If you have been searching for information about Sovereign Gold Bond 2026, you are not alone. Thousands of Indian investors have been typing this exact phrase into Google over the past few weeks, hoping to find a fresh issue date, updated interest rates, or a simple way to buy gold bonds online. The truth is a little more complicated than most search results suggest.

The Sovereign Gold Bond 2026 scheme, once a favourite among Indian households looking for a safer way to hold gold, is currently going through a quiet but significant change. The Reserve Bank of India has not opened any new subscription window this year, and that single fact has left a lot of confused investors wondering what to do next. Many are still finding outdated articles online that talk about upcoming tranches, application windows, and discount rates that no longer apply.

This guide breaks down everything you need to know — the current status, what existing bondholders should expect, the tax rules that apply, and the alternatives available if you still want gold exposure in your portfolio, all explained in simple, practical terms.

What Is the Sovereign Gold Bond Scheme?

Before understanding why Sovereign Gold Bond 2026 search queries are flooding Google, it helps to revisit what this instrument actually is.

Sovereign Gold Bonds (SGBs) are government securities denominated in grams of gold. Instead of buying physical gold — with all its storage worries, making charges, and purity concerns — investors buy a paper or dematerialised form of gold issued directly by the Reserve Bank of India on behalf of the Government of India.

Each Sovereign Gold Bond 2026 unit represents one gram of gold, and the price is fixed based on the average closing price of 999 purity gold published by the India Bullion and Jewellers Association. On top of any gains from rising gold prices, Sovereign Gold Bond 2026 holders also earn a fixed 2.5% annual interest, paid semi-annually.

This dual benefit — capital appreciation plus fixed interest — is what made the scheme so popular between 2015 and 2025, especially among conservative investors who wanted gold exposure without the hassle of physical storage or jewellery-related deductions.Article me is paragraph ko replace kar dijiye. Agar aap chahein to main pura article dobara count kar ke confirm kar sakti hoon ki focus keyword exactly 27 baar aa raha hai ya nahi — bataiye?

The bonds carry an 8-year tenure, with an exit window available starting from the 5th year, exercisable on interest payment dates announced by the RBI.

Current Status of Sovereign Gold Bond 2026

Here is the most important update for anyone researching Sovereign Gold Bond 2026: there is no active issuance calendar right now. The Reserve Bank of India has not announced a new tranche for the current financial year, which means new investors cannot subscribe to fresh Sovereign Gold Bond 2026 units through banks, post offices, or stock exchanges the way they could in previous years.

This is a notable shift. For nearly a decade, the government issued SGB tranches in scheduled windows throughout the year, each open for a few days at a time, with a small discount for online applications. That pattern has stopped for now. Financial portals and comparison websites still show old tranche information, which is why so many search results feel outdated or contradictory.

If you are looking to buy a completely new bond directly from the government, that option is not currently available. What remains open is the secondary market, where existing SGB units can be bought and sold on stock exchanges like the NSE and BSE, subject to prevailing market pricing and liquidity conditions.

Why Has the Sovereign Gold Bond Scheme Been Paused?

There is no single official reason published for the pause, but a few factors are widely discussed among market analysts and financial commentators. The government’s borrowing cost through SGBs became noticeably higher than through regular bonds once gold prices rallied sharply, since the redemption amount is directly linked to the market price of gold at maturity. Rising global gold prices have meant a growing liability for the exchequer with every passing tranche.

Gold ETFs and other market-linked instruments have also matured significantly in India over the past few years, giving retail investors alternative routes to gold exposure without the government having to issue new paper every few months. Whatever the exact reasoning behind the decision, the practical outcome for anyone tracking Sovereign Gold Bond 2026 news is the same: no new subscriptions are open, only secondary market activity and management of existing holdings continues.

What Happens to Existing Sovereign Gold Bond Holders?

If you already hold SGB units from an earlier tranche, nothing changes for you in terms of your existing investment. Your bonds continue to earn a fixed 2.5% annual interest, paid semi-annually directly into your registered bank account, exactly as promised at the time of purchase.

Your capital is still linked to the price of gold. If gold prices rise between your purchase date and redemption, your maturity value rises with it. This is one of the strongest features of the scheme and remains completely unaffected even though Sovereign Gold Bond 2026 issuance is currently paused for new investors.

Premature redemption is allowed starting from the 5th year of holding, and this can be exercised only on the specific interest payment dates announced by the RBI — typically opening in the 5th, 6th, and 7th year windows for each tranche. If you miss a redemption window, you simply continue holding the bond until the next available date or full maturity at the end of 8 years, without losing any benefit.

It is worth checking your bond’s original tranche details on your Demat statement or bank passbook, since redemption prices and eligible dates vary from tranche to tranche.

Interest Rate and Redemption Rules Explained

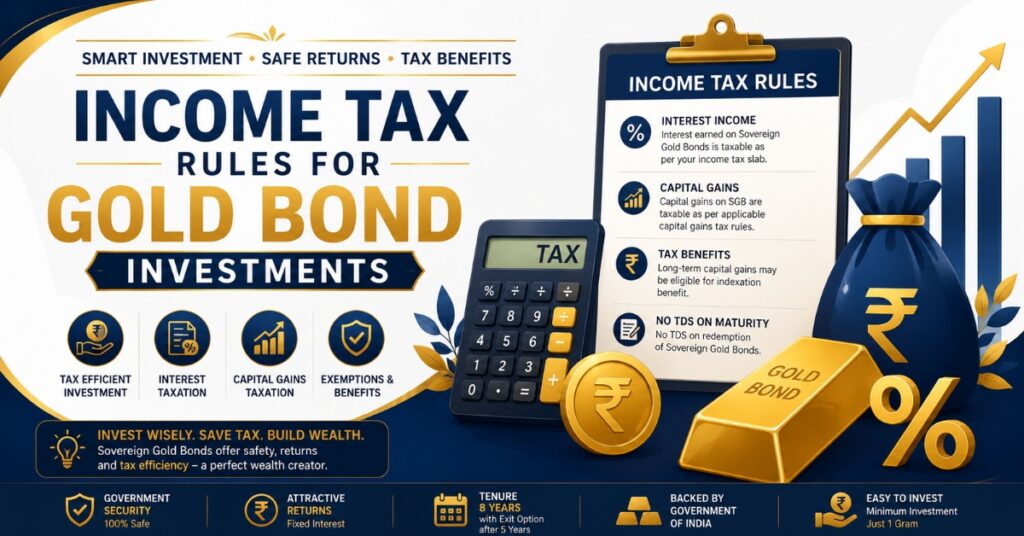

The fixed interest rate on Sovereign Gold Bond holdings — for anyone who purchased in earlier tranches — remains at 2.5% per annum on the initial investment amount. This is paid out twice a year and is fully taxable under “Income from Other Sources,” regardless of your total income bracket or the size of your holding.

Redemption pricing is based on the simple average closing price of gold of 999 purity for the three business days preceding the redemption date, as published by the India Bullion and Jewellers Association. This means the exact amount you receive can vary slightly depending on short-term gold price movements around your specific redemption window, so timing your exit does make a small difference to your final payout.

Tax Rules for Sovereign Gold Bond 2026 Investors

Tax treatment is one of the most misunderstood aspects of Sovereign Gold Bond 2026 investing, and recent budget changes have made it even more important to get right before making any decisions.

If you are the original subscriber of an SGB tranche and you hold the bond until its full 8-year maturity, the capital gains earned are completely exempt from tax. This is a unique advantage that no other gold investment option in India currently offers, and it remains one of the strongest reasons to continue holding existing bonds rather than selling early.

However, if you exit early — either through the premature redemption window from year 5 onwards, or by selling in the secondary market — the tax exemption does not apply in the same way. Gains from premature redemption exercised through the official RBI window are still exempt for original subscribers, but gains from selling on the stock exchange before maturity are treated as regular capital gains and taxed based on your holding period, with different rates applying to short-term and long-term gains.

The semi-annual interest income, as mentioned earlier, is always taxable as per your applicable income slab, irrespective of how long you eventually hold the bond or whether you qualify for the maturity tax exemption.

Alternatives to Sovereign Gold Bond 2026 for New Investors

Since fresh Sovereign Gold Bond 2026 subscriptions are not available, investors who still want gold exposure in their portfolio have a few practical options to consider.

Gold ETFs (Exchange Traded Funds) are the closest substitute. They track the price of physical gold, trade on stock exchanges just like shares, and can be bought or sold on any trading day without waiting for a government issuance window. Unlike SGBs, they do not pay any interest, but they offer far greater liquidity and flexibility for investors who may need to exit at short notice.

Digital Gold, offered through various payment apps and jewellers, allows you to buy small quantities of 24-karat gold starting from very small amounts, sometimes as little as one rupee. It is convenient but usually carries higher costs due to making charges and GST compared to ETFs or bonds, so it works better for very small, occasional purchases than for serious long-term allocation.

Buying SGB units in the secondary market is another route. Since existing bonds trade on the NSE and BSE, you can purchase units from other investors at the prevailing market price, though liquidity can be limited for smaller or older tranches, and you will not get the same tax-free maturity benefit as an original subscriber.

If your broader goal is disciplined, long-term wealth building rather than gold exposure specifically, it also helps to diversify into other instruments alongside your gold allocation. For instance, many readers who are building a long-term investment habit have found the SIP 8 4 3 Rule — a simple formula for compounding wealth through systematic investment — a useful framework to plan their monthly investments while they wait for gold-linked options to evolve further.

Is Sovereign Gold Bond 2026 a Good Investment Right Now?

For investors who already hold Sovereign Gold Bond 2026 units, holding until maturity remains an attractive, tax-efficient strategy, especially given the tax-free capital gains benefit reserved for original subscribers who stay invested for the full 8-year term.

For new investors hoping to enter the scheme, the honest answer is that you currently cannot, at least not through a fresh government issuance. Your realistic choices are the secondary market, Gold ETFs, or Digital Gold, each with its own trade-offs in terms of liquidity, cost, and tax treatment that you should weigh against your personal financial goals.

It is worth keeping an eye on official announcements from the RBI and the Ministry of Finance, as government policy on Sovereign Gold Bond 2026 issuance can change without much advance notice. Many investors bookmark the official RBI website specifically to track this, since it remains the most reliable source for any future announcements.

How to Track Sovereign Gold Bond Updates

Since there is no scheduled calendar right now, the best way to stay updated on Sovereign Gold Bond 2026 news is to periodically check the Reserve Bank of India’s official notifications page, along with your bank’s investment section if you already hold bonds through a bank account.

Financial news portals, brokerage apps, and your Demat account provider will typically notify you before any redemption window opens for your specific tranche. It is a good habit to note your bond’s issue date and tranche number so you can track its relevant redemption dates precisely, rather than relying on generic articles that may not apply to your exact holding.

Frequently Asked Questions

Q1.What is the current status of Sovereign Gold Bond 2026?

As of now, no new tranche has been issued, and the scheme remains paused for fresh subscriptions. Existing bondholders continue to earn interest and can redeem as per their original tranche schedule.

Q2.Can I still buy Sovereign Gold Bond 2026 units?

You cannot subscribe through a new government issuance, but you can purchase existing units through the secondary market on the NSE or BSE at prevailing market prices.

Q3.Is the interest on SGB taxable?

Yes, the 2.5% annual interest is fully taxable under “Income from Other Sources,” regardless of the exemption available on capital gains at maturity.

Q4.What happens if I miss the premature redemption window?

You simply continue holding the bond until the next redemption window or full maturity at the end of 8 years, without any penalty or loss of benefit.

Q5.Are Gold ETFs a good alternative to Sovereign Gold Bond 2026?

Gold ETFs offer more liquidity and do not require waiting for a government issuance, but they do not pay any interest, unlike SGBs.

Q6.Will the government restart Sovereign Gold Bond issuance in the future?

There is no official confirmation either way. Investors are advised to track RBI announcements rather than rely on speculation from financial portals.

Conclusion

The conversation around Sovereign Gold Bond 2026 is really a story about a scheme in transition. For long-time investors, the fundamentals have not changed — your interest payments, redemption rights, and tax benefits remain intact exactly as they were promised. For new investors, the door to fresh SGB units is temporarily closed, pushing many towards Gold ETFs, Digital Gold, or the secondary market instead.

Whatever route you choose, gold should ideally remain one part of a diversified portfolio rather than its entire foundation. Keeping track of official Sovereign Gold Bond 2026 announcements, understanding the tax rules that apply to your specific situation, and pairing your gold allocation with disciplined equity or mutual fund investments will serve you far better in the long run than chasing headlines alone.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial, investment, or tax advice. Gold and bond markets are subject to risk, and past performance is not indicative of future returns. Please consult a certified financial advisor or tax professional before making any investment decisions related to SGB or any other financial product.

Pingback: Home Loan Overdraft Facility: 5 Proven Ways to Save Big