The SIP 8 4 3 rule is one of the most talked-about wealth-building concepts in personal finance today, and for good reason. If you have ever wondered how a simple monthly investment of Rs. 21,250 can quietly transform into Rs. 1 crore, this compounding framework explains exactly how it happens. This article breaks down the SIP 8 4 3 rule in plain language, shows you the year-by-year math, and helps you decide whether this strategy fits your own financial goals.

Most people start a Systematic Investment Plan hoping to build long-term wealth, but very few understand the actual mechanics of how that wealth accumulates. This concept gives you a clear, three-phase roadmap that makes the entire compounding journey easy to visualize. Instead of staring at a random maturity number after fifteen years, it shows you exactly when your money doubles, when it doubles again, and when the final surge to your target corpus happens. Understanding this pattern early can completely change how patiently you approach long-term investing.

What Is the SIP 8 4 3 Rule?

The SIP 8 4 3 rule is a simple framework used to explain how a mutual fund SIP grows in three distinct stages over a fifteen-year period, assuming an average annual return of around 12 percent. The numbers 8, 4, and 3 refer to the number of years it takes for your invested corpus to complete each phase of growth.

According to this framework, your money takes the first 8 years to build a solid base through steady, disciplined investing. In the next 4 years, the corpus roughly doubles again because compounding starts working faster on a larger base. Finally, in the last 3 years, this rule reveals the most dramatic phase, where your money grows almost as much as it did in the first eight years combined, purely because of the scale compounding has reached by that point.

This is why the SIP 8 4 3 rule is often described as a “secret” — not because the math is hidden, but because most investors quit too early, right before the most powerful phase kicks in. Financial educators use this three-phase breakdown precisely because raw numbers on a spreadsheet rarely convince anyone to stay invested for over a decade. Seeing the journey mapped out in distinct, understandable stages makes the discipline required feel achievable rather than abstract.

Breaking Down the SIP 8 4 3 Rule: Rs. 21,250 Per Month Example

Let’s apply this framework to a real, relatable number. Suppose you start a monthly SIP of Rs. 21,250 in an equity mutual fund that delivers an average annual return of 12 percent. Here is how the journey plays out over fifteen years.

Phase 1 (Years 1 to 8): During this stage, growth is slow and steady. You invest Rs. 21,250 every month, totaling roughly Rs. 20.4 lakh in contributions over 8 years. Thanks to compounding, this grows to approximately Rs. 34 lakh by the end of year 8. This is the discipline-building stage of the SIP 8 4 3 rule, where patience matters more than excitement. Many investors find this phase the most difficult psychologically, because the monthly statements look almost identical to the amount they have contributed, with only a small visible gain from returns.

Phase 2 (Years 9 to 12): This is where the strategy starts to show its real strength. Over the next 4 years, your corpus roughly doubles from Rs. 34 lakh to nearly Rs. 66-68 lakh. You are still investing the same Rs. 21,250 every month, but the base is now large enough that compounding does most of the heavy lifting. This is the phase where the SIP 8 4 3 rule separates patient investors from those who stop too soon, since the visible acceleration in corpus value often tempts people to either withdraw early or, conversely, become overconfident and take on unnecessary risk.

Phase 3 (Years 13 to 15): The final and most exciting stage of this journey. In just 3 years, your corpus jumps from around Rs. 68 lakh to over Rs. 1 crore. This last leg adds nearly as much wealth as the entire first eight years combined, purely because compounding is now working on a much bigger base. It is a vivid demonstration of why financial advisors constantly repeat that time in the market beats timing the market.

By the end of 15 years, your total investment through this plan is around Rs. 38.25 lakh, while the remaining amount — well over Rs. 61 lakh — comes purely from the power of compounding. This is the core lesson every investor should take from the SIP 8 4 3 rule: consistency and patience, not perfect timing, are what actually build wealth.

Why the SIP 8 4 3 Rule Works: The Power of Compounding

At its core, this framework is essentially a visual representation of compound interest applied to mutual fund investing. Compounding means you earn returns not just on your original investment, but also on the returns generated in previous years. In the early years, growth feels slow because the base amount is small. But as the years pass, the base grows large enough that even a modest 12 percent annual return generates massive absolute gains.

This is exactly why the SIP 8 4 3 rule breaks the journey into three phases instead of showing a flat, linear graph. It helps investors emotionally prepare for a slow start and stay invested long enough to reach the explosive final phase. Many investors abandon their SIPs around year 6 or 7, right when the corpus is about to accelerate. Understanding this concept can help you avoid this common and costly mistake, and it is one of the biggest reasons financial planners recommend reviewing this framework before you even start your first SIP.

Benefits of Following the SIP 8 4 3 Rule

There are several reasons why financial planners frequently reference this framework when advising new investors.

First, it sets realistic expectations. New investors often expect fast results, and this breakdown clearly shows that the biggest gains come only after staying invested for over a decade.

Second, this approach encourages consistency. Since the framework is built around uninterrupted monthly contributions, it naturally discourages investors from pausing or withdrawing their SIP during market corrections.

Third, this concept is easy to customize. Whether your monthly SIP is Rs. 5,000, Rs. 10,000, or Rs. 21,250, the same three-phase pattern applies proportionally, making it useful for investors at every income level.

Fourth, it reinforces the importance of starting early. Because the final phase depends on a large accumulated base, delaying your SIP by even a few years can significantly reduce your final corpus under this framework.

Fifth, this framework works as an excellent goal-setting tool for families planning long-term milestones such as a child’s higher education, a home down payment, or retirement. Because the three phases are clearly defined, you can map specific life goals to specific years of your investment journey and track your progress with far more clarity than a vague “invest and forget” approach.

Things to Keep in Mind Before Relying on the SIP 8 4 3 Rule

While this framework is a useful planning tool, it comes with a few important caveats. The 12 percent annual return used in this calculation is an assumption based on long-term historical equity market averages in India — it is not guaranteed. Actual mutual fund returns fluctuate every year depending on market conditions, and some years may even see negative returns.

This model also assumes zero interruptions in your investment. Missing SIP installments, withdrawing money mid-way, or switching funds frequently can all reduce the compounding benefit that this framework depends on.

Taxation is another factor this framework does not account for. Long-term capital gains on equity mutual funds are taxed once you redeem your investment, so your actual take-home corpus may be slightly lower than what this projection suggests on paper.

Finally, fund selection matters. This rule assumes a well-performing diversified equity fund. Choosing a poorly performing fund, or one with a high expense ratio, can slow down the compounding curve that the entire framework relies on. It is worth reviewing your fund’s historical performance, fund manager track record, and expense ratio at least once a year to make sure your investment stays aligned with the assumptions behind this model.

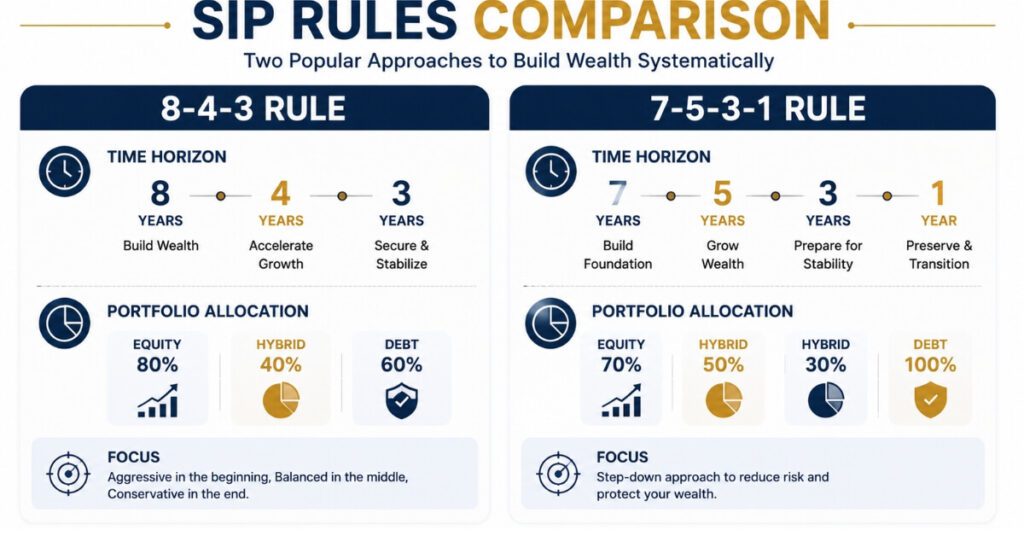

SIP 8 4 3 Rule vs Other Popular SIP Strategies

Investors often compare the SIP 8 4 3 rule with the 7-5-3-1 rule, another popular mutual fund framework. While the 7-5-3-1 rule focuses on portfolio allocation across different market caps and fund types, this framework is purely about the compounding timeline of a single ongoing SIP. Both strategies are complementary — you can use the 7-5-3-1 rule to decide where to invest, and the SIP 8 4 3 rule to understand how long you need to stay invested to see meaningful results. Neither strategy replaces professional financial advice, but together they offer a useful mental model for structuring a long-term equity investment plan.

How to Start Using the SIP 8 4 3 Rule for Your Own Goals

Applying this framework to your own financial plan starts with identifying your target corpus and working backward. If you want to reach Rs. 1 crore in 15 years, the SIP 8 4 3 rule suggests a monthly investment of around Rs. 21,250 at a 12 percent expected return. If your goal amount or timeline is different, you can adjust the monthly contribution accordingly while the same three-phase structure still applies.

It also helps to build your overall retirement and wealth strategy around multiple pillars, not just mutual fund SIPs. Many salaried employees in India already contribute regularly to their Employees’ Provident Fund, and keeping that account active and accessible matters just as much as your SIP discipline. If you want to check or manage your EPF account digitally, you can refer to our detailed guide on EPFO online services restored, which walks you through accessing EPFO’s online portal for balance checks, withdrawals, and other services. Combining a disciplined EPF contribution with a SIP based on the SIP 8 4 3 rule can significantly strengthen your long-term retirement corpus.

For authoritative, up-to-date data on mutual fund performance and SIP trends across India, you can also refer to AMFI India, the official industry body that publishes verified mutual fund statistics and investor education resources.

Staying disciplined for the full fifteen-year cycle is often the hardest part of this journey, not the math itself. Setting up an auto-debit SIP, avoiding the temptation to time the market, and reviewing your portfolio only once a year are simple habits that help investors stick to the SIP 8 4 3 rule without emotional interference. It also helps to increase your SIP amount gradually every year in line with your income growth, a practice commonly known as a “step-up SIP,” which can help you reach your target corpus even faster than this base framework suggests.

Common Mistakes Investors Make While Chasing a Rs. 1 Crore Corpus

Even with a clear roadmap in hand, many investors stumble at the same predictable points. The first common mistake is stopping the SIP the moment the market falls. Corrections are a normal part of any long-term equity journey, and pausing contributions during a downturn actually works against you, since you end up buying fewer units at lower prices when the market eventually recovers.

The second mistake is chasing past performance. Investors often switch funds every year based on which scheme topped the previous year’s return charts, not realizing that frequent switching resets the compounding clock and adds unnecessary exit loads or tax liabilities. Sticking with a well-researched, diversified equity fund for the entire duration usually outperforms constant fund-hopping.

A third mistake is ignoring inflation while setting a target corpus. Rs. 1 crore today will not have the same purchasing power fifteen years from now, so it is worth periodically reassessing whether your target amount still aligns with your future goals, and adjusting your monthly contribution upward if needed.

Finally, many investors forget to diversify beyond a single fund or asset class. While a single equity SIP can absolutely help you reach a large corpus, spreading investments across a mix of large-cap, mid-cap, and hybrid funds can help manage volatility while still capturing long-term growth.

Who Should Consider This Long-Term SIP Strategy?

This kind of long-term, phase-based investing approach works particularly well for young professionals in their twenties and early thirties who have a genuine fifteen-year runway ahead of them. It also suits parents planning for a child’s higher education or marriage, since these goals typically fall ten to eighteen years into the future, matching the framework’s natural timeline almost perfectly.

It may not be the right approach, however, for investors nearing retirement or those with short-term goals of five years or less, since equity mutual funds carry short-term volatility that may not average out favorably in a shorter window. For such investors, a mix of debt instruments and shorter-duration hybrid funds is usually more appropriate, and consulting a certified financial planner before finalizing an asset allocation is strongly recommended.

Frequently Asked Questions About the SIP 8 4 3 Rule

Q1.What exactly does the SIP 8 4 3 rule mean?

It explains how a mutual fund SIP grows in three phases over 15 years — 8 years of steady growth, 4 years where the corpus roughly doubles, and a final 3 years where growth accelerates the most, assuming a 12 percent annual return.

Q2.Is the SIP 8 4 3 rule guaranteed to work?

No. This framework is based on an assumed average annual return of 12 percent, which reflects long-term historical equity performance but is not guaranteed. Actual results depend on market conditions and fund performance.

Q3.How much do I need to invest monthly to become a crorepati using the SIP 8 4 3 rule?

Based on this calculation, investing Rs. 21,250 per month for 15 years at an average 12 percent annual return can help you build a corpus of approximately Rs. 1 crore.

Q4.Can I apply the SIP 8 4 3 rule to a smaller monthly SIP amount?

Yes. This framework applies proportionally to any SIP amount. Whether you invest Rs. 5,000 or Rs. 50,000 per month, the same three-phase compounding pattern holds true over a 15-year period.

Q5.What is the difference between the SIP 8 4 3 rule and the 7-5-3-1 rule?

This framework focuses on the compounding timeline of a single SIP, while the 7-5-3-1 rule focuses on how to structure your portfolio across different fund categories and market caps.

Conclusion

The SIP 8 4 3 rule is a powerful reminder that wealth creation through mutual funds is a long-term game, not a shortcut. By understanding the three phases of this framework, you can set realistic expectations, stay invested through the slow early years, and avoid the common mistake of quitting right before the biggest growth phase begins. Whether your target is Rs. 1 crore or a different financial goal altogether, this simple, proven framework can help you plan your journey with confidence and discipline.

Financial Disclaimer

This article is for educational and informational purposes only and should not be considered personalized financial or investment advice. Mutual fund investments, including SIPs, are subject to market risks, and past performance is not indicative of future results. The 12 percent annual return used in this article is an assumption based on historical averages and is not guaranteed. Please read all scheme-related documents carefully and consult a certified financial advisor before making any investment decisions. SK Smart Digital Hub does not take responsibility for any financial losses incurred based on the information provided in this article

Pingback: Sovereign Gold Bond 2026: 5 Shocking Truths Investors Fear