Introduction

India has become one of the world’s leading countries in digital payments. From buying groceries at a local shop to paying utility bills online, digital transactions have become a part of everyday life. Most people are already familiar with UPI, but many are now hearing about the Digital Rupee and wondering how it differs from existing payment methods.

The discussion around UPI vs Digital Rupee has gained significant attention since the Reserve Bank of India (RBI) introduced its Central Bank Digital Currency (CBDC), commonly known as the RBI e-Rupee. While both options support digital transactions, they are fundamentally different in how they work, who issues them, and their role in India’s financial ecosystem.

Understanding UPI vs Digital Rupee is important for anyone interested in digital payment India trends, cashless transactions, and the future of money. Whether you are a student, salaried employee, business owner, or simply curious about financial technology, this guide will help you understand the differences in simple language.

In this comprehensive article, we will explore UPI vs Digital Rupee, their features, advantages, disadvantages, and which option may be better for different users.

What Is UPI? Complete Guide

UPI stands for Unified Payments Interface. It is a real-time payment system developed by the National Payments Corporation of India (NPCI). The system allows users to instantly transfer money between bank accounts using smartphones.

Today, UPI has become the backbone of digital payment India initiatives. Millions of people use UPI every day through apps such as Google Pay, PhonePe, Paytm, BHIM, and Amazon Pay.

When discussing UPI vs Digital Rupee, it is important to understand that UPI is not money itself. Instead, it is a payment system that helps move money from one bank account to another.

How Does UPI Work?

UPI connects multiple bank accounts into a single mobile application. Users can send and receive money using:

Mobile numbers

UPI IDs

QR codes

Bank account details

A typical UPI transaction follows these steps:

1 .Open a UPI-enabled app.

2 .Enter payment details or scan a QR code.

3 .Enter the UPI PIN.

4 .Complete the transaction instantly.

This convenience has made UPI one of the most successful digital payment systems in the world.

Key Features of UPI

Some important features include:

Instant money transfer

24/7 availability

Secure authentication

Easy QR code payments

Direct bank account connectivity

Low transaction costs

The popularity of UPI often leads people to compare UPI vs Digital Rupee, but both serve different purposes despite appearing similar.

Benefits of UPI

UPI offers several advantages:

Fast transactions

User-friendly interface

Wide acceptance across India

No need to carry cash

Easy bill payments

Seamless online shopping experience

These advantages have played a major role in promoting a cashless economy.

Limitations of UPI

Despite its success, UPI has certain limitations:

Requires a bank account

Depends on internet connectivity

Transaction failures may occur

Bank server issues can affect payments

Not a form of digital currency

These limitations become relevant when analyzing UPI vs Digital Rupee in detail.

What Is Digital Rupee? RBI’s New Digital Currency

The Digital Rupee, also known as e₹ or RBI e-Rupee, is India’s official Central Bank Digital Currency (CBDC). It is issued directly by the Reserve Bank of India.

Official RBI Website: https://www.rbi.org.in

Unlike UPI, which transfers money from a bank account, the Digital Rupee itself is a form of money issued by the central bank.

This distinction is one of the most important aspects of UPI vs Digital Rupee.

What Is a CBDC?

A Central Bank Digital Currency is a digital version of a country’s sovereign currency.

Just as physical notes and coins are issued by RBI, the Digital Rupee is issued electronically by RBI.

In simple terms:

Cash = Physical currency

Digital Rupee = Digital currency

Both represent legal tender backed by the Government of India and RBI.

How Does the Digital Rupee Work?

The RBI issues Digital Rupee through participating banks.

Users can:

Download a supported wallet

Store Digital Rupee tokens

Send money digitally

Receive digital currency instantly

Unlike traditional digital payments, Digital Rupee transactions involve transferring digital currency rather than moving funds between bank accounts.

This is another crucial difference in the UPI vs Digital Rupee debate.

Key Features of Digital Rupee

Important features include:

Issued directly by RBI

Legal tender status

Digital form of cash

Secure transactions

Reduced dependency on physical cash

Potential offline transaction capability

The RBI e-Rupee is considered a major step toward digital currency India initiatives.

Why Did RBI Introduce Digital Rupee?

The RBI introduced Digital Rupee to:

Modernize payment systems

Reduce cash handling costs

Improve financial inclusion

Strengthen digital infrastructure

Support a cashless economy

Provide sovereign digital currency

As digital payments continue to grow, understanding UPI vs Digital Rupee becomes increasingly important for consumers and businesses.

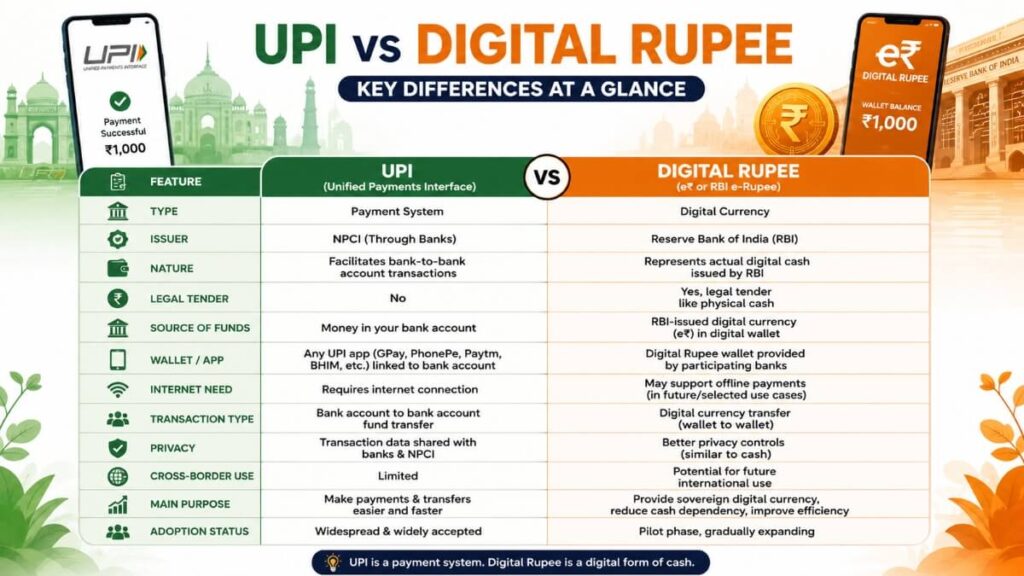

UPI vs Digital Rupee – 10 Major Differences

The easiest way to understand UPI vs Digital Rupee is through a detailed comparison.

| Feature | UPI | Digital Rupee |

| Type | Payment System | Digital Currency |

| Issuer | NPCI Framework | RBI |

| Money Source | Bank Account | RBI-issued Currency |

| Legal Tender | No | Yes |

| Wallet Required | No | Yes |

| Bank Dependency | High | Lower |

| Transaction Nature | Account Transfer | Currency Transfer |

| Offline Potential | Limited | Possible |

| Currency Form | Not Currency | Actual Currency |

| Future Role | Payment Network | Digital Cash |

1. Nature of the System

The biggest difference in UPI vs Digital Rupee is that UPI is a payment mechanism while Digital Rupee is actual money.

2. Issuing Authority

UPI operates through NPCI and banks, while Digital Rupee is issued directly by RBI.

3. Source of Funds

In UPI vs Digital Rupee, UPI transactions use money already stored in bank accounts, whereas Digital Rupee uses RBI-issued digital currency.

4. Legal Tender Status

The Digital Rupee has legal tender status similar to physical cash. UPI itself does not have legal tender status because it is only a payment channel.

5. Dependency on Banks

6. Transaction Method

UPI moves account balances. Digital Rupee transfers currency tokens directly between wallets.

7. Privacy Considerations

Many experts discussing UPI vs Digital Rupee believe Digital Rupee may offer cash-like characteristics in certain use cases, although regulations continue to evolve.

8. Offline Capability

Future versions of Digital Rupee may support offline payments more effectively than current UPI systems.

9. Financial Infrastructure

UPI depends heavily on banking infrastructure, while Digital Rupee introduces a new digital currency layer.

10. Future Potential

When analyzing UPI vs Digital Rupee, many experts believe both technologies will coexist and complement each other rather than compete directly.

Digital Rupee Benefits and Drawbacks

Understanding the advantages and disadvantages is essential when comparing UPI vs Digital Rupee. While the Digital Rupee is still in its growth phase, it offers several promising benefits.

Benefits of Digital Rupee

1. Official RBI-Backed Currency

The biggest advantage in the UPI vs Digital Rupee comparison is that the Digital Rupee is issued directly by the Reserve Bank of India. This gives it the same trust and credibility as physical cash.

2. Supports a Cashless Economy

The RBI e-Rupee can help India move further toward a cashless economy while maintaining the reliability of sovereign currency.

3. Faster Settlement

Digital Rupee transactions can potentially provide instant settlement without relying entirely on traditional banking processes.

4. Reduced Cash Management Costs

Printing, transporting, and securing physical cash is expensive. Digital currency India initiatives can help reduce these costs over time.

5. Future Offline Payments

One of the most discussed topics in UPI vs Digital Rupee is offline payment capability. Future Digital Rupee systems may allow transactions even when internet connectivity is limited.

6. Improved Financial Inclusion

Digital Rupee could help bring more people into the formal financial system, especially in areas with limited banking access.

Drawbacks of Digital Rupee

Despite its benefits, there are some challenges:

Limited adoption compared to UPI

Many users are still unfamiliar with RBI e-Rupee

Merchant acceptance is still growing

Requires user education

Wallet infrastructure is still developing

Because of these factors, the UPI vs Digital Rupee debate remains highly relevant as both systems continue to evolve.

UPI Benefits and Drawbacks

UPI has transformed digital payment India and remains one of the most successful payment innovations globally.

Benefits of UPI

1. Easy to Use

UPI applications are simple and user-friendly. Even first-time users can make payments within minutes.

2. Widely Accepted

When discussing UPI vs Digital Rupee, UPI currently has a significant advantage in merchant acceptance. Almost every online and offline business accepts UPI payments.

3. Instant Transactions

Money transfers happen in real time, making UPI extremely convenient.

4. No Need to Carry Cash

Users can complete transactions directly from their smartphones.

5. Supports Multiple Banks

A single UPI app can connect multiple bank accounts.

6. Available 24/7

Unlike some traditional banking services, UPI works around the clock.

Drawbacks of UPI

UPI also has some limitations:

Requires internet access

Depends on bank servers

Transaction failures can occur

Requires a bank account

Vulnerable to phishing scams if users are careless

These factors are important when evaluating UPI vs Digital Rupee for long-term usage.

UPI vs Digital Rupee: Which One Should You Use?

Many people ask whether they should choose UPI or Digital Rupee. The answer depends on your needs.

Use UPI If:

You already use mobile banking.

You want maximum merchant acceptance.

You make frequent daily transactions.

You need a familiar payment method.

Use Digital Rupee If:

You want to experience RBI-backed digital currency.

You are interested in future financial technology.

You want an alternative form of digital cash.

You wish to participate in India’s CBDC ecosystem.

The reality is that the UPI vs Digital Rupee discussion should not be viewed as a competition. Both systems serve different purposes.

UPI is a payment system, while Digital Rupee is a form of money.

As India’s digital ecosystem grows, many experts believe UPI and Digital Rupee will work together rather than replace each other.

This is one of the most important conclusions in the UPI vs Digital Rupee debate.

Future of UPI and Digital Rupee in India

India is rapidly becoming a global leader in digital payments. The combination of UPI payment system innovation and RBI e-Rupee development could create one of the world’s most advanced financial ecosystems.

Potential future developments include:

Offline Digital Rupee payments

Wider merchant acceptance

Integration with government services

Faster international payment solutions

Enhanced digital currency infrastructure

As technology advances, the UPI vs Digital Rupee conversation will continue to evolve.

Consumers who understand UPI vs Digital Rupee today will be better prepared for tomorrow’s financial landscape.

Official Resources:

Frequently Asked Questions (FAQs)

1. What is the main difference between UPI vs Digital Rupee?

The primary difference in UPI vs Digital Rupee is that UPI is a payment system, while Digital Rupee is actual digital currency issued by RBI.

2. Is Digital Rupee better than UPI?

Not necessarily. The UPI vs Digital Rupee comparison depends on your use case. UPI is currently more widely accepted, while Digital Rupee represents the future of sovereign digital currency.

3. Can I use Digital Rupee through UPI apps?

Some integrations may become available in the future, but Digital Rupee generally operates through approved wallets.

4. Is Digital Rupee safe?

Yes. The RBI e-Rupee is issued and regulated by RBI, making it one of the safest forms of digital currency India offers.

5. Does Digital Rupee replace cash?

No. Digital Rupee complements cash rather than replacing it completely.

6. Will UPI disappear after Digital Rupee launches?

No. Most experts believe the UPI vs Digital Rupee discussion is about coexistence, not replacement.

7. Which is more suitable for daily payments?

Currently, UPI remains the most practical choice for everyday transactions because of its widespread acceptance.

“While understanding UPI vs Digital Rupee is important, investors should also explore Best SIP Plan to Invest Now for long-term wealth creation.”

Conclusion

The discussion around UPI vs Digital Rupee is becoming increasingly important as India moves toward a more digital financial future. Although both systems support digital transactions, they are fundamentally different.

UPI is a payment network that transfers money between bank accounts, while the Digital Rupee is a central bank-issued digital currency backed directly by RBI. Understanding UPI vs Digital Rupee helps consumers make informed decisions about how they manage and spend money in the digital age.

For most users today, UPI remains the preferred option due to its convenience and widespread acceptance. However, the Digital Rupee has enormous long-term potential and could play a major role in shaping the future of digital payment India.

As RBI continues expanding the RBI e-Rupee ecosystem, staying informed about UPI vs Digital Rupee will help you adapt to the next generation of financial technology.

If you found this guide useful, share it with friends and family so they can also understand UPI vs Digital Rupee and make smarter digital payment decisions.