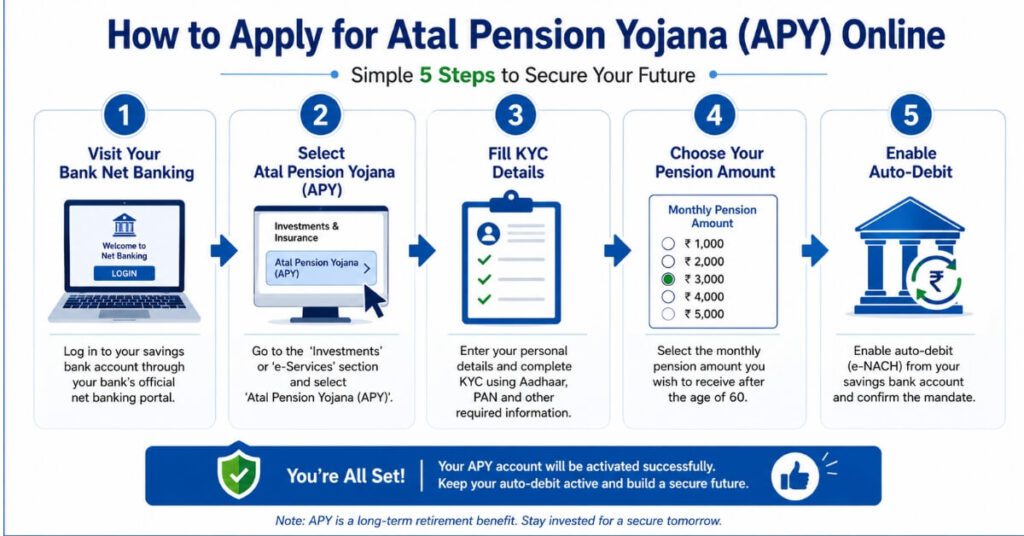

How to Apply for Atal Pension Yojana 2026 — Online and Offline

Option 1: Through Your Bank’s Net Banking

Most Indian banks (SBI, HDFC, ICICI, Canara, PNB, Axis, Kotak) allow you to open an Atal Pension Yojana 2026 account directly through mobile banking or internet banking:

1 .Log in to your bank’s net banking or mobile app

2 .Search for “APY” or “Atal Pension Yojana”

3 .Enter your basic details — Aadhaar, nominee info, date of birth

4 .Select your desired monthly pension (₹1,000 to ₹5,000)

5 .Choose contribution frequency (monthly/quarterly/half-yearly)

6 .Enable auto-debit consent and submit

The entire process takes 10–15 minutes online.

Option 2: Through the eNPS/e-APY Portal

1 .Visit the NPS CRA portal (npscra.nsdl.co.in)

2 .Select “Atal Pension Yojana” registration

3 .Complete Aadhaar-based OTP verification

4 .Fill subscriber details and nominee information

5 .Choose pension amount and contribution frequency

6 eSign and submit — your PRAN card is generated digitally

Option 3: Offline Through Bank or Post Office

Visit any bank branch or post office where you hold a savings account. Ask for the Atal Pension Yojana 2026 registration form (Form APY-1), fill it out, and submit with your Aadhaar copy and bank passbook.

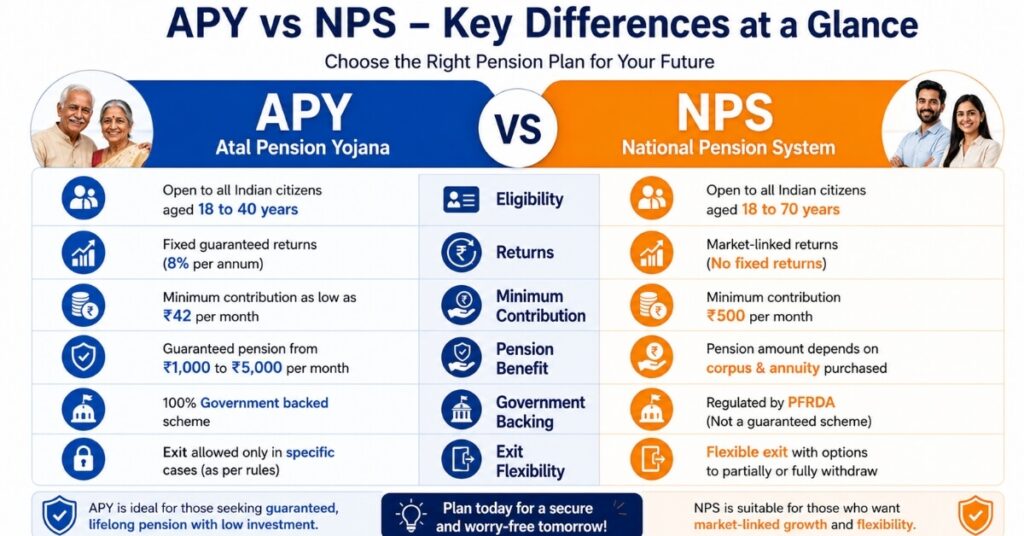

APY vs NPS — Which One Should You Choose in 2026?

Many people confuse Atal Pension Yojana 2026 with the National Pension System (NPS). Here is a clear comparison

| Feature | APY | NPS |

| Target Audience | Unorganized sector, non-taxpayers | Salaried, self-employed, all citizens |

| Returns | Government-guaranteed fixed pension | Market-linked, variable returns |

| Minimum Contribution | ₹42/month | ₹500/month |

| Pension Range | ₹1,000–₹5,000/month fixed | Depends on corpus at 60 |

| Income Tax Payer Eligible? | No (since Oct 2022) | Yes |

| Corpus to Nominee | Up to ₹8.50 lakh | Full accumulated corpus |

| Flexibility | Fixed plan | High flexibility |

| Government Backing | Yes — guaranteed | Partial |

If you are a non-taxpayer in the unorganized sector, Atal Pension Yojana 2026 is the clear winner. For salaried professionals and taxpayers, NPS offers better flexibility and higher potential returns.

What Happens If You Miss APY Contributions?

If the auto-debit fails due to insufficient balance, a small penalty is charged:

| Monthly Contribution | Penalty Per Month of Default |

| ₹100 or less | ₹1 |

| ₹101–₹500 | ₹2 |

| ₹501–₹1,000 | ₹5 |

| Above ₹1,000 | ₹10 |

If contributions are not paid for 6 consecutive months, the account is frozen. After 12 months, it becomes deactivated. After 24 months, the account may be closed and the accumulated corpus returned to the subscriber.

To reactivate a frozen Atal Pension Yojana 2026 account, you need to pay all overdue contributions plus penalties in one go. Always ensure sufficient balance on your SIP auto-debit date.

Early Exit From Atal Pension Yojana 2026 — Rules

Normal Exit: At age 60, you begin receiving the guaranteed monthly pension for life.

Voluntary Exit Before 60: Allowed only in exceptional circumstances. If you exit early:

Only your own contributions + earned interest are returned

Government co-contribution and accumulated returns on it are not refunded

Applicable taxes will be deducted as per income tax rules

Exit on Death Before 60:

Spouse can continue contributing and receive the full pension at 60, OR

Spouse can choose to exit and receive the full accumulated corpus immediately

This makes Atal Pension Yojana 2026 one of the most family-friendly pension schemes available to India’s unorganized workers.

Atal Pension Yojana 2026 — 2026 Updates You Must Know

Several important updates make Atal Pension Yojana 2026 more relevant than ever:

1. Extended to FY 2030–31: Union Cabinet approved the extension on January 21, 2026 — giving more Indians a longer window to join.

2. 9 Crore Subscriber Milestone: APY crossed 9 crore total gross enrollments on April 21, 2026 — the fastest growth in its history.

3. FY 2025–26: Highest-Ever New Enrollments: 1.35 crore new subscribers joined in a single year — a record that shows rising awareness among unorganized workers.

4. Higher Pension Under Consideration: PFRDA is actively evaluating a proposal to raise the maximum guaranteed pension above ₹5,000/month, which would be a major upgrade for Atal Pension Yojana 2026 subscribers.

5. Corpus Crosses ₹54,000 Crore: Total assets under APY management crossed ₹54,000 crore in 2026, ensuring the fund remains financially robust.

Who Should Join Atal Pension Yojana 2026?

Atal Pension Yojana 2026 is ideal for:

Daily wage workers, construction workers, domestic helpers

Agricultural laborers and small farmers

Rickshaw pullers, auto drivers, street vendors

Artisans, weavers, fishermen

Small shop owners and self-employed individuals who are non-taxpayers

Young adults (18–25 years) who want to lock in the lowest possible contribution rate

If you earn income in any of these categories and do not file income tax returns, Atal Pension Yojana 2026 is literally built for you.

Frequently Asked Questions (FAQs)

Q1. What is the Atal Pension Yojana 2026?

Atal Pension Yojana 2026 is a government-backed pension scheme managed by PFRDA, offering a guaranteed monthly pension of ₹1,000 to ₹5,000 to Indian citizens aged 18–40 in the unorganized sector after they turn 60.

Q2. Who is eligible for Atal Pension Yojana 2026?

Indian citizens aged 18–40 with an active savings bank account who are not income tax payers are eligible for Atal Pension Yojana 2026. Aadhaar and mobile number linking is mandatory.

Q3. How much do I need to contribute monthly?

It depends on your age and chosen pension amount. An 18-year-old wanting ₹5,000/month needs to pay ₹210/month. A 40-year-old wanting the same pension pays ₹1,454/month. The earlier you join Atal Pension Yojana 2026, the lower your contribution.

Q4. Is Atal Pension Yojana 2026 safe?

Yes — it is 100% government-guaranteed. Your pension amount is guaranteed regardless of market conditions, making Atal Pension Yojana 2026 one of the safest retirement products in India.

Q5. Can I have both APY and NPS accounts?

You can hold an Atal Pension Yojana 2026 account and an NPS account simultaneously — provided you meet the eligibility criteria for both.

Q6. What happens to my APY account if I become a taxpayer?

If you become an income tax payer after enrolling in Atal Pension Yojana 2026, your account will be closed by the government and only your accumulated contributions + interest will be returned. No government co-contribution is refunded.

Q7. Can I increase my pension amount after joining?

Yes — you can upgrade your pension slab (from ₹1,000 to ₹2,000, etc.) once per year during April each year in Atal Pension Yojana 2026. Your contribution will increase accordingly.

Q8. Is there a nominee facility in APY?

Yes — you must declare a nominee at enrollment. After both subscriber and spouse pass away, the nominee receives the full accumulated corpus (up to ₹8.50 lakh) as a lump sum from Atal Pension Yojana 2026.

Conclusion

The Atal Pension Yojana 2026 is not just a government scheme — it is a financial lifeline for crore of Indians who work hard every day without any safety net for tomorrow. With guaranteed pension, family protection, tax benefits, and a government extension till FY 2030–31, this scheme has never been more accessible or more essential.

Whether you are 18 or 39, whether you contribute ₹42 or ₹1,454 per month — the most important step is to join Atal Pension Yojana 2026 today. Because every month you delay means a higher contribution later.

Open your bank app, search for APY, and complete enrollment in under 15 minutes. Your retirement is worth 15 minutes of action today.

Disclaimer

This article is for educational and informational purposes only. The information provided about Atal Pension Yojana 2026 is based on publicly available PFRDA and government sources as of June 2026. Pension rules, contribution amounts, eligibility criteria, and tax benefits may change over time. Please verify the latest details on the official PFRDA website (pfrda.org.in) or consult a SEBI/PFRDA-registered financial advisor before making any investment or enrollment decision. SK Smart Digital Hub does not provide personalized financial advice.

Pingback: EPFO Nomination Update: Easy Step-by-Step Guide 2026